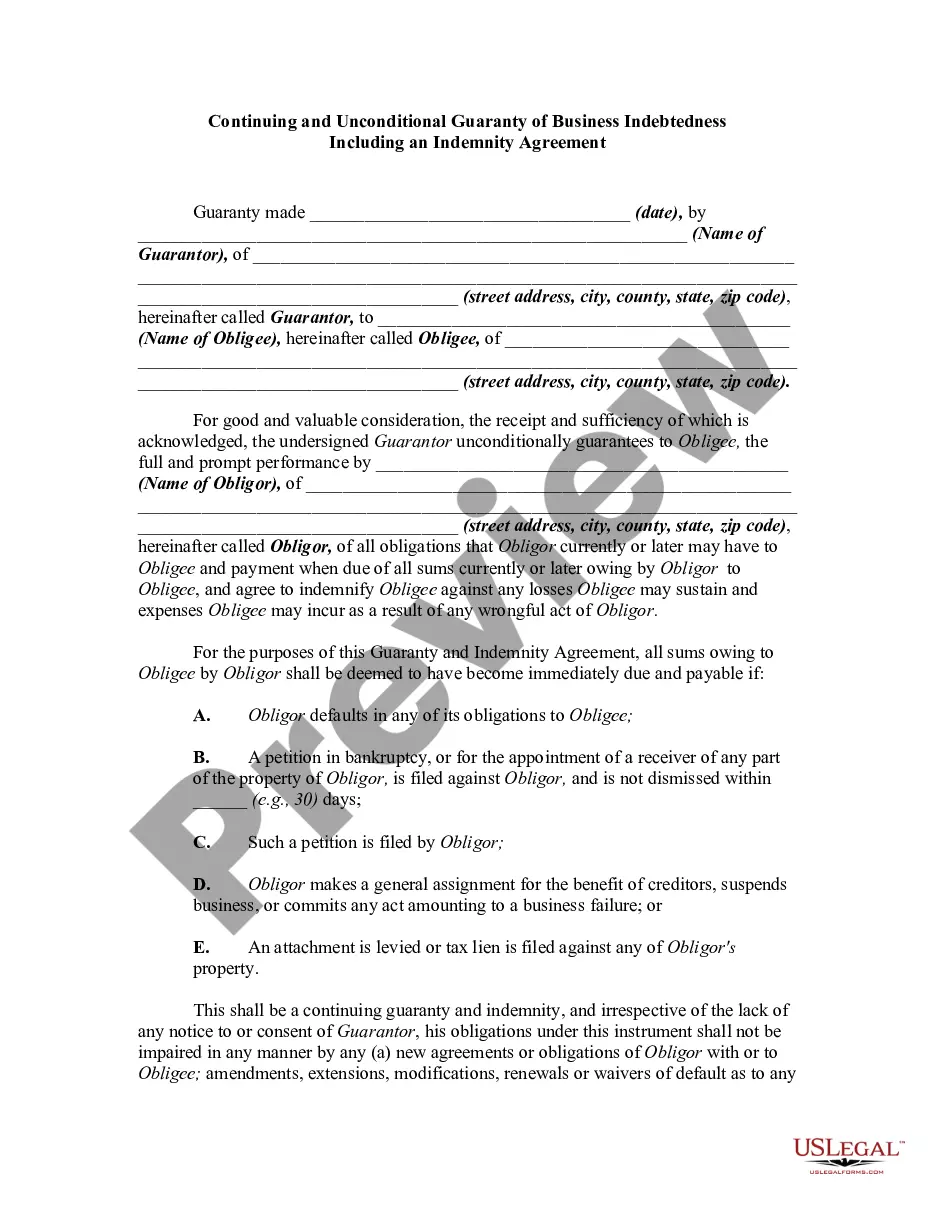

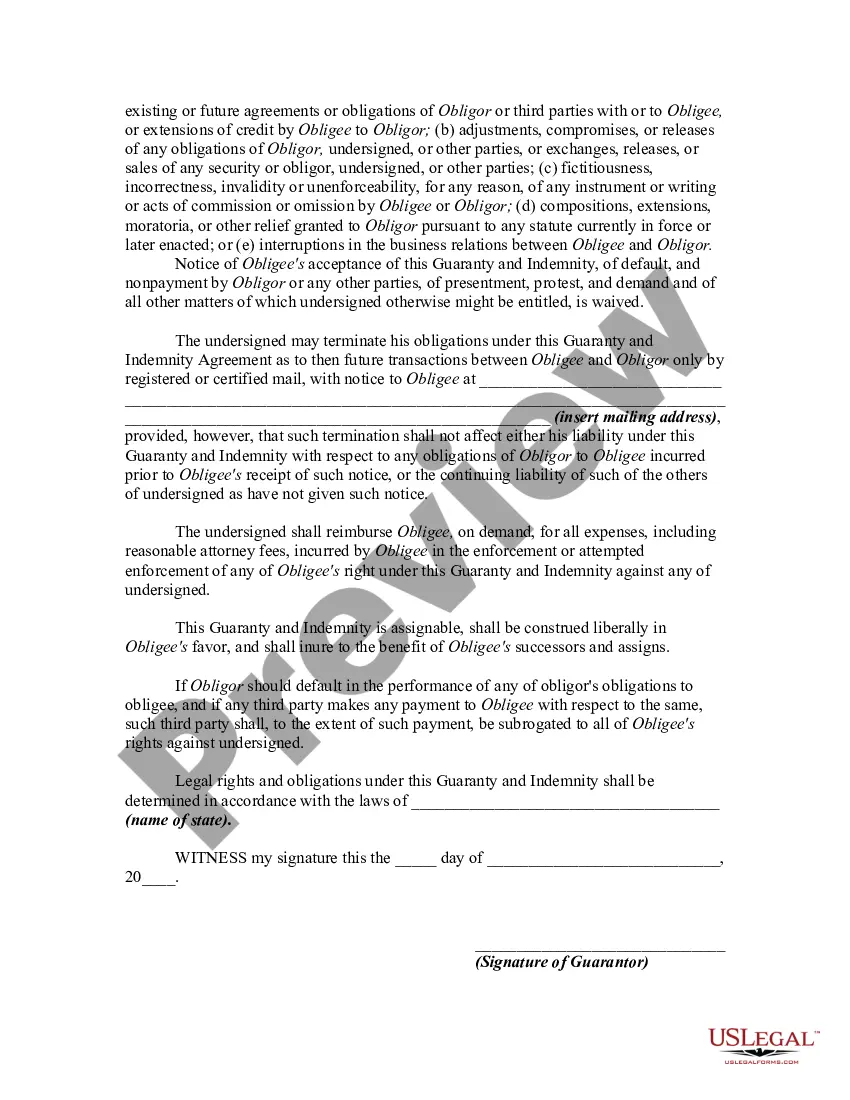

A guaranty is an undertaking on the part of one person (the guarantor) which binds the guarantor to performing the obligation of the debtor or obligor in the event of default by the debtor or obligor. The contract of guaranty may be absolute or it may be conditional. An absolute or unconditional guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A guaranty may be either continuing or restricted. The contract is restricted if it is limited to the guaranty of a single transaction or to a limited number of specific transactions and is not effective as to transactions other than those guaranteed. The contract is continuing if it contemplates a future course of dealing during an indefinite period, or if it is intended to cover a series of transactions or a succession of credits, or if its purpose is to give to the principal debtor a standing credit to be used by him or her from time to time.

Utah Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a legal document that outlines the terms and conditions under which a guarantor agrees to be held responsible for a business's debt. This agreement is commonly used in commercial transactions to provide additional assurance to lenders or creditors. In Utah, there are various types of Continuing and Unconditional Guaranty of Business Indebtedness agreements, each tailored to specific circumstances and requirements. These agreements may be categorized based on the purpose, scope, or parties involved. Some common variations include: 1. Personal Guaranty: A personal guaranty is when an individual, typically the business owner or a major shareholder, agrees to personally guarantee the business's indebtedness. This means that in the event of default, the guarantor's personal assets can be used to satisfy the debt. 2. Corporate Guaranty: In some cases, rather than an individual, a corporation or another business entity may act as the guarantor. This type of guaranty offers protection to lenders by leveraging the assets and resources of the guarantor company. 3. Limited Guaranty: A limited guaranty limits the liability of the guarantor to only a portion of the total debt. This type of agreement may specify a maximum limit or a percentage of the total debt for which the guarantor is responsible. 4. Continuing Guaranty: A continuing guaranty remains in effect until the debt is fully paid off or until a specific condition or event occurs, such as the lender's written consent to release the guarantor. This ensures that the guarantor's liability continues over time. 5. Unconditional Guaranty: An unconditional guaranty holds the guarantor liable without any conditions or exceptions. Regardless of circumstances, the guarantor is fully responsible for the business's debt obligations. An indemnity agreement is often included as part of the Continuing and Unconditional Guaranty of Business Indebtedness contract in Utah. This agreement acts as an additional layer of protection for the lender or creditor, wherein the guarantor agrees to indemnify the lender against any losses, damages, or costs incurred due to non-payment or default by the business. It is crucial to consult with a qualified attorney or legal professional to draft and review any Utah Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement, ensuring it complies with state laws and accurately reflects the intentions of all parties involved.Utah Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a legal document that outlines the terms and conditions under which a guarantor agrees to be held responsible for a business's debt. This agreement is commonly used in commercial transactions to provide additional assurance to lenders or creditors. In Utah, there are various types of Continuing and Unconditional Guaranty of Business Indebtedness agreements, each tailored to specific circumstances and requirements. These agreements may be categorized based on the purpose, scope, or parties involved. Some common variations include: 1. Personal Guaranty: A personal guaranty is when an individual, typically the business owner or a major shareholder, agrees to personally guarantee the business's indebtedness. This means that in the event of default, the guarantor's personal assets can be used to satisfy the debt. 2. Corporate Guaranty: In some cases, rather than an individual, a corporation or another business entity may act as the guarantor. This type of guaranty offers protection to lenders by leveraging the assets and resources of the guarantor company. 3. Limited Guaranty: A limited guaranty limits the liability of the guarantor to only a portion of the total debt. This type of agreement may specify a maximum limit or a percentage of the total debt for which the guarantor is responsible. 4. Continuing Guaranty: A continuing guaranty remains in effect until the debt is fully paid off or until a specific condition or event occurs, such as the lender's written consent to release the guarantor. This ensures that the guarantor's liability continues over time. 5. Unconditional Guaranty: An unconditional guaranty holds the guarantor liable without any conditions or exceptions. Regardless of circumstances, the guarantor is fully responsible for the business's debt obligations. An indemnity agreement is often included as part of the Continuing and Unconditional Guaranty of Business Indebtedness contract in Utah. This agreement acts as an additional layer of protection for the lender or creditor, wherein the guarantor agrees to indemnify the lender against any losses, damages, or costs incurred due to non-payment or default by the business. It is crucial to consult with a qualified attorney or legal professional to draft and review any Utah Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement, ensuring it complies with state laws and accurately reflects the intentions of all parties involved.