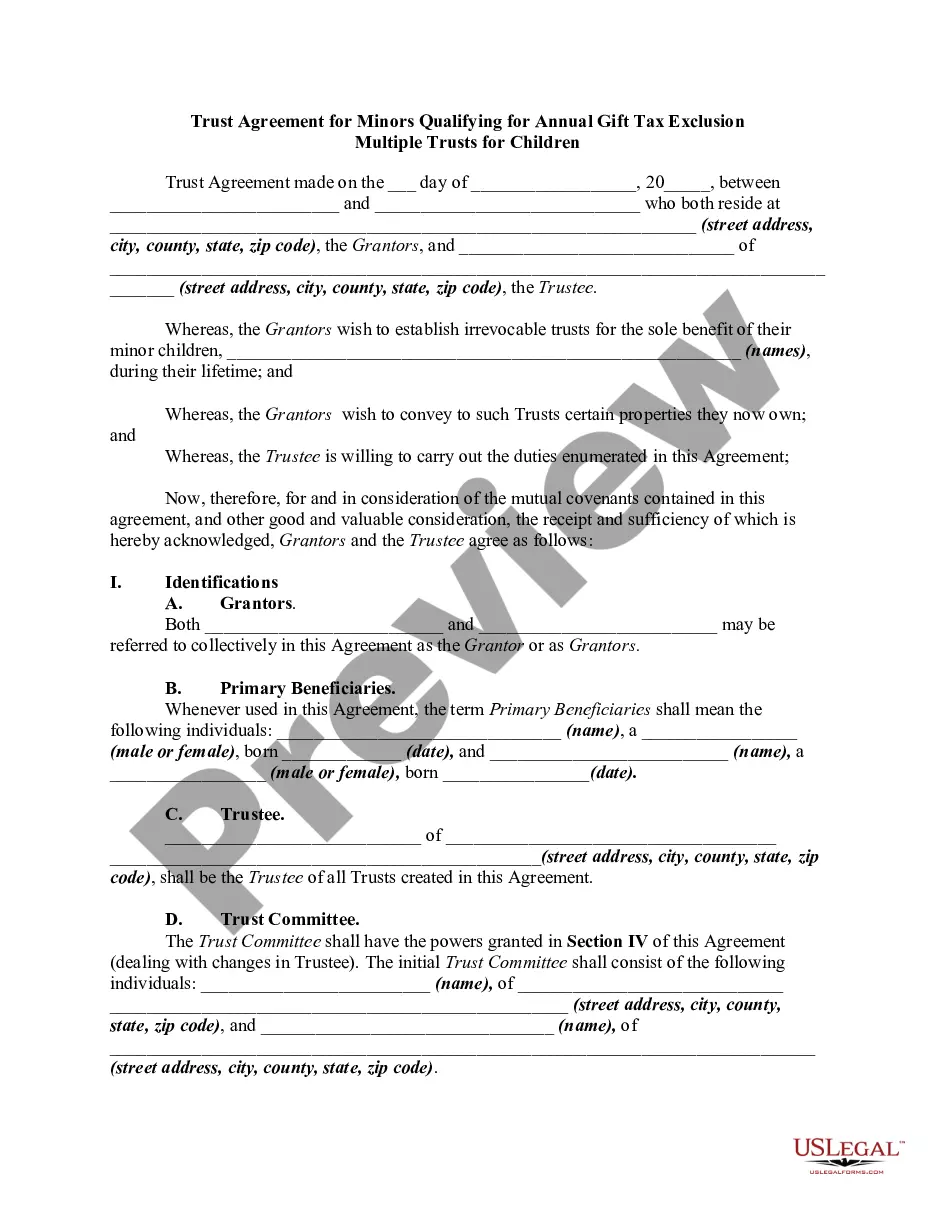

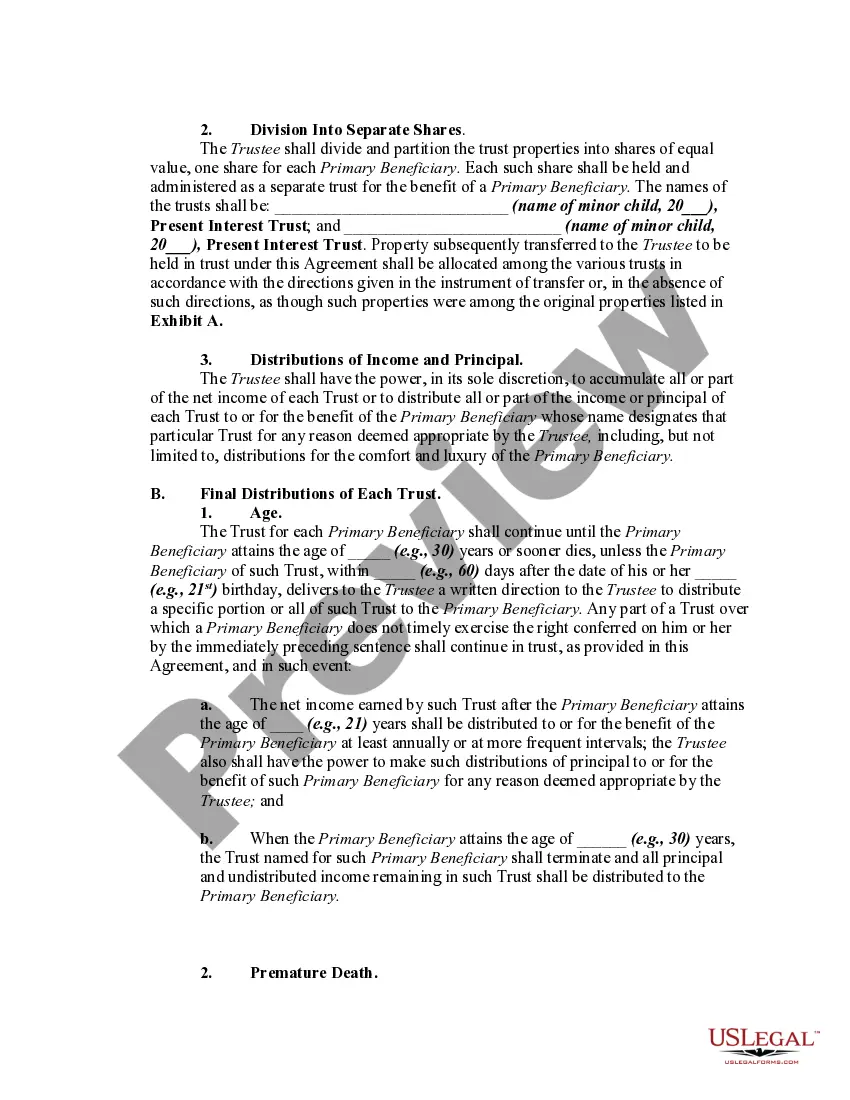

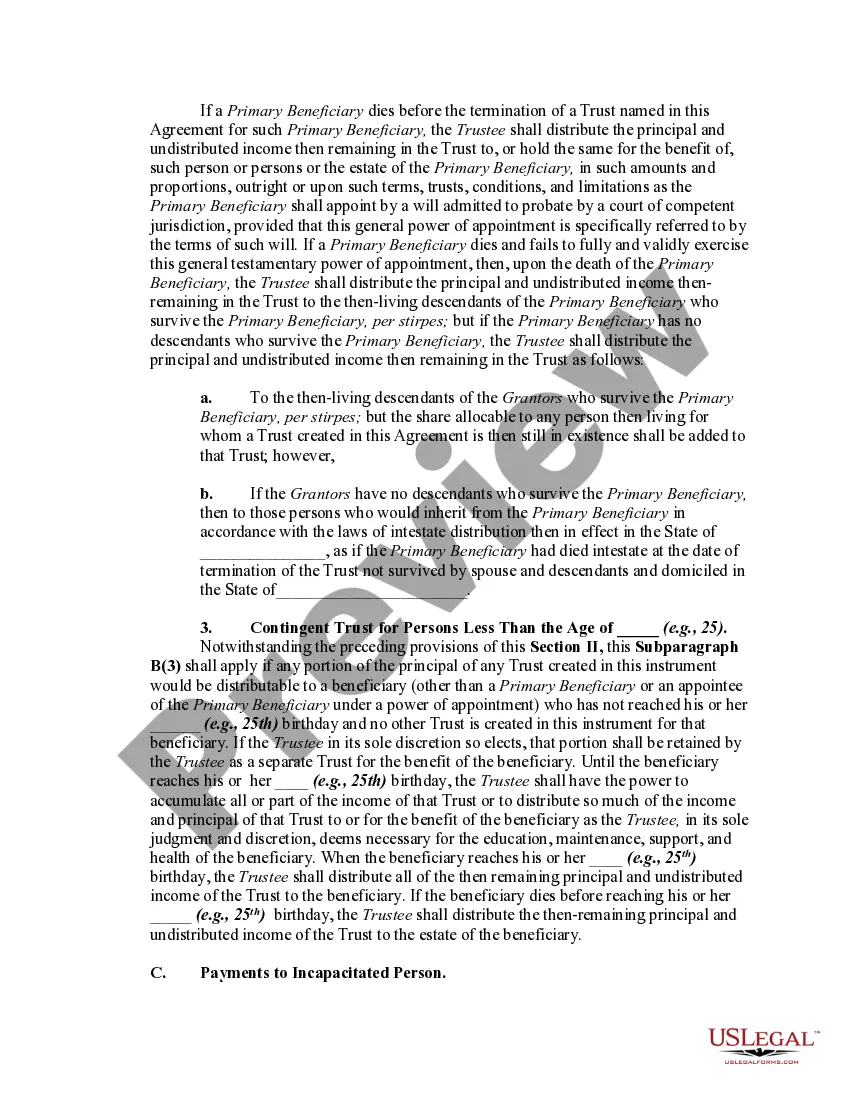

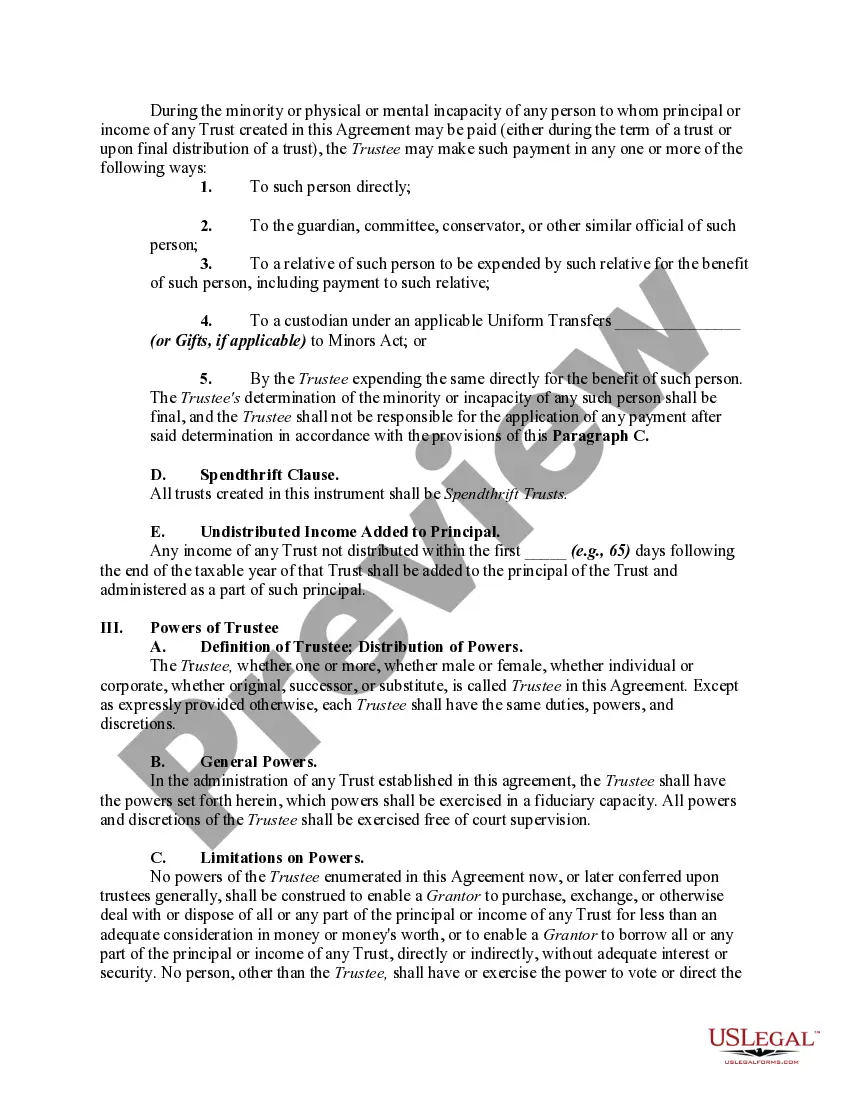

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

The Utah Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document that allows individuals to establish multiple trusts for their children, while still taking advantage of the annual gift tax exclusion. This type of trust agreement is particularly beneficial for parents or grandparents who want to gift money or assets to their minor children or grandchildren without incurring gift taxes. By creating multiple trusts, the person can distribute their gifts among different trust accounts, ensuring that each child receives a separate trust fund. This can be useful when there are multiple beneficiaries, as it allows for more flexibility in managing and safeguarding the assets. Additionally, establishing a trust agreement for minors provides several advantages, such as asset protection, tax planning, and control over the distribution of funds. There are various types of Utah Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children, each suited to specific circumstances or preferences: 1. Individual Trusts: This type of trust agreement establishes separate trusts for each child, ensuring that the assets and investments are managed and distributed individually for each beneficiary. 2. Pot Trusts: Pot trusts combine the assets of multiple beneficiaries into a single trust, allowing for more efficient management of funds and potentially avoiding higher administrative costs. 3. Testamentary Trusts: These trust agreements are created through a will and take effect upon the death of the person establishing the trust. Testamentary trusts are useful for individuals who want to ensure that their assets are properly managed for the benefit of their minor children after their passing. 4. Discretionary Trusts: With discretionary trusts, the trustee has the discretion to determine how and when to distribute the assets to the beneficiaries, providing greater control over the use and timing of the funds. 5. Accumulation Trusts: Accumulation trusts allow for the income generated by the trust assets to accumulate and be reinvested, ensuring growth and potentially increasing the value of the trust over time. Overall, the Utah Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children provides a versatile and effective tool for parents or grandparents who wish to gift assets to their minor children or grandchildren, while minimizing tax liabilities and ensuring proper management and protection of the assets.