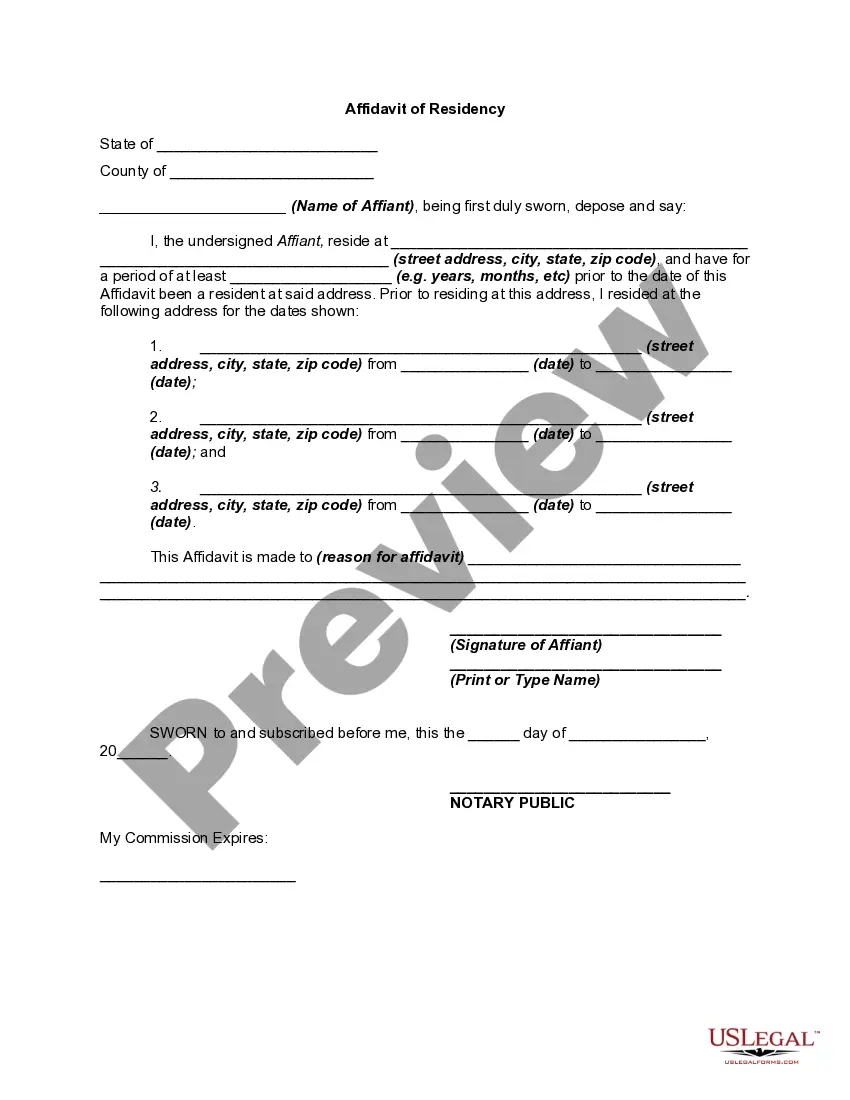

Utah Proof of Residency for Mortgage

Description

How to fill out Proof Of Residency For Mortgage?

Have you been in the place the place you need paperwork for sometimes company or person purposes nearly every day? There are a lot of lawful papers layouts available online, but finding versions you can rely is not straightforward. US Legal Forms offers a large number of kind layouts, just like the Utah Proof of Residency for Mortgage, which can be composed to satisfy federal and state specifications.

If you are already informed about US Legal Forms site and possess an account, simply log in. After that, you may obtain the Utah Proof of Residency for Mortgage web template.

If you do not have an profile and wish to begin using US Legal Forms, follow these steps:

- Find the kind you require and ensure it is for the appropriate town/county.

- Take advantage of the Review button to check the shape.

- See the explanation to ensure that you have chosen the right kind.

- In case the kind is not what you are looking for, utilize the Lookup industry to obtain the kind that meets your needs and specifications.

- If you discover the appropriate kind, just click Purchase now.

- Opt for the costs plan you desire, complete the necessary information and facts to create your account, and purchase the transaction making use of your PayPal or Visa or Mastercard.

- Pick a handy data file file format and obtain your duplicate.

Get each of the papers layouts you have bought in the My Forms menus. You can get a additional duplicate of Utah Proof of Residency for Mortgage any time, if required. Just select the required kind to obtain or print the papers web template.

Use US Legal Forms, one of the most substantial collection of lawful varieties, to save lots of time as well as steer clear of faults. The support offers professionally manufactured lawful papers layouts which can be used for a variety of purposes. Create an account on US Legal Forms and initiate producing your lifestyle easier.

Form popularity

FAQ

Don't worry if your mailing address on your W-2 form is wrong or has since changed. This won't affect your taxes.

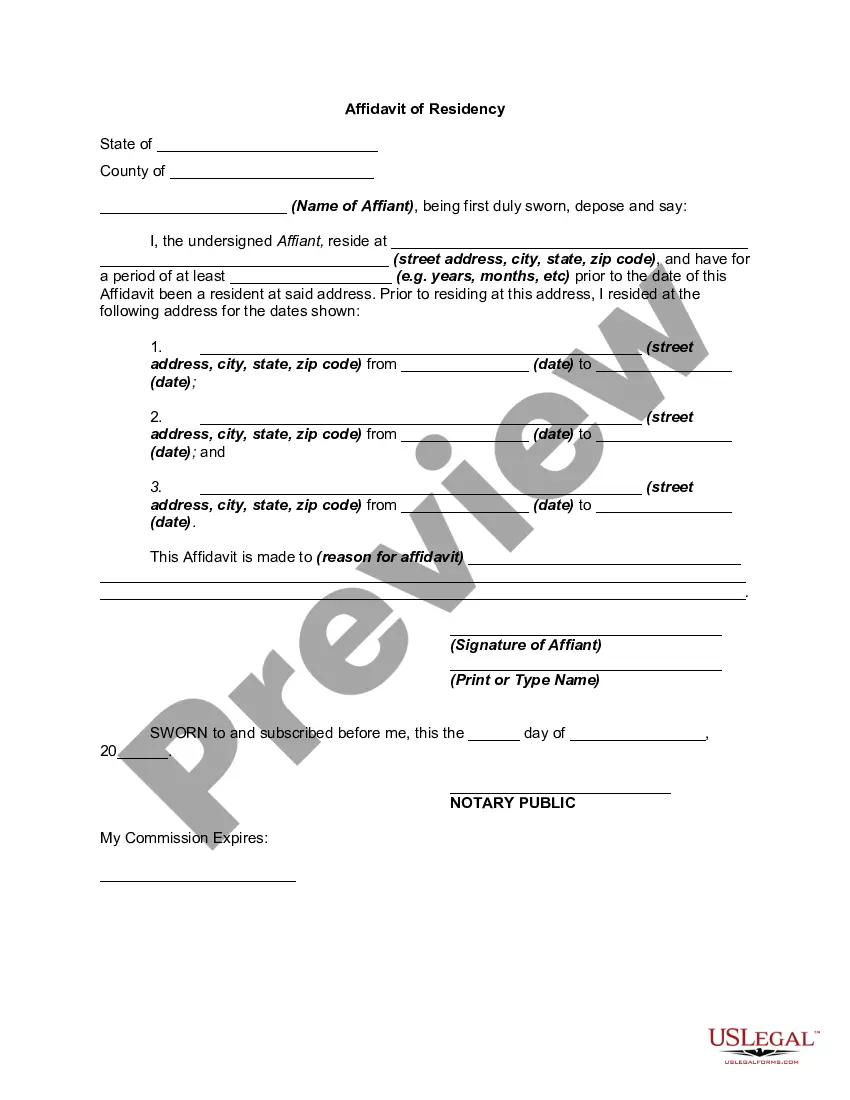

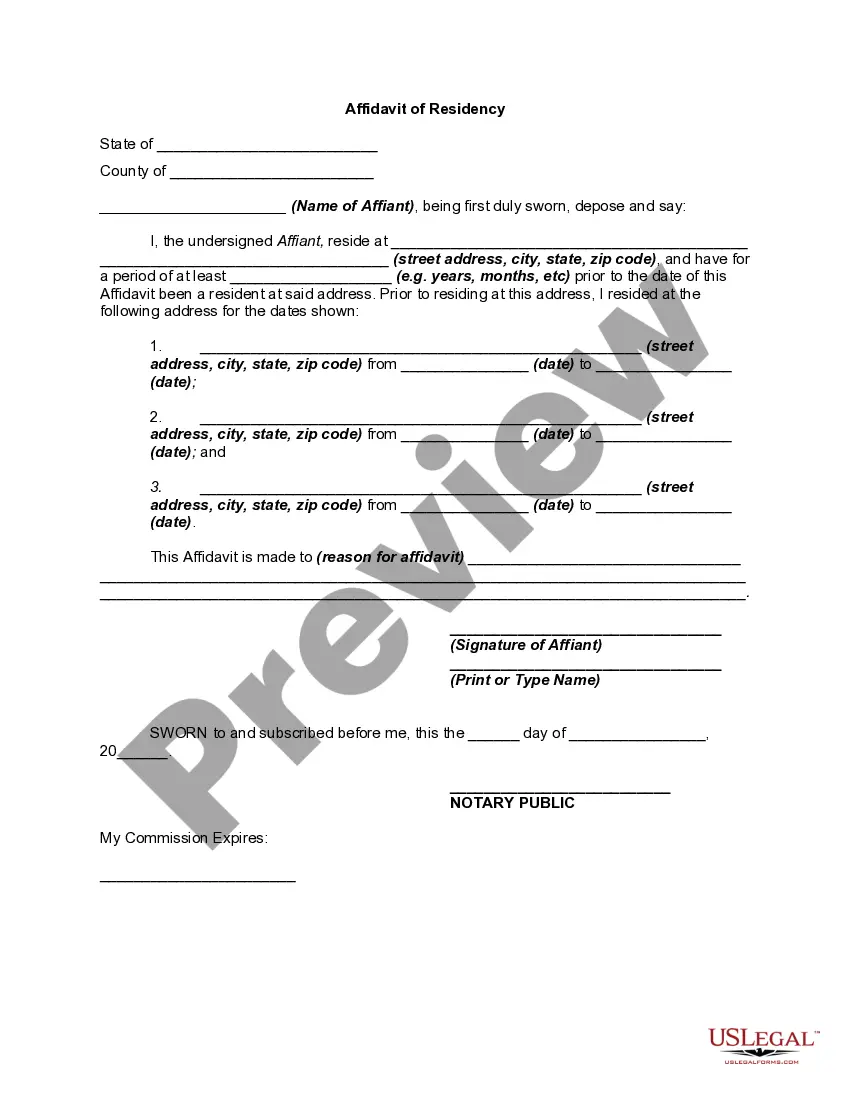

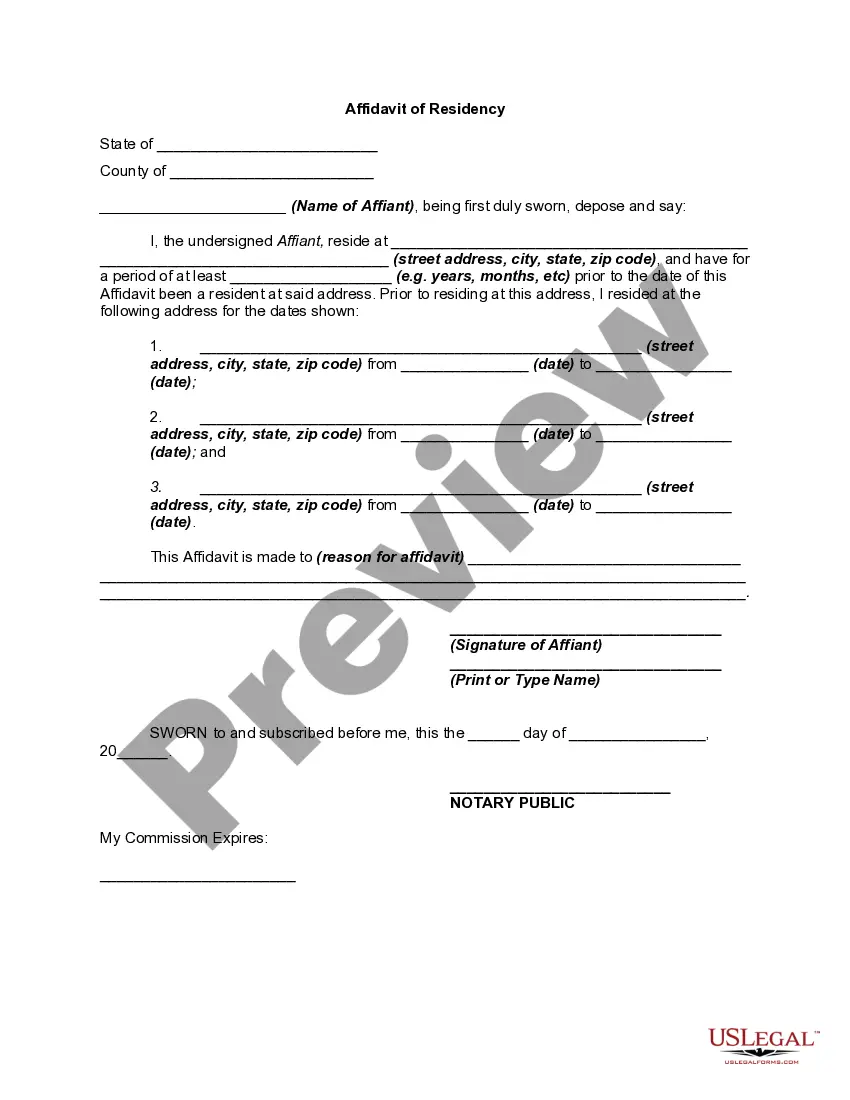

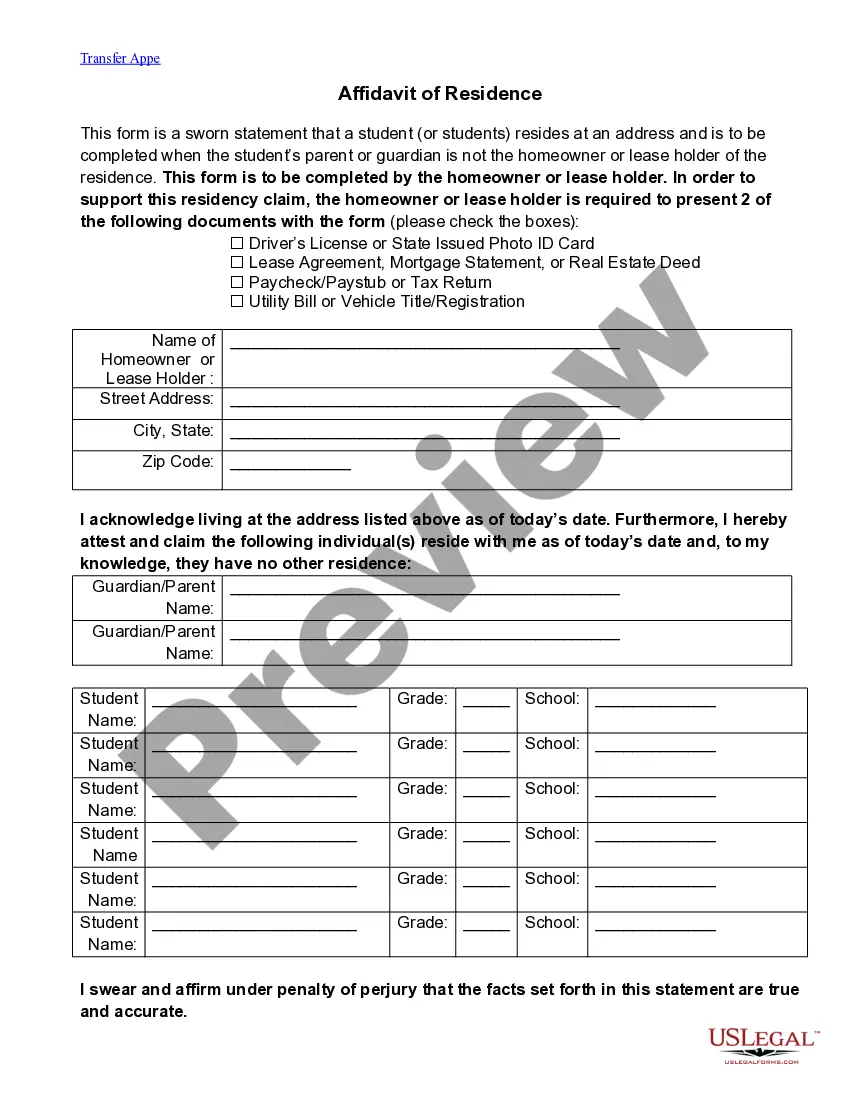

Must display the applicant's name and principal Utah residence address which may include a bank statement, court documents, current mortgage or rental contract, major credit card bill, property tax notice statement or receipt, school transcript, utility bill, or vehicle title.

Utah residency requirements involve verification of your Social Security card, a W-2 form, an SSA-1099 form, a pay stub with your name, or a non-SSA-1099 form. If you own a vehicle, you will need to show you have a current Utah vehicle registration when you file your Utah residency application.

Some of the documents that can be used to establish proof of residency include: Utility bills. W-2's and other tax forms or tax returns. Paycheck or pay stub.

A utility bill, credit card statement, lease agreement or mortgage statement will all work to prove residency. If you've gone paperless, print a billing statement from your online account.

Bring proof of identity (name and date of birth.) Bring social security card. Bring two (2) documents of Utah residence address. Visit our Required Documentation page for what is acceptable proof of each type of document required.

The IRS matches your name and Social Security number to their database, but not your address. Use your current address on your personal income tax return.

Some documents that may work are: ? California state income taxes forms from the previous year ? W-2 form showing a California physical address ? Mortgage, title or rental agreements showing the physical address where the student lives ? Utility or other bills showing a California physical address ? California voter ...