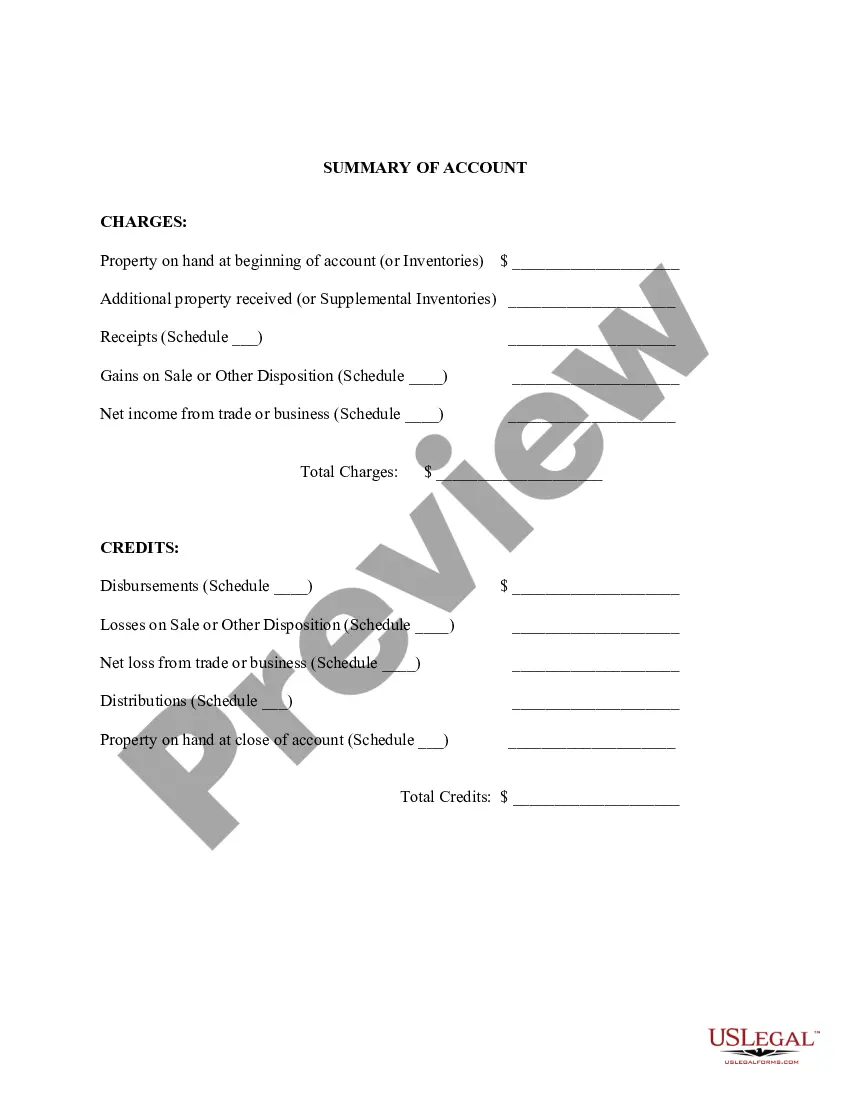

Title: Understanding Utah Summary of Account for Inventory of Business Introduction: In the state of Utah, businesses are required to file a Summary of Account for Inventory (SAI) annually. This document holds substantial importance as it helps the Utah State Tax Commission determine the value of a business's inventory for tax purposes. This article aims to provide a detailed description of the Utah Summary of Account for Inventory of Business, explaining its purpose, requirements, and implementation. Keywords: Utah, Summary of Account, Inventory of Business, tax purposes, requirements, implementation Understanding Utah Summary of Account for Inventory of Business: 1. Purpose: The primary purpose of the Utah Summary of Account for Inventory of Business is to assist the Utah State Tax Commission in determining the taxable value of a business's inventory. It allows for fair assessment and proper taxation of inventory assets across various industries. 2. Requirements: a. Annual Filing: All businesses in Utah, regardless of their size and industry, must file the Summary of Account for Inventory on an annual basis. b. Reporting Deadline: The inventory summary must be filed with the Utah State Tax Commission no later than the last day of February each year. c. Detailed Information: The SAI requires businesses to provide detailed information about their inventory, including its value, description, and location. 3. Types of Utah Summary of Account for Inventory of Business: Though a single type of SAI is applicable to all businesses in Utah, there may be variations based on the type of inventory being reported. Some common types of SAI may include: a. Retail Inventory: This type of SAI is relevant to businesses that engage in retail sales, involving tangible products sold directly to consumers. b. Manufacturing Inventory: Manufacturing businesses that produce goods through various stages of production may have a different format for reporting their inventory. c. Wholesale Inventory: Businesses involved in wholesale trading, acting as intermediaries between manufacturers and retailers, may have specific reporting requirements. 4. Implementation: a. Accurate Valuation: The SAI requires businesses to provide accurate valuations for their inventory assets. The inventory's value is determined by considering factors such as purchase cost, market value, and depreciation. b. Supporting Documentation: In addition to filing the SAI, businesses must maintain proper supporting documentation, such as purchase and sale invoices, inventory counts, and valuation reports. c. Consequences of Non-Compliance: Failure to file the Summary of Account for Inventory or providing inaccurate information may result in penalties, audits, or investigations by the Utah State Tax Commission. Conclusion: The Utah Summary of Account for Inventory of Business serves as an essential tool in determining the taxable value of inventory assets. Businesses in Utah must comply with the filing requirements and provide accurate information to ensure fair taxation. By understanding the purpose, requirements, and implementation of the Utah SAI, businesses can fulfill their responsibilities and maintain compliance with state tax regulations. Keywords: Utah, Summary of Account, Inventory of Business, tax purposes, requirements, implementation, types, accurate valuation, supporting documentation, consequences of non-compliance.

Utah Summary of Account for Inventory of Business

Description

How to fill out Utah Summary Of Account For Inventory Of Business?

It is possible to devote hrs on the Internet trying to find the lawful record web template that suits the federal and state requirements you will need. US Legal Forms supplies 1000s of lawful kinds that are evaluated by professionals. You can easily obtain or print out the Utah Summary of Account for Inventory of Business from our support.

If you already have a US Legal Forms bank account, it is possible to log in and click on the Download key. Next, it is possible to total, modify, print out, or indication the Utah Summary of Account for Inventory of Business. Each and every lawful record web template you purchase is your own forever. To get yet another duplicate for any bought develop, visit the My Forms tab and click on the related key.

If you work with the US Legal Forms web site the first time, stick to the simple recommendations listed below:

- Initially, ensure that you have chosen the best record web template for that county/city that you pick. See the develop description to make sure you have chosen the correct develop. If readily available, make use of the Preview key to search from the record web template also.

- If you would like discover yet another version of the develop, make use of the Lookup field to obtain the web template that meets your needs and requirements.

- Once you have found the web template you would like, simply click Buy now to continue.

- Choose the costs plan you would like, enter your accreditations, and register for your account on US Legal Forms.

- Total the financial transaction. You may use your Visa or Mastercard or PayPal bank account to pay for the lawful develop.

- Choose the file format of the record and obtain it to the gadget.

- Make alterations to the record if possible. It is possible to total, modify and indication and print out Utah Summary of Account for Inventory of Business.

Download and print out 1000s of record themes making use of the US Legal Forms site, which provides the largest assortment of lawful kinds. Use professional and express-distinct themes to take on your company or person requires.