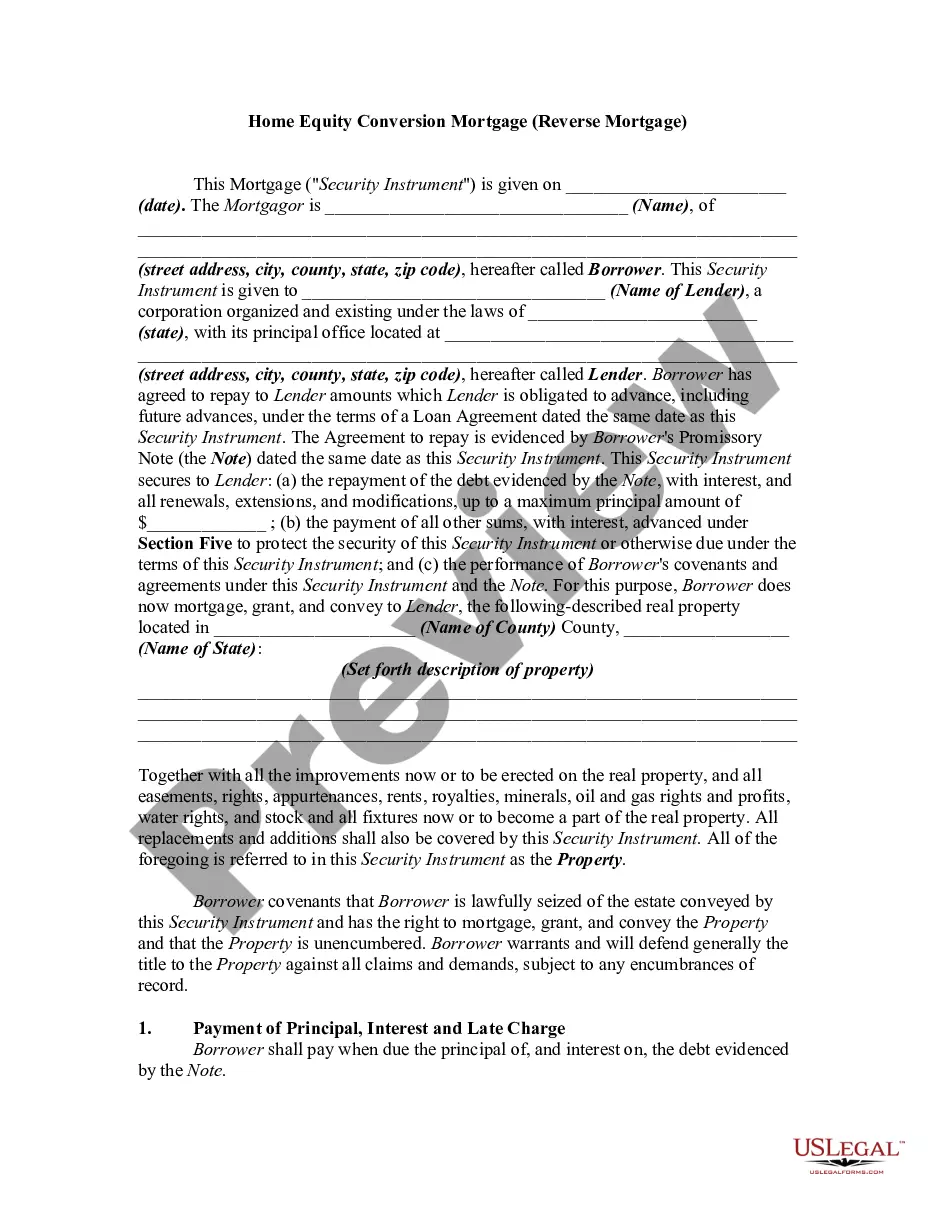

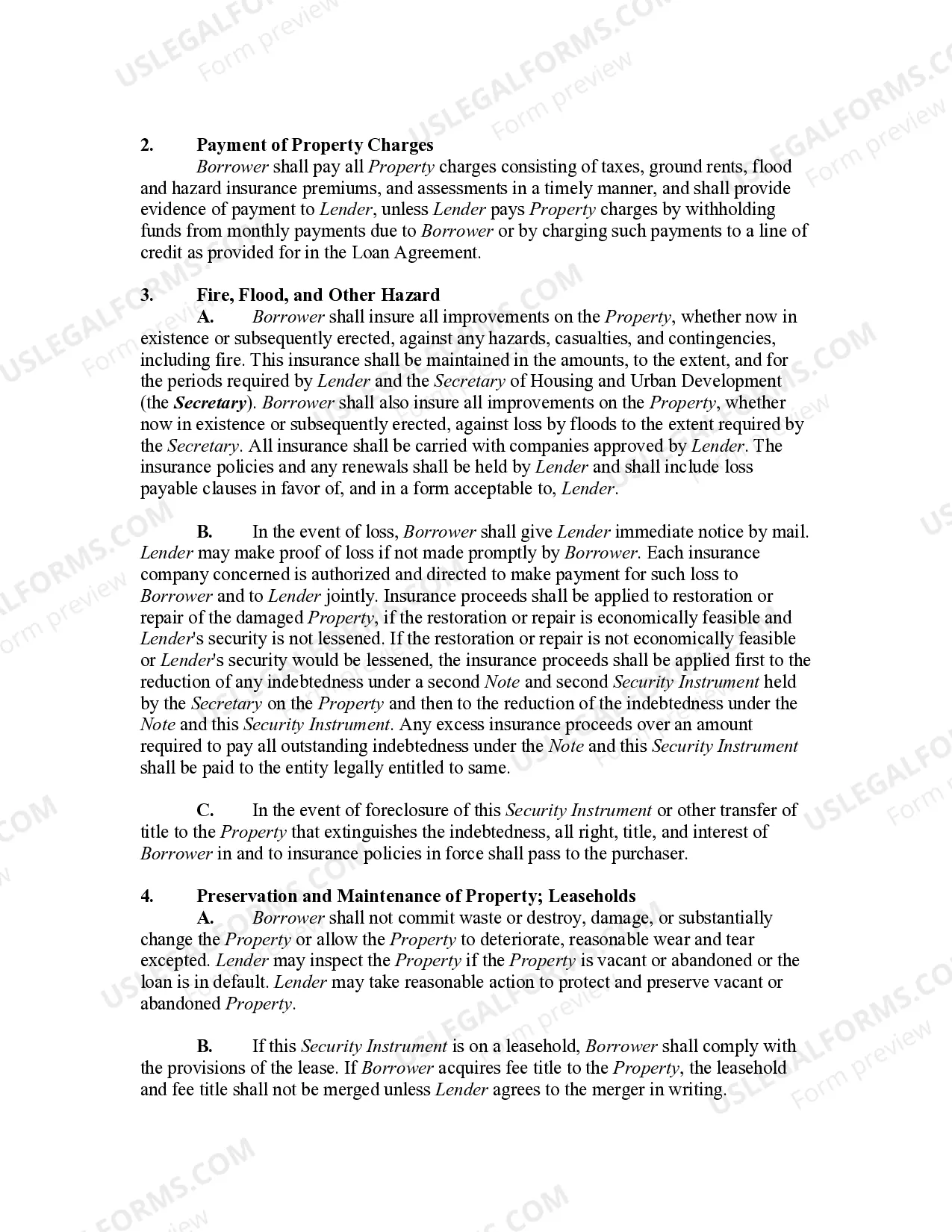

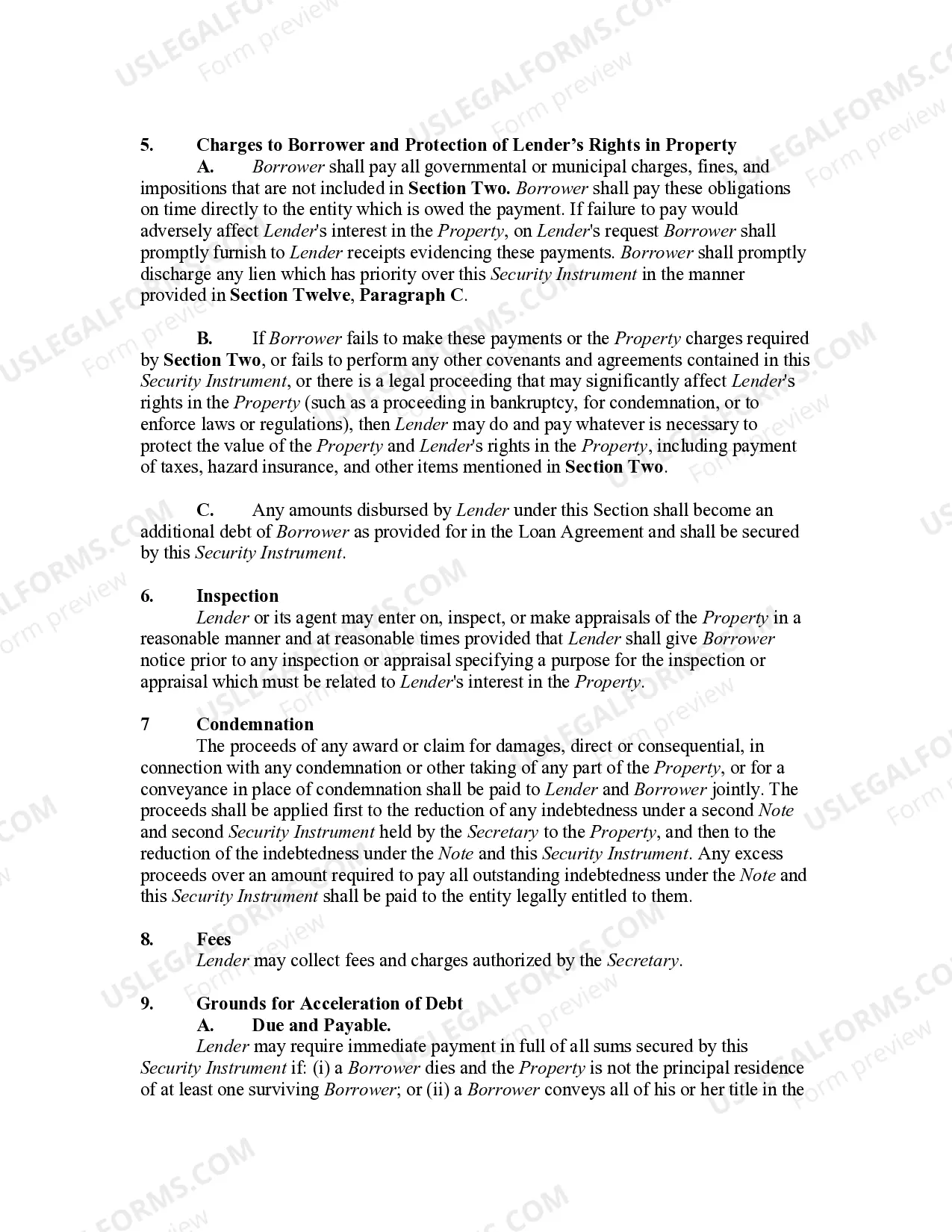

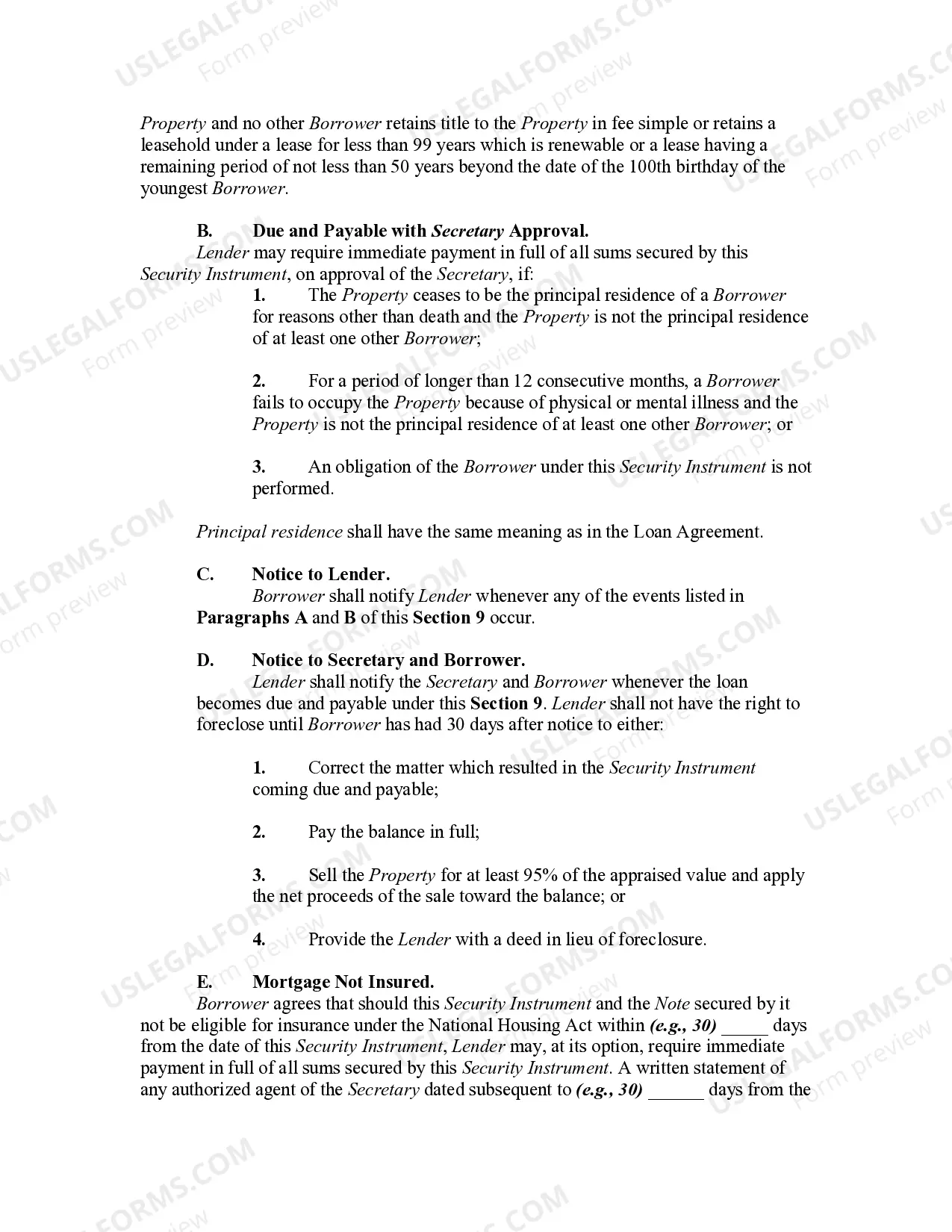

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

A Utah Home Equity Conversion Mortgage (HELM) or reverse mortgage is a unique financial product designed for homeowners aged 62 and older who want to convert a portion of their home equity into cash. It enables seniors to access the funds they have accumulated in their homes without having to sell or move out. With a Utah HELM, seniors can receive their loan proceeds in various ways, such as a lump sum, monthly payments, a line of credit, or a combination of these options. The loan amount received depends on factors such as the borrower's age, home value, interest rates, and the chosen disbursement method. One type of Utah HELM is the Fixed-Rate HELM, which provides a lump sum payment and a fixed interest rate throughout the loan term. This option is suitable for seniors who prefer a predictable payment structure. Another type is the Adjustable-Rate HELM, which offers flexibility in terms of disbursement options. Borrowers can choose from various payment plans, including monthly payments, a line of credit, a combination of both, or even change the payment plan during the loan term. The interest rate on the loan adjusts periodically based on market conditions. Utah also offers the HELM for Purchase option, allowing seniors to purchase a new primary residence using a reverse mortgage. This option is particularly beneficial for those wishing to downsize, age in place, or relocate to a more suitable home. A key aspect of the Utah HELM is that borrowers are not required to make monthly mortgage payments. Instead, they are required to maintain the property, pay property taxes, homeowner's insurance, and any applicable homeowners' association fees. It is important to note that Utah Helms are federally insured by the Federal Housing Administration (FHA), which provides added protection and safeguards for borrowers. Non-recourse provisions ensure that neither the borrower nor their estate will owe more than the home's value at the time of repayment. To be eligible for a Utah HELM, homeowners must meet certain criteria, including being at least 62 years old, owning their home outright or having a low remaining mortgage balance, and living in the home as their primary residence. In conclusion, a Utah Home Equity Conversion Mortgage (HELM) or reverse mortgage is a valuable financial tool for seniors to tap into their home equity and improve their overall financial situation. With various options available, including fixed-rate and adjustable-rate Helms, as well as the HELM for Purchase, Utah seniors can choose the option that best suits their needs and goals.A Utah Home Equity Conversion Mortgage (HELM) or reverse mortgage is a unique financial product designed for homeowners aged 62 and older who want to convert a portion of their home equity into cash. It enables seniors to access the funds they have accumulated in their homes without having to sell or move out. With a Utah HELM, seniors can receive their loan proceeds in various ways, such as a lump sum, monthly payments, a line of credit, or a combination of these options. The loan amount received depends on factors such as the borrower's age, home value, interest rates, and the chosen disbursement method. One type of Utah HELM is the Fixed-Rate HELM, which provides a lump sum payment and a fixed interest rate throughout the loan term. This option is suitable for seniors who prefer a predictable payment structure. Another type is the Adjustable-Rate HELM, which offers flexibility in terms of disbursement options. Borrowers can choose from various payment plans, including monthly payments, a line of credit, a combination of both, or even change the payment plan during the loan term. The interest rate on the loan adjusts periodically based on market conditions. Utah also offers the HELM for Purchase option, allowing seniors to purchase a new primary residence using a reverse mortgage. This option is particularly beneficial for those wishing to downsize, age in place, or relocate to a more suitable home. A key aspect of the Utah HELM is that borrowers are not required to make monthly mortgage payments. Instead, they are required to maintain the property, pay property taxes, homeowner's insurance, and any applicable homeowners' association fees. It is important to note that Utah Helms are federally insured by the Federal Housing Administration (FHA), which provides added protection and safeguards for borrowers. Non-recourse provisions ensure that neither the borrower nor their estate will owe more than the home's value at the time of repayment. To be eligible for a Utah HELM, homeowners must meet certain criteria, including being at least 62 years old, owning their home outright or having a low remaining mortgage balance, and living in the home as their primary residence. In conclusion, a Utah Home Equity Conversion Mortgage (HELM) or reverse mortgage is a valuable financial tool for seniors to tap into their home equity and improve their overall financial situation. With various options available, including fixed-rate and adjustable-rate Helms, as well as the HELM for Purchase, Utah seniors can choose the option that best suits their needs and goals.