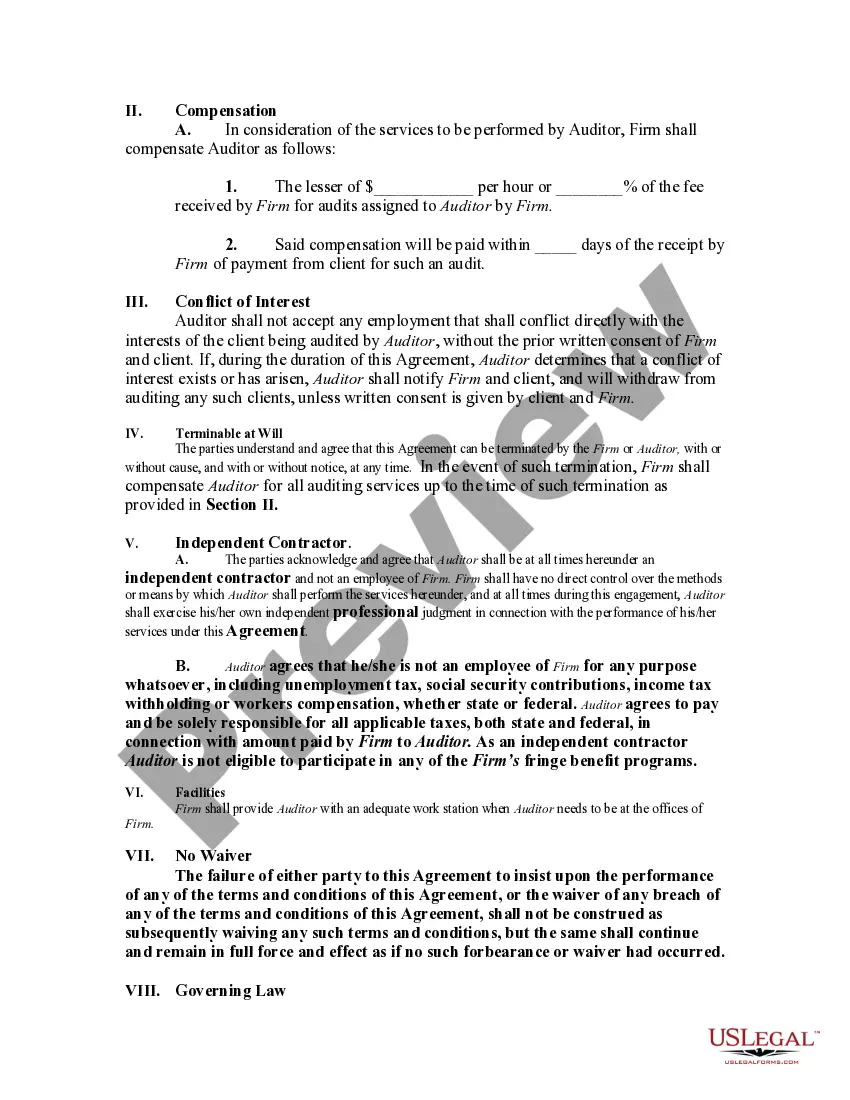

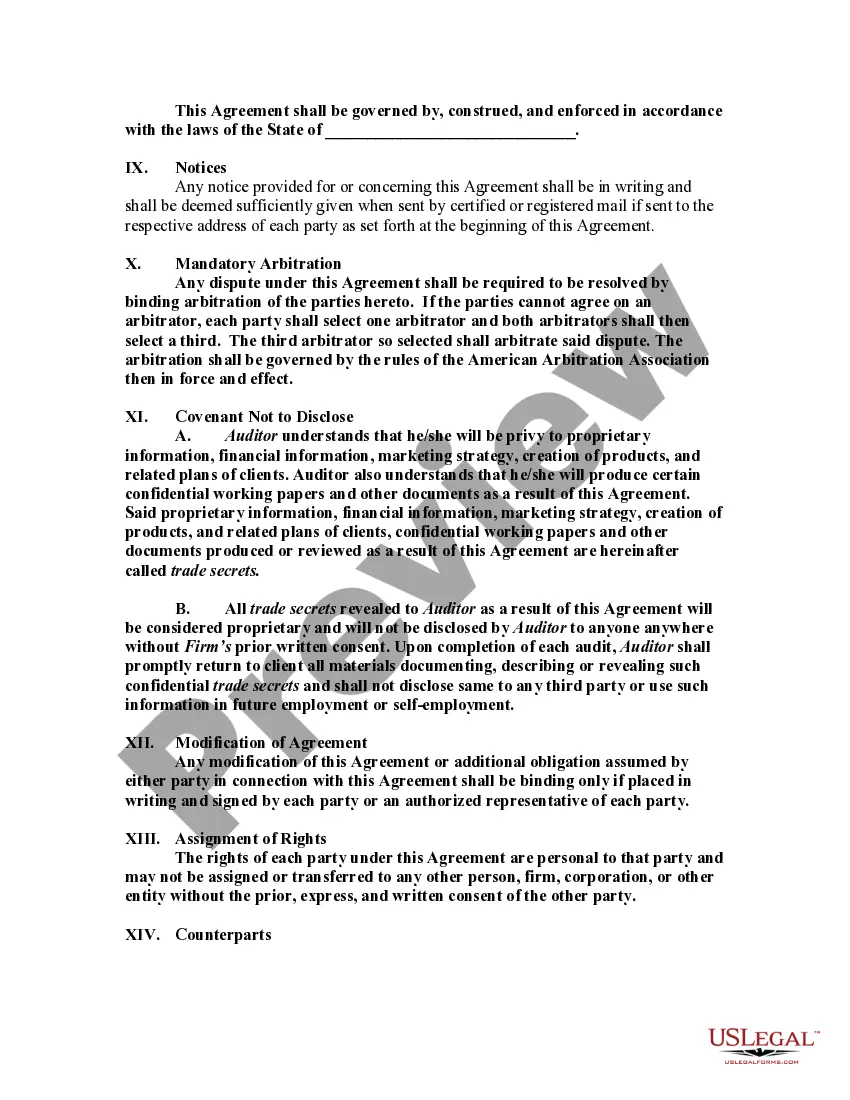

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

Title: Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: A Comprehensive Guide Introduction: In the realm of accounting, it is common for accounting firms in Utah to engage auditors as self-employed independent contractors to provide their expertise and services. This detailed description aims to elucidate the key features, benefits, and legal aspects of the Utah Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor. Additionally, it will touch upon the different types of agreements that exist within this context. 1. Definition and Nature of Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In the state of Utah, this agreement pertains to a legally binding contract between an accounting firm, acting as the entity seeking auditing services, and an auditor, operating as a self-employed independent contractor. It outlines the terms, expectations, and obligations of both parties involved. 2. Key Elements of the Agreement: — Scope of Work: Clearly defining the specific auditing services the independent contractor will provide, including the audit objectives, timelines, and methodologies. — Compensation and Payment: Establishing the agreed-upon payment structure, such as fixed fees, hourly rates, or project-based remuneration, along with the payment schedule. — Confidentiality and Non-Disclosure: Ensuring the protection of sensitive information and trade secrets by implementing confidentiality clauses. — Independent Contractor Status: Explicitly stating that the auditor operates as an independent contractor and is responsible for their own taxes, insurance, and benefits. — Intellectual Property Rights: Addressing the ownership and usage rights of any intellectual property created during the engagement. — Termination and Dispute Resolution: Outlining the circumstances under which either party can terminate the agreement, as well as the methods for resolving conflicts or disputes. 3. Benefits of Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: — Flexibility: Accounting firms can engage auditors on a project-by-project basis, allowing them to tap into specialized expertise without the long-term commitment. — Cost-Effectiveness: By hiring independent contractors, firms can avoid costs associated with full-time employees, such as benefits, office space, and training. — Expanded Talent Pool: Independent auditors bring diverse skills and experiences, enhancing the quality and variety of auditing services available to accounting firms. — Reduced Legal Liability: The independence of the contractor limits the accounting firm's liability in terms of employment rights, taxes, and benefits. Types of Utah Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: — General Auditing Agreement: A standard agreement covering various auditing services provided by the self-employed independent contractor. — Specialized Auditing Agreement: Tailored agreements for specific auditing areas like financial, internal, compliance, or performance audits. — Long-Term Agreement: An ongoing contractual relationship between the accounting firm and the auditor, spanning multiple projects or audits. Conclusion: Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor offers numerous advantages for accounting firms seeking auditing services while affording auditors the freedom to work independently. Understanding the key elements and variations of this agreement is essential for both parties to establish a transparent and mutually beneficial working relationship.Title: Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: A Comprehensive Guide Introduction: In the realm of accounting, it is common for accounting firms in Utah to engage auditors as self-employed independent contractors to provide their expertise and services. This detailed description aims to elucidate the key features, benefits, and legal aspects of the Utah Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor. Additionally, it will touch upon the different types of agreements that exist within this context. 1. Definition and Nature of Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In the state of Utah, this agreement pertains to a legally binding contract between an accounting firm, acting as the entity seeking auditing services, and an auditor, operating as a self-employed independent contractor. It outlines the terms, expectations, and obligations of both parties involved. 2. Key Elements of the Agreement: — Scope of Work: Clearly defining the specific auditing services the independent contractor will provide, including the audit objectives, timelines, and methodologies. — Compensation and Payment: Establishing the agreed-upon payment structure, such as fixed fees, hourly rates, or project-based remuneration, along with the payment schedule. — Confidentiality and Non-Disclosure: Ensuring the protection of sensitive information and trade secrets by implementing confidentiality clauses. — Independent Contractor Status: Explicitly stating that the auditor operates as an independent contractor and is responsible for their own taxes, insurance, and benefits. — Intellectual Property Rights: Addressing the ownership and usage rights of any intellectual property created during the engagement. — Termination and Dispute Resolution: Outlining the circumstances under which either party can terminate the agreement, as well as the methods for resolving conflicts or disputes. 3. Benefits of Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: — Flexibility: Accounting firms can engage auditors on a project-by-project basis, allowing them to tap into specialized expertise without the long-term commitment. — Cost-Effectiveness: By hiring independent contractors, firms can avoid costs associated with full-time employees, such as benefits, office space, and training. — Expanded Talent Pool: Independent auditors bring diverse skills and experiences, enhancing the quality and variety of auditing services available to accounting firms. — Reduced Legal Liability: The independence of the contractor limits the accounting firm's liability in terms of employment rights, taxes, and benefits. Types of Utah Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: — General Auditing Agreement: A standard agreement covering various auditing services provided by the self-employed independent contractor. — Specialized Auditing Agreement: Tailored agreements for specific auditing areas like financial, internal, compliance, or performance audits. — Long-Term Agreement: An ongoing contractual relationship between the accounting firm and the auditor, spanning multiple projects or audits. Conclusion: Utah Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor offers numerous advantages for accounting firms seeking auditing services while affording auditors the freedom to work independently. Understanding the key elements and variations of this agreement is essential for both parties to establish a transparent and mutually beneficial working relationship.