Utah Mortgage Note

Description

How to fill out Mortgage Note?

Choosing the best lawful record format can be quite a struggle. Obviously, there are plenty of themes available on the net, but how would you obtain the lawful type you will need? Use the US Legal Forms web site. The assistance gives thousands of themes, including the Utah Mortgage Note, that can be used for organization and private requirements. Every one of the varieties are examined by professionals and satisfy federal and state needs.

When you are already authorized, log in for your profile and click the Obtain key to obtain the Utah Mortgage Note. Use your profile to look with the lawful varieties you have bought earlier. Check out the My Forms tab of your own profile and obtain yet another copy from the record you will need.

When you are a new consumer of US Legal Forms, allow me to share easy directions so that you can follow:

- Initial, ensure you have chosen the appropriate type for your area/state. It is possible to check out the shape using the Preview key and read the shape outline to make sure it is the best for you.

- In case the type will not satisfy your needs, use the Seach discipline to get the proper type.

- When you are sure that the shape would work, go through the Get now key to obtain the type.

- Opt for the rates prepare you want and enter in the essential information. Build your profile and pay for the transaction utilizing your PayPal profile or bank card.

- Choose the submit formatting and down load the lawful record format for your system.

- Full, revise and print out and sign the received Utah Mortgage Note.

US Legal Forms is the greatest local library of lawful varieties where you can discover different record themes. Use the service to down load appropriately-created paperwork that follow state needs.

Form popularity

FAQ

Because there are secured and unsecured loans, you can have a promissory note without a mortgage ? which is considered an unsecured loan. However, you typically can't have a mortgage without a promissory note, ing to Chase Bank. The promissory note is a crucial legal document to protect the lender.

Deeds of trust are the most common instrument used in the financing of real estate purchases in Alaska, Arizona, California, Colorado, the District of Columbia, Idaho, Maryland, Mississippi, Missouri, Montana, Nebraska, Nevada, North Carolina, Oregon, Tennessee, Texas, Utah, Virginia, Washington, and West Virginia, ...

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.

The mortgage is not an ownership interest for the lender?it is just a vehicle that the lender uses to foreclose, if needed. Because of that, any person on the deed must sign and be on the mortgage. However, someone can be on the mortgage, but not be someone who is on the promissory note.

The Court's holding requires that prior to the assignee of a mortgage loan filing suit on the note or mortgage, the assignee must have received both an allonge/assignment of the note and an assignment of the mortgage.

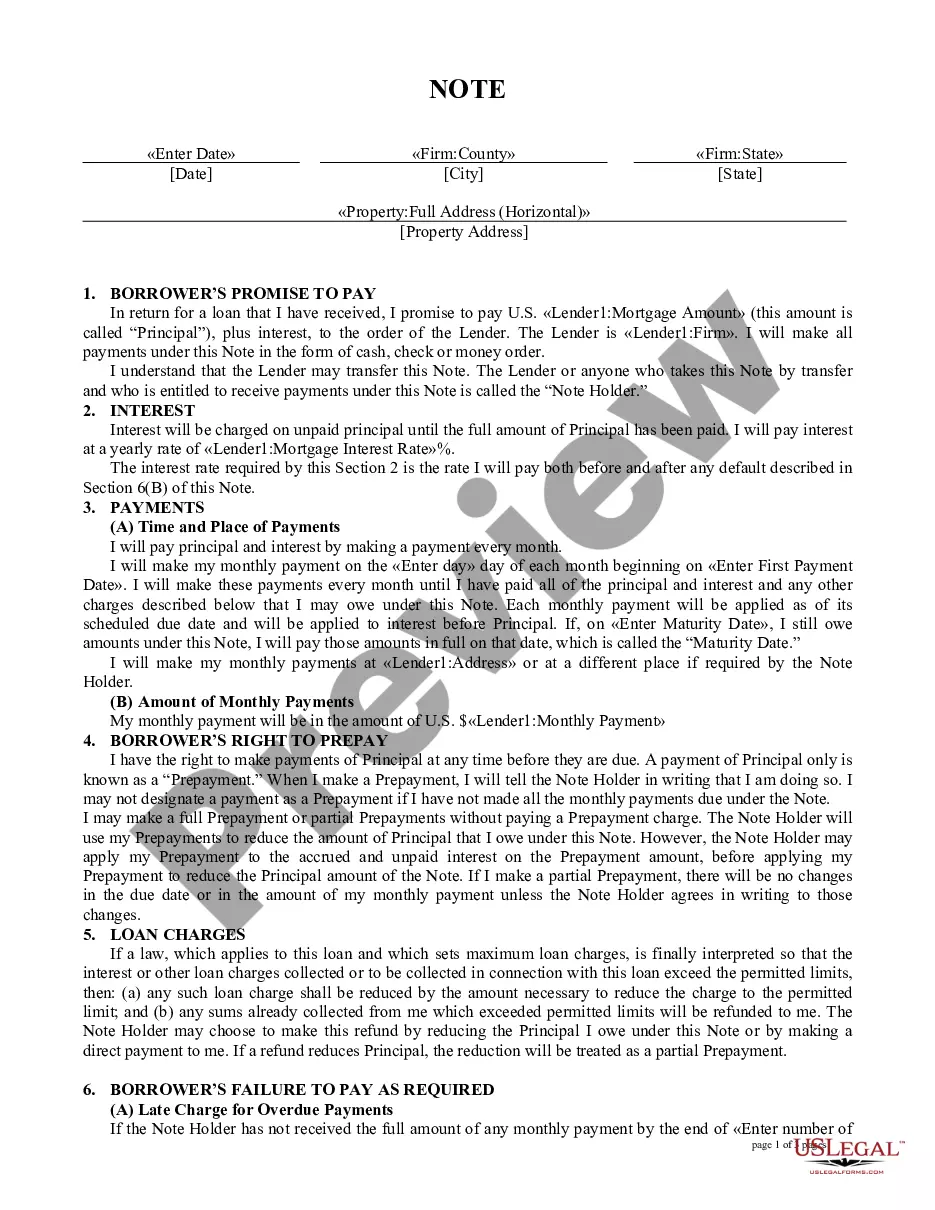

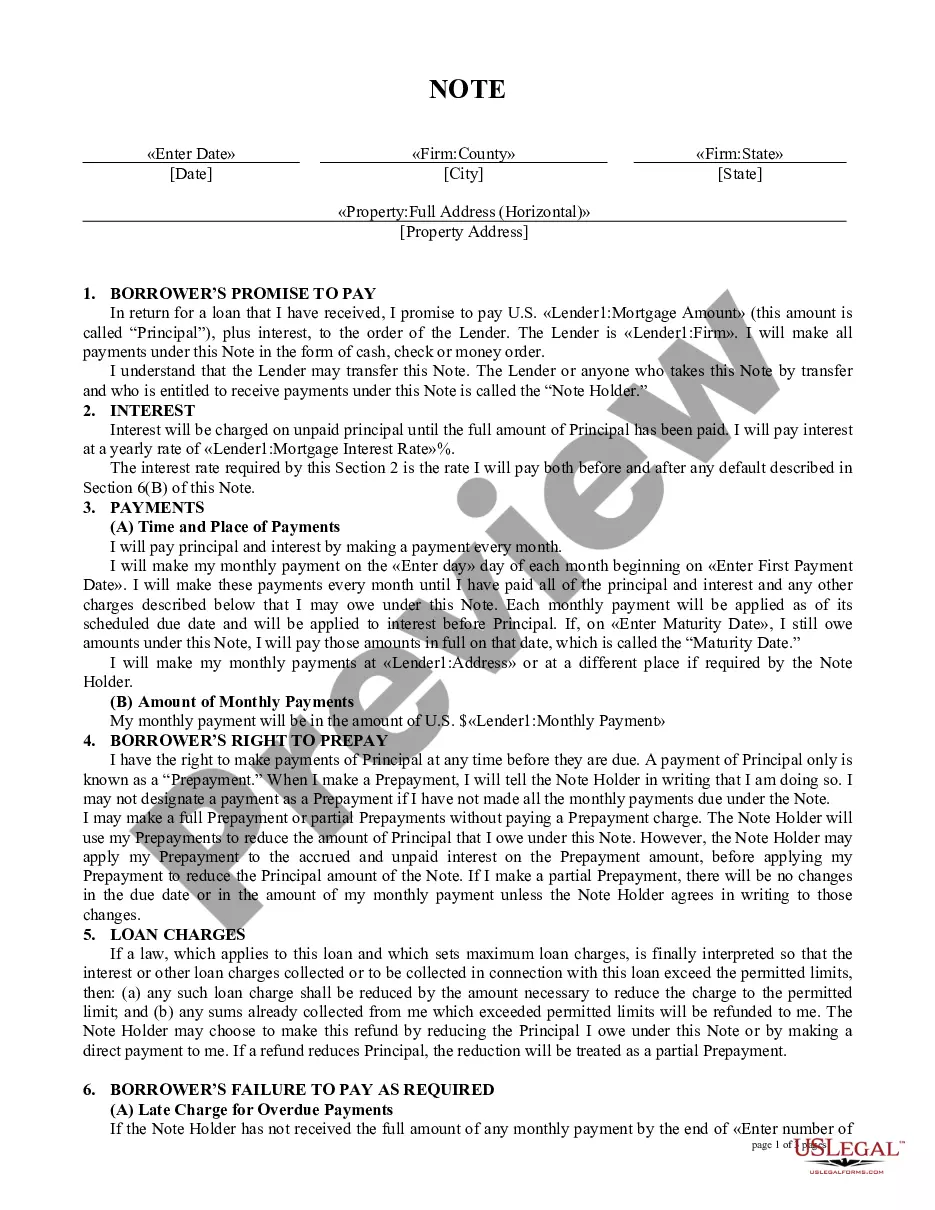

A mortgage is a type of contract. What makes it special is that it's a loan secured by real estate. A mortgage note is the document that you sign at the end of your home closing. It should accurately reflect all the terms of the agreement between the borrower and the lender or be corrected immediately if it doesn't.

All mortgage notes will contain the following information: Amount Borrowed. This is the total amount you owe on the mortgage. Interest Rate. Early in the mortgage application process an interest rate is locked-in by the buyer. ... Down Payment Amount. ... Name of Borrower. ... Name of Lender. ... Repayment Plan. ... Failure to Repay.

Promissory Note Vs. Mortgage. A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.