The "look through" trust can affords long term IRA deferrals and special protection or tax benefits for the family. But, as with all specialized tools, you must use it only in the right situation. If the IRA participant names a trust as beneficiary, and the trust meets certain requirements, for purposes of calculating minimum distributions after death, one can "look through" the trust and treat the trust beneficiary as the designated beneficiary of the IRA. You can then use the beneficiary's life expectancy to calculate minimum distributions. Were it not for this "look through" rule, the IRA or plan assets would have to be paid out over a much shorter period after the owner's death, thereby losing long term deferral.

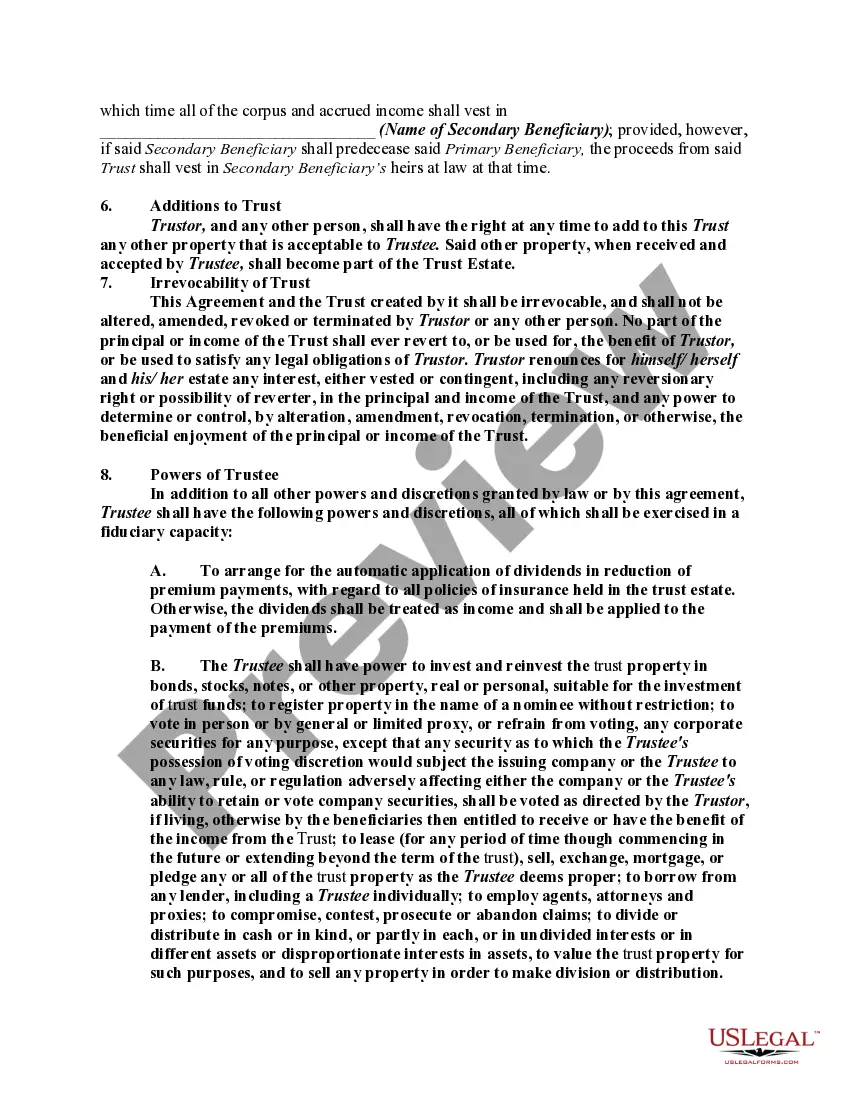

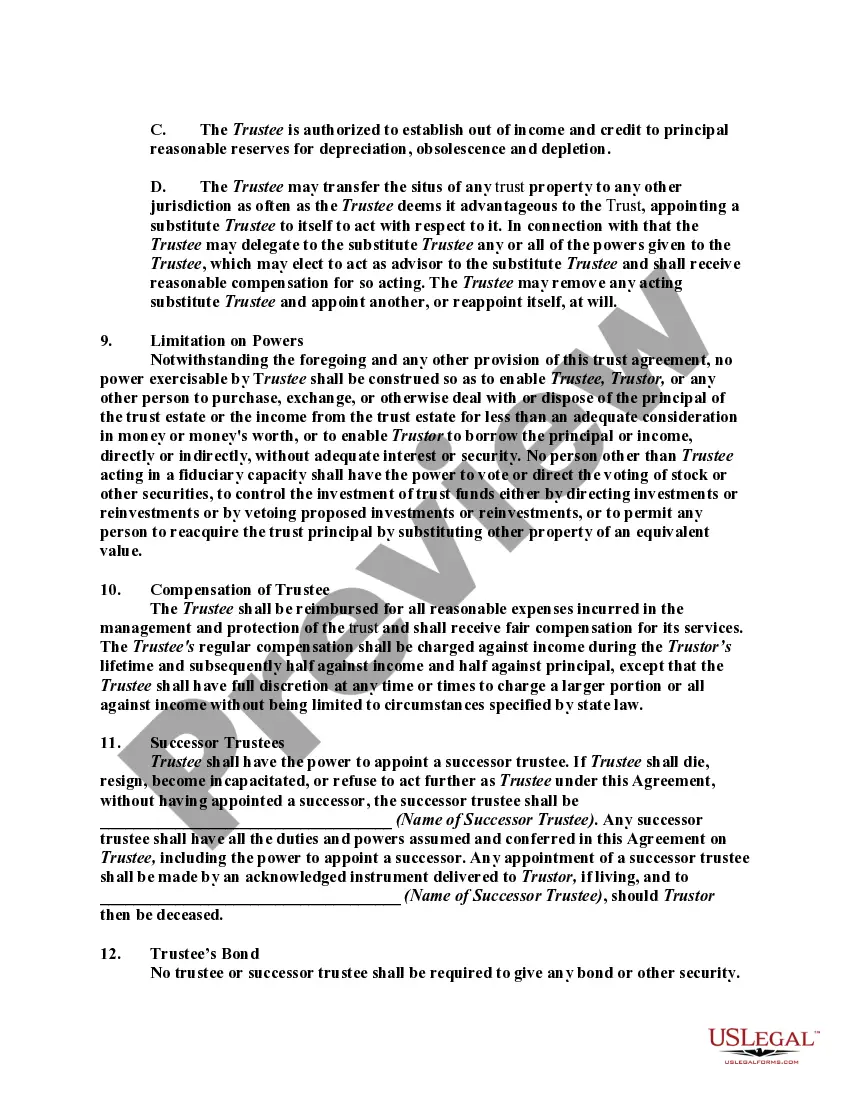

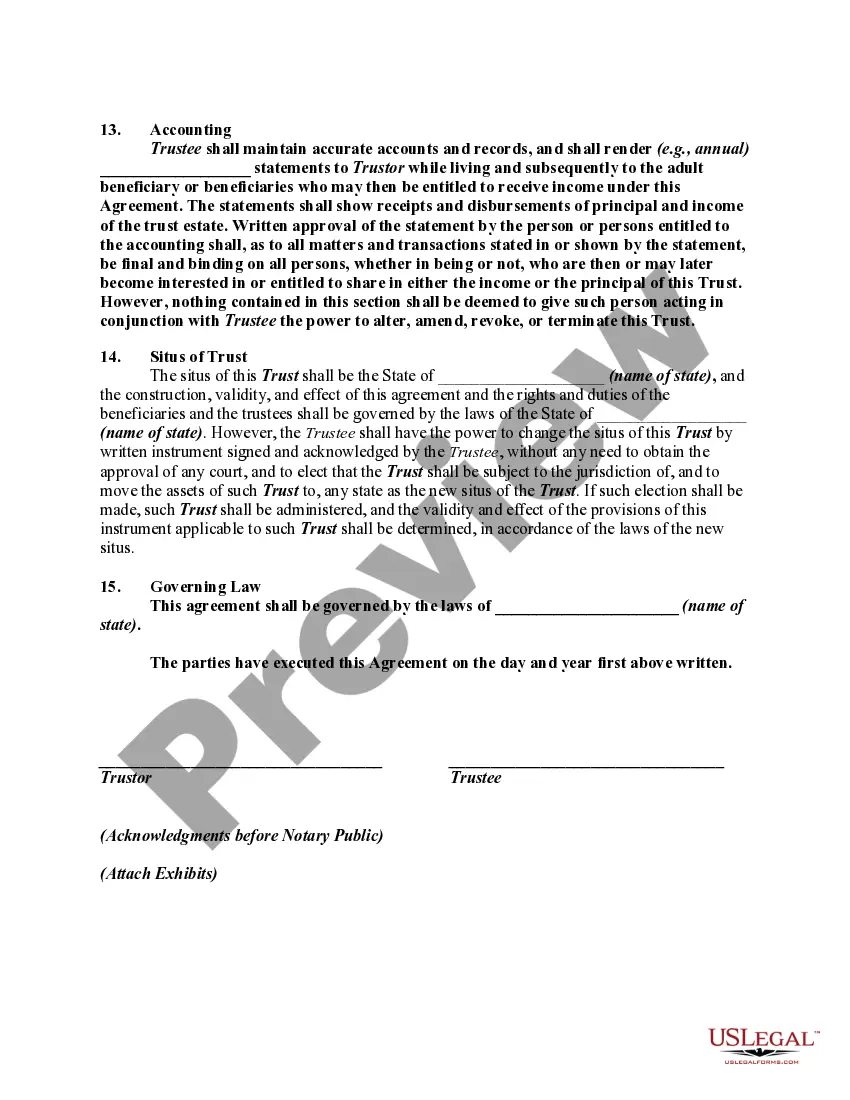

Utah Irrevocable Trust as Designated Beneficiary of an Individual Retirement Account (IRA) An Irrevocable Trust is a legal entity established by an individual (settler) for the benefit of designated beneficiaries. In the context of an Individual Retirement Account (IRA), a Utah Irrevocable Trust can be named as a designated beneficiary, providing unique advantages and potential estate planning benefits. The primary purpose of designating an Irrevocable Trust as the beneficiary of an IRA is to control the distribution and protection of the IRA assets, ensuring that they are managed and dispersed according to the settler's wishes. By utilizing the trust structure, the settler can carefully outline how the assets are distributed, provide for specific beneficiaries, and potentially minimize taxes and future probate costs. Different types of Utah Irrevocable Trusts that can be designated as beneficiaries of an IRA include: 1. Testamentary Trust: This type of trust is created through a person's will and comes into effect upon their death. The IRA assets will be distributed to the trust, governed by the instructions outlined in the will. 2. Living Trust: Also known as a revocable trust, this type of trust is established during the settler's lifetime and can be changed or revoked. The IRA assets can be transferred to the living trust, and the trust document will dictate how they are managed and distributed. 3. Special Needs Trust: This type of trust provides for the financial needs of a beneficiary with special needs or disabilities without impacting their eligibility for government benefits. By designating a special needs trust as the IRA beneficiary, the settler can provide ongoing financial support while safeguarding the beneficiary's eligibility for assistance programs. 4. Charitable Remainder Trust: This trust allows the settler to transfer the IRA assets to a charitable organization, with the provision that income is provided to designated beneficiaries for a specified period. After the end of the trust term, the remaining assets are donated to the designated charity. 5. Credit Shelter Trust: Also known as a bypass trust or family trust, this type of trust is typically used to minimize estate taxes. By designating the trust as the IRA beneficiary, the settler can ensure that the trust's assets are protected from estate taxes at their death, and the trust can provide income to the surviving spouse while preserving the principal for future generations. In summary, a Utah Irrevocable Trust as the Designated Beneficiary of an Individual Retirement Account offers numerous estate planning benefits, including control over distribution, potential tax savings, and protection of assets. Depending on the specific objectives and circumstances, different types of trusts can be utilized to meet the settler's goals and provide for the well-being of beneficiaries. It is crucial to consult with an experienced estate planning attorney to navigate the complexities of establishing and managing such trusts.