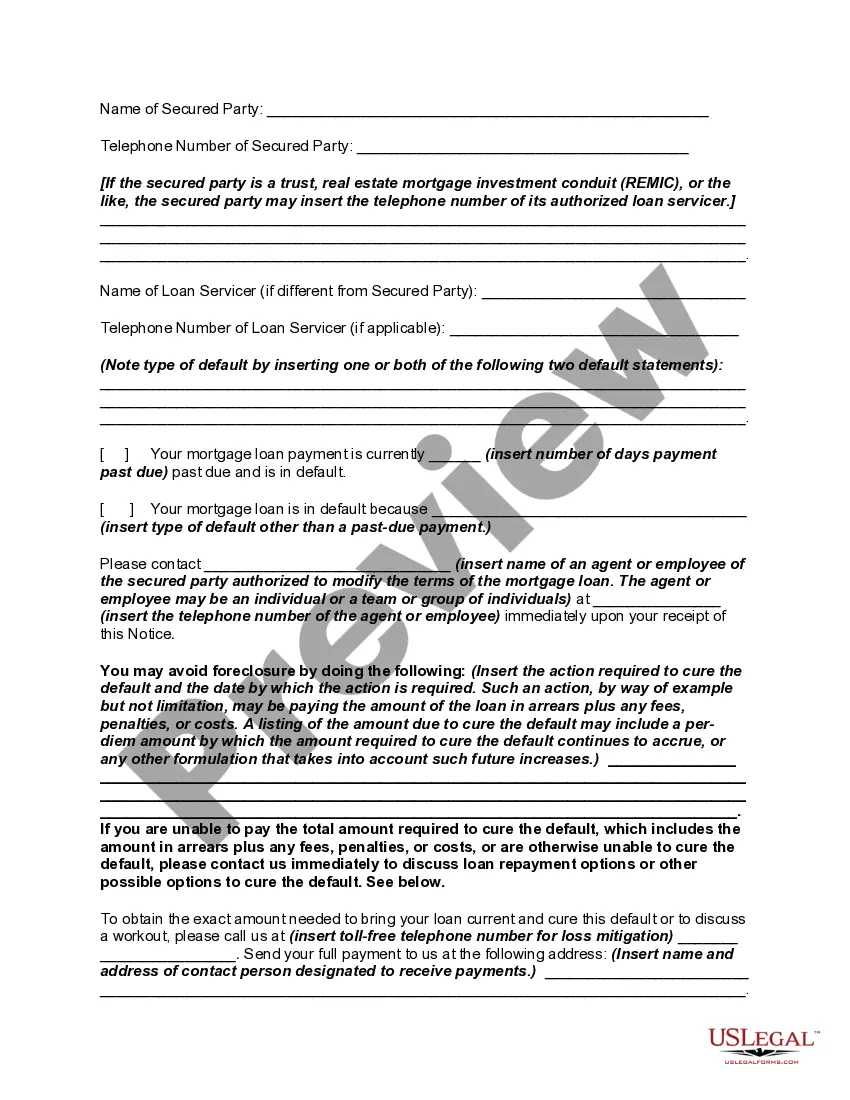

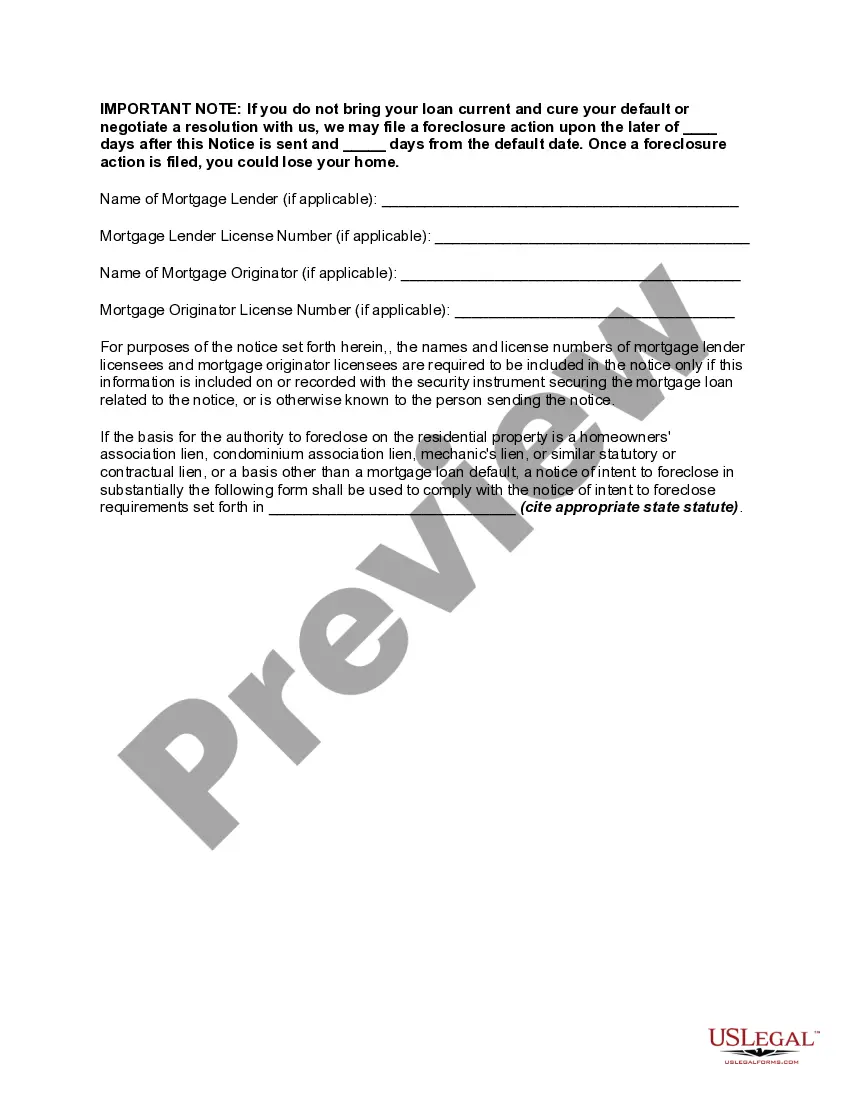

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Utah Notice of Intent to Foreclose — Mortgage Loan Default: A Comprehensive Overview Keywords: Utah, Notice of Intent, Foreclose, Mortgage Loan Default Introduction: A Utah Notice of Intent to Foreclose — Mortgage Loan Default is a legal document issued by a lender or mortgage holder to inform a borrower that their mortgage loan is in default and that foreclosure proceedings may begin if the default is not resolved. This notice serves as a formal communication to the borrower, explaining the consequences of failing to fulfill their mortgage obligations. Types: 1. Utah Notice of Intent to Foreclose — Non-Judicial: In Utah, as in many states, the foreclosure process is primarily non-judicial, meaning it does not require court intervention unless contested by the borrower. In such cases, the lender issues a Notice of Intent to Foreclose to the borrower, setting a timeframe for resolution before foreclosure proceedings commence. 2. Utah Notice of Intent to Foreclose — Judicial: In rare situations where the foreclosure process becomes judicial, the lender may file a lawsuit against the borrower, initiating a court case. The Notice of Intent to Foreclose is still issued to the borrower, but the legal process in this case will involve court hearings and proceedings. Key Elements of the Utah Notice of Intent to Foreclose: 1. Borrower's Information: The notice includes the borrower's name, address, and contact details. It confirms the identification of the individual or entity receiving the notice. 2. Lender's Information: The lender's name, contact details, and authorized representative's information are provided. This ensures clear communication channels between the lender and borrower during the resolution process. 3. Loan Details: The notice includes the mortgage loan number, the date of origination, and the amount borrowed. These details help verify the specific loan in default and provide a clear understanding of the financial obligations involved. 4. Payment Default Information: This section clearly outlines the defaulted loan payment(s), including the date(s) of failure, outstanding balance, and late fees accrued. The borrower will be informed of the specific defaults that triggered the notice. 5. Right to Cure: The notice explains the borrower's right to cure the default by paying the delinquent amount within a specified timeframe. It provides information on where and how to make the payment to resolve the default. 6. Foreclosure Process Information: In this section, the notice details the consequences of failing to cure the default. It explains that the lender may initiate foreclosure proceedings after the cure period expires, leading to eviction and potential loss of property ownership. 7. Contact Information: The notice includes contact information for the lender's representative or loan service, enabling the borrower to communicate and seek assistance in resolving the default before foreclosure becomes inevitable. Conclusion: A Utah Notice of Intent to Foreclose — Mortgage Loan Default is a vital legal document that serves as a warning to borrowers that their mortgage loan is in default and that foreclosure procedures may be initiated. Understanding the contents and implications of this notice is crucial for borrowers in Utah as it provides an opportunity to resolve their defaulted mortgage and avoid the potentially severe consequences of foreclosure.Utah Notice of Intent to Foreclose — Mortgage Loan Default: A Comprehensive Overview Keywords: Utah, Notice of Intent, Foreclose, Mortgage Loan Default Introduction: A Utah Notice of Intent to Foreclose — Mortgage Loan Default is a legal document issued by a lender or mortgage holder to inform a borrower that their mortgage loan is in default and that foreclosure proceedings may begin if the default is not resolved. This notice serves as a formal communication to the borrower, explaining the consequences of failing to fulfill their mortgage obligations. Types: 1. Utah Notice of Intent to Foreclose — Non-Judicial: In Utah, as in many states, the foreclosure process is primarily non-judicial, meaning it does not require court intervention unless contested by the borrower. In such cases, the lender issues a Notice of Intent to Foreclose to the borrower, setting a timeframe for resolution before foreclosure proceedings commence. 2. Utah Notice of Intent to Foreclose — Judicial: In rare situations where the foreclosure process becomes judicial, the lender may file a lawsuit against the borrower, initiating a court case. The Notice of Intent to Foreclose is still issued to the borrower, but the legal process in this case will involve court hearings and proceedings. Key Elements of the Utah Notice of Intent to Foreclose: 1. Borrower's Information: The notice includes the borrower's name, address, and contact details. It confirms the identification of the individual or entity receiving the notice. 2. Lender's Information: The lender's name, contact details, and authorized representative's information are provided. This ensures clear communication channels between the lender and borrower during the resolution process. 3. Loan Details: The notice includes the mortgage loan number, the date of origination, and the amount borrowed. These details help verify the specific loan in default and provide a clear understanding of the financial obligations involved. 4. Payment Default Information: This section clearly outlines the defaulted loan payment(s), including the date(s) of failure, outstanding balance, and late fees accrued. The borrower will be informed of the specific defaults that triggered the notice. 5. Right to Cure: The notice explains the borrower's right to cure the default by paying the delinquent amount within a specified timeframe. It provides information on where and how to make the payment to resolve the default. 6. Foreclosure Process Information: In this section, the notice details the consequences of failing to cure the default. It explains that the lender may initiate foreclosure proceedings after the cure period expires, leading to eviction and potential loss of property ownership. 7. Contact Information: The notice includes contact information for the lender's representative or loan service, enabling the borrower to communicate and seek assistance in resolving the default before foreclosure becomes inevitable. Conclusion: A Utah Notice of Intent to Foreclose — Mortgage Loan Default is a vital legal document that serves as a warning to borrowers that their mortgage loan is in default and that foreclosure procedures may be initiated. Understanding the contents and implications of this notice is crucial for borrowers in Utah as it provides an opportunity to resolve their defaulted mortgage and avoid the potentially severe consequences of foreclosure.