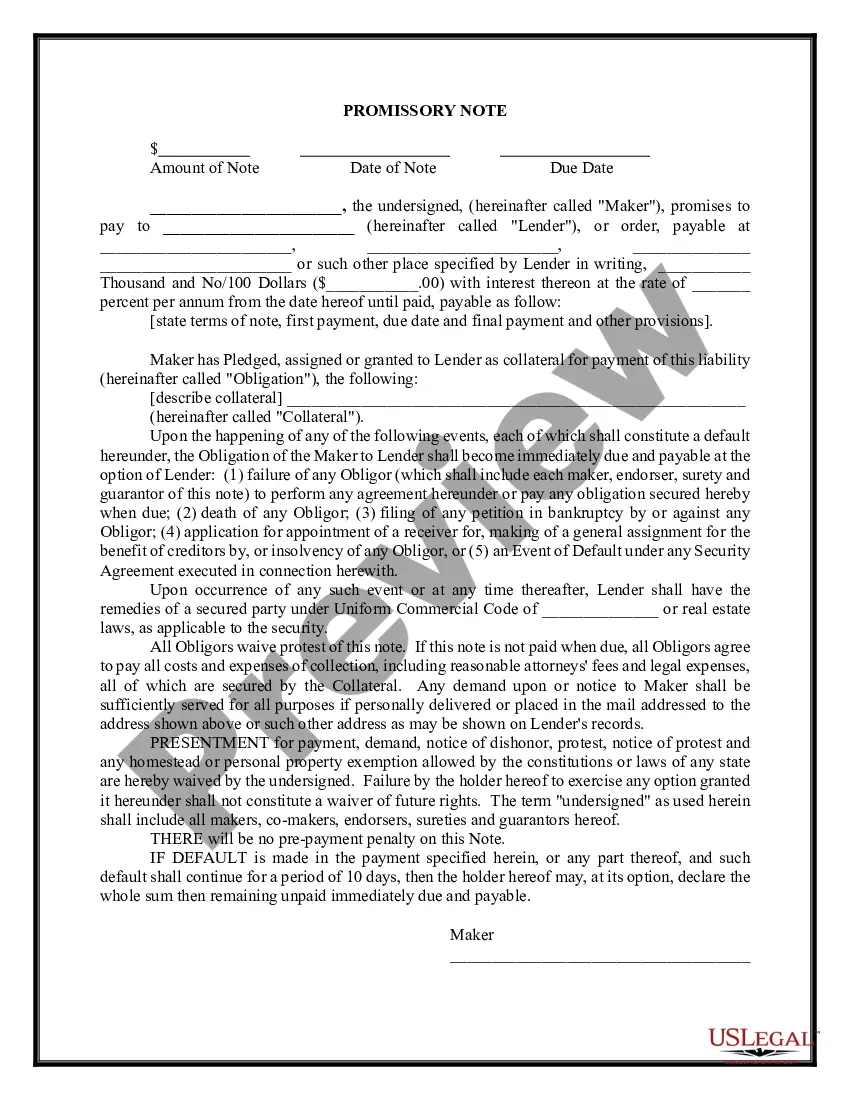

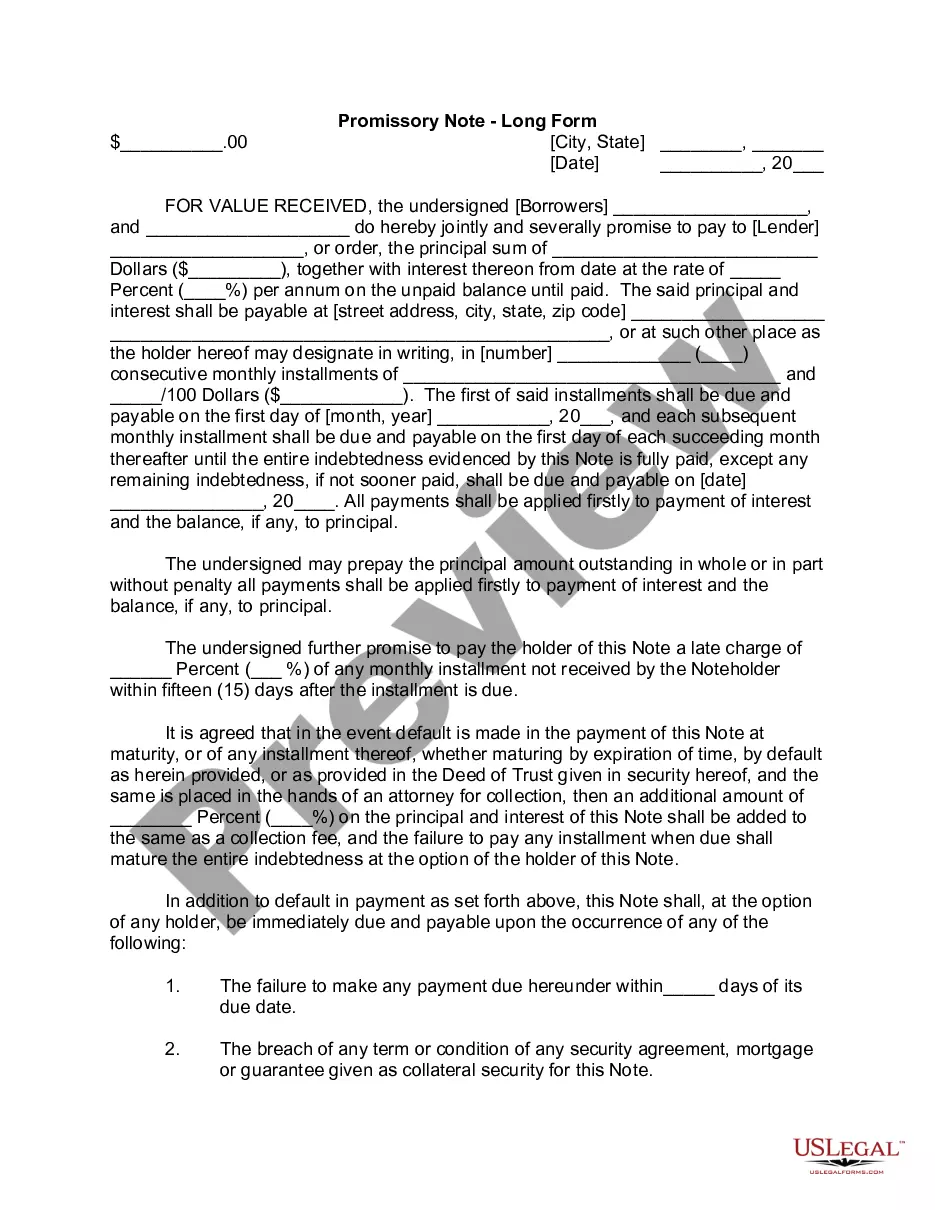

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

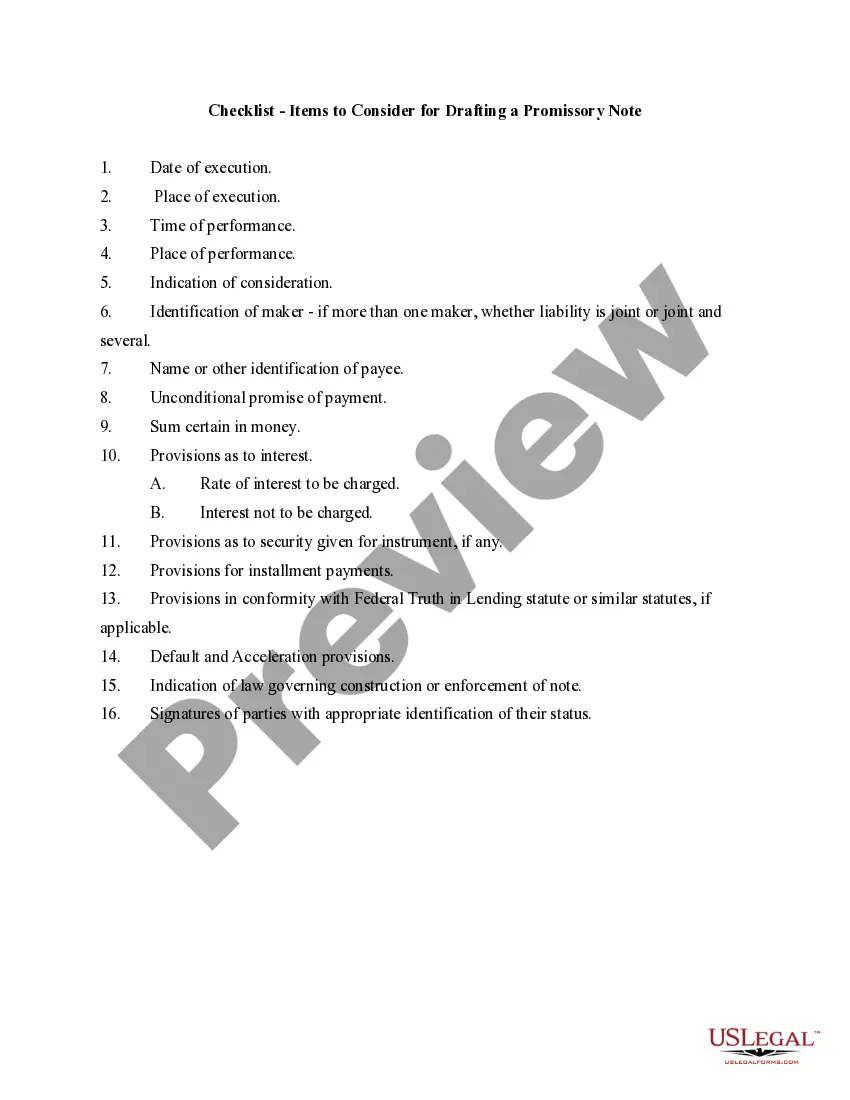

Utah Checklist - Items to Consider for Drafting a Promissory Note

Category:

State:

Multi-State

Control #:

US-03060BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Checklist - Items To Consider For Drafting A Promissory Note?

You can invest several hours online trying to locate the legal document template that complies with the federal and state requirements you need. US Legal Forms offers thousands of legal forms that have been evaluated by professionals.

You can easily obtain or print the Utah Checklist - Items to Consider for Drafting a Promissory Note from their services.

If you already possess a US Legal Forms account, you can Log In and select the Download option. After that, you can complete, modify, print, or sign the Utah Checklist - Items to Consider for Drafting a Promissory Note. Every legal document template you acquire is yours indefinitely.

Complete the transaction. You may use your credit card or PayPal account to pay for the legal form. Download the format of your document and save it to your device. Make adjustments to your document if necessary. You can complete, modify, sign, and print the Utah Checklist - Items to Consider for Drafting a Promissory Note. Obtain and print thousands of document templates using the US Legal Forms website, which offers the largest selection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- To access another version of the purchased form, navigate to the My documents tab and choose the corresponding option.

- If you are using the US Legal Forms website for the first time, follow the basic instructions below.

- First, ensure that you have selected the correct document template for the state/city of your choice. Review the form summary to ensure you have chosen the correct type.

- If available, utilize the Preview option to review the document template as well.

- If you wish to locate another version of your form, use the Search field to find the template that suits your needs and specifications.

- Once you have found the template you desire, click Purchase now to proceed.

- Select the pricing plan you want, enter your details, and sign up for a free account on US Legal Forms.

Form popularity

FAQ

A promissory note can be deemed invalid for several reasons. For instance, if it lacks essential components like the signature of the borrower or the clearly stated repayment terms, it could lead to complications. Additionally, if the note is not executed voluntarily, it may not hold up in court. To ensure validity, refer to the Utah Checklist - Items to Consider for Drafting a Promissory Note for guidance, and consider using platforms like US Legal Forms to create compliant documents.

Certain elements are indispensable in every promissory note you create. It must state the amount borrowed, the repayment schedule, and the consequences of non-payment. By incorporating these foundational elements, you comply with the Utah Checklist - Items to Consider for Drafting a Promissory Note, thus solidifying the note's authenticity.

A promissory note should possess several key elements to serve its purpose. These include the principal amount, interest rate, repayment terms, and the date of issuance. To promote clarity and legality, following the Utah Checklist - Items to Consider for Drafting a Promissory Note can enhance the effectiveness of your document.

The rules for promissory notes dictate that the agreement must be in writing, must specify the payment terms, and require proper signatures from both parties. Additionally, the terms should be clear to avoid disputes in the future. By referring to the Utah Checklist - Items to Consider for Drafting a Promissory Note, you can ensure compliance with these essential rules.

The conditions for a promissory note generally include a written document, clear terms for repayment, and signed consent from all parties involved. The note must also specify the interest rate, if applicable. By utilizing the Utah Checklist - Items to Consider for Drafting a Promissory Note, you can verify that these conditions are properly met.

Yes, consideration is a necessary element for a promissory note. It refers to something of value exchanged between parties, making the agreement enforceable. In the context of the Utah Checklist - Items to Consider for Drafting a Promissory Note, ensuring there is valid consideration is crucial for legal standing.

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan.

There is no legal requirement to have a Utah promissory note notarized. To execute the note, the borrower and any co-signer to the loan must sign and date the agreement.

Acceptance is not an essential requirement of a valid promissory note.

Signatures. Generally, promissory notes do not need to be notarized. Typically, legally enforceable promissory notes must be signed by individuals and contain unconditional promises to pay specific amounts of money. Generally, they also state due dates for payment and an agreed-upon interest rate.