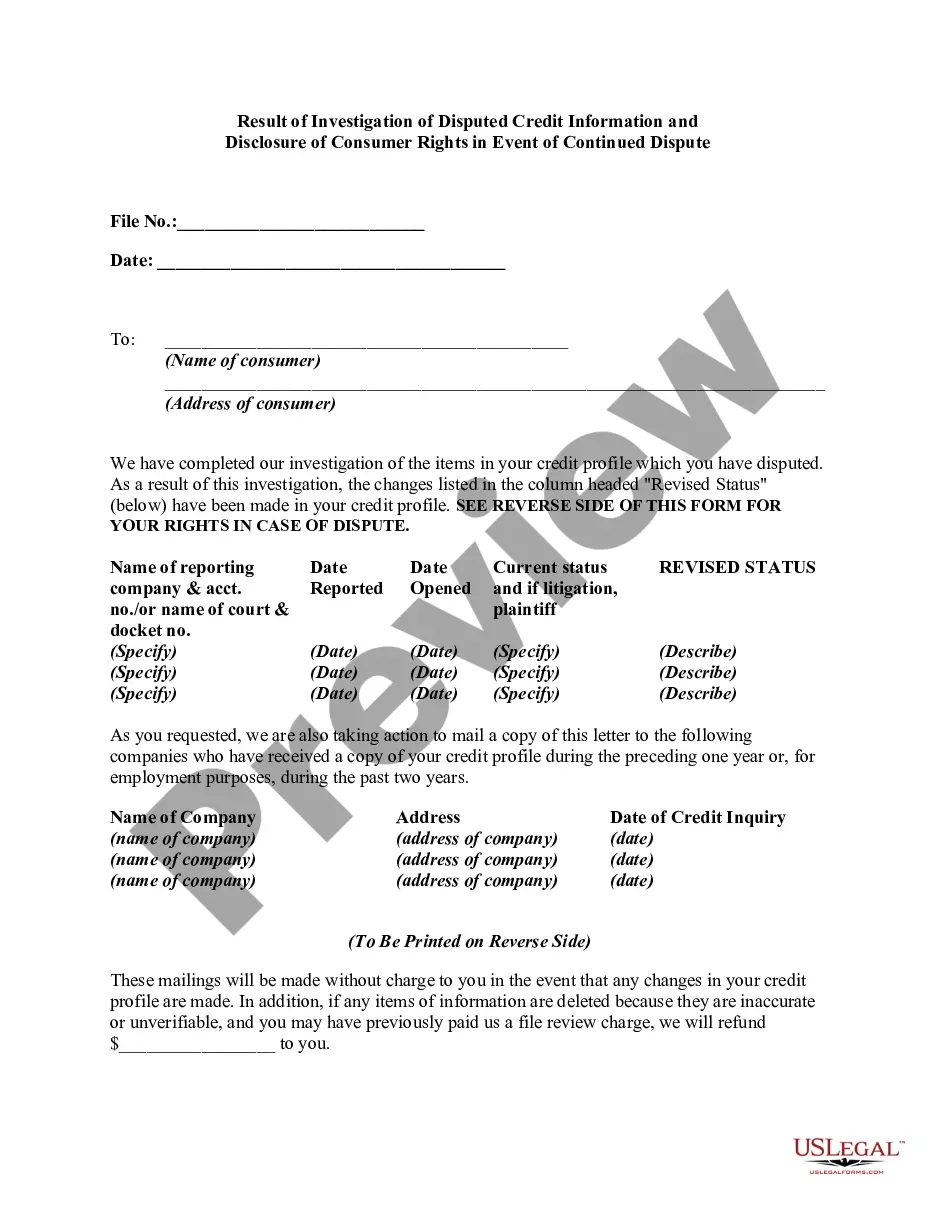

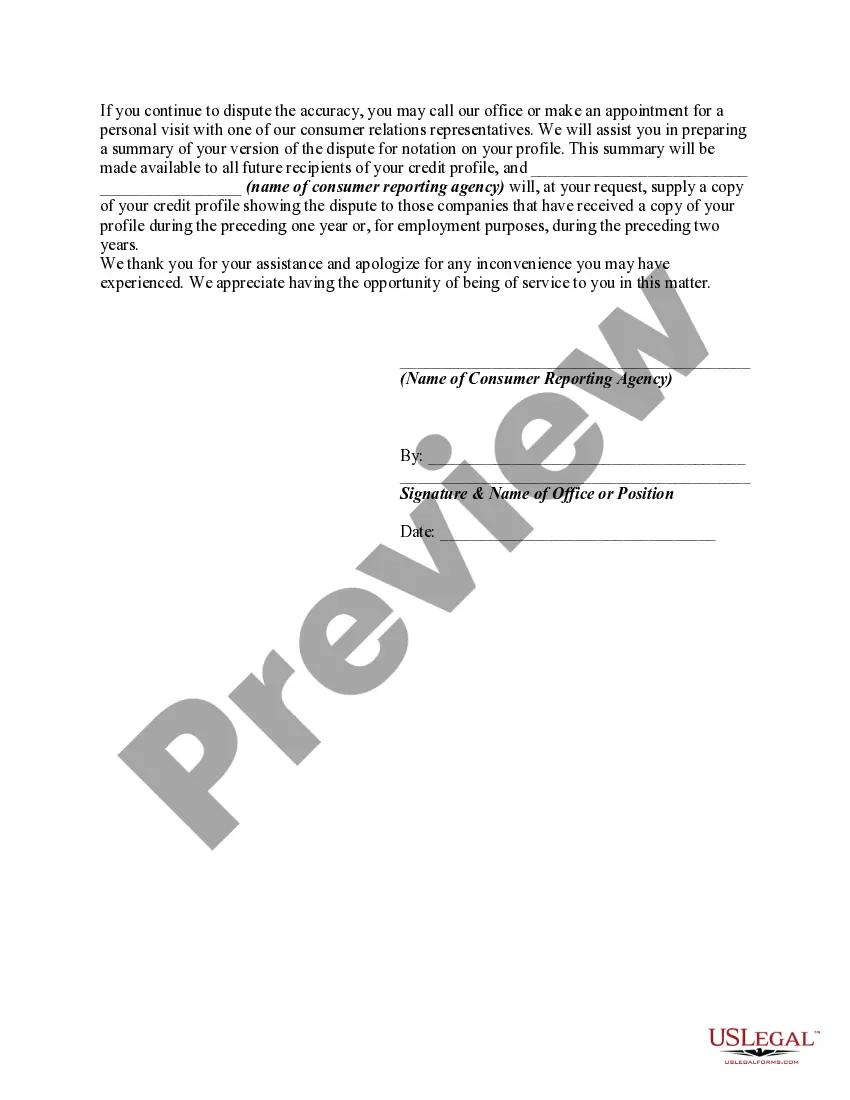

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Utah Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute Keywords: Utah, result of investigation, disputed credit information, disclosure of consumer rights, continued dispute Introduction: In Utah, when consumers engage in a dispute regarding their credit information, it is essential to understand the possible outcomes of an investigation and the resulting consumer rights in the event of a continued dispute. This comprehensive guide will provide detailed information on the results of investigations related to disputed credit information and the disclosure of consumer rights in Utah. 1. Investigation Process: Utah follows a structured investigation process when resolving credit information disputes. The relevant credit reporting agencies initiate an investigation upon receiving a consumer's dispute. The investigation typically involves contacting the information provider and verifying the accuracy of the disputed information. Each dispute is treated on a case-by-case basis, ensuring a thorough analysis. 2. Utah Result of Investigation: a. Verified and Accurate Information: If the investigation confirms that the disputed item is accurate and valid, the credit reporting agency will inform the consumer accordingly. The disputed information will remain on the consumer's credit report unless it reaches its expiration period according to federal laws (e.g., seven years for most negative information). b. Corrected and Updated Information: In cases where the investigation reveals errors or inaccuracies, the credit reporting agency will update the consumer's credit report accordingly. This includes eliminating or correcting any misreported information that affected the consumer's credit history negatively. c. Removal of Disputed Information: If the investigation concludes that the disputed information is incorrect or cannot be verified within a reasonable time frame, the credit reporting agency must remove the item from the consumer's credit report. This removal will positively impact the consumer's credit score and overall creditworthiness. 3. Disclosure of Consumer Rights: Utah ensures that consumers are informed of their rights during and after the investigation process. These rights include: a. Written Notification — Consumers have the right to receive written notifications regarding the results of the investigation, whether the information was verified, corrected, or removed. b. Free Credit Report — Following the completion of the investigation, Utah allows consumers to obtain a free copy of their credit report from each credit reporting agency involved in the dispute. This ensures transparency and empowers consumers to monitor their credit status. c. Continued Disputes — If a consumer disagrees with the results of the investigation or believes the information was inaccurately verified, they have the right to continue the dispute. This guarantees that consumers can rectify any unresolved credit information issues and maintain accurate credit histories. Conclusion: Understanding the results of an investigation into disputed credit information is crucial for Utah consumers. By being aware of their rights and the possible outcomes, individuals can take appropriate actions to rectify any inaccuracies and protect their financial well-being. Stay informed, exercise your rights, and ensure the accuracy of your credit history in Utah.Title: Utah Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute Keywords: Utah, result of investigation, disputed credit information, disclosure of consumer rights, continued dispute Introduction: In Utah, when consumers engage in a dispute regarding their credit information, it is essential to understand the possible outcomes of an investigation and the resulting consumer rights in the event of a continued dispute. This comprehensive guide will provide detailed information on the results of investigations related to disputed credit information and the disclosure of consumer rights in Utah. 1. Investigation Process: Utah follows a structured investigation process when resolving credit information disputes. The relevant credit reporting agencies initiate an investigation upon receiving a consumer's dispute. The investigation typically involves contacting the information provider and verifying the accuracy of the disputed information. Each dispute is treated on a case-by-case basis, ensuring a thorough analysis. 2. Utah Result of Investigation: a. Verified and Accurate Information: If the investigation confirms that the disputed item is accurate and valid, the credit reporting agency will inform the consumer accordingly. The disputed information will remain on the consumer's credit report unless it reaches its expiration period according to federal laws (e.g., seven years for most negative information). b. Corrected and Updated Information: In cases where the investigation reveals errors or inaccuracies, the credit reporting agency will update the consumer's credit report accordingly. This includes eliminating or correcting any misreported information that affected the consumer's credit history negatively. c. Removal of Disputed Information: If the investigation concludes that the disputed information is incorrect or cannot be verified within a reasonable time frame, the credit reporting agency must remove the item from the consumer's credit report. This removal will positively impact the consumer's credit score and overall creditworthiness. 3. Disclosure of Consumer Rights: Utah ensures that consumers are informed of their rights during and after the investigation process. These rights include: a. Written Notification — Consumers have the right to receive written notifications regarding the results of the investigation, whether the information was verified, corrected, or removed. b. Free Credit Report — Following the completion of the investigation, Utah allows consumers to obtain a free copy of their credit report from each credit reporting agency involved in the dispute. This ensures transparency and empowers consumers to monitor their credit status. c. Continued Disputes — If a consumer disagrees with the results of the investigation or believes the information was inaccurately verified, they have the right to continue the dispute. This guarantees that consumers can rectify any unresolved credit information issues and maintain accurate credit histories. Conclusion: Understanding the results of an investigation into disputed credit information is crucial for Utah consumers. By being aware of their rights and the possible outcomes, individuals can take appropriate actions to rectify any inaccuracies and protect their financial well-being. Stay informed, exercise your rights, and ensure the accuracy of your credit history in Utah.