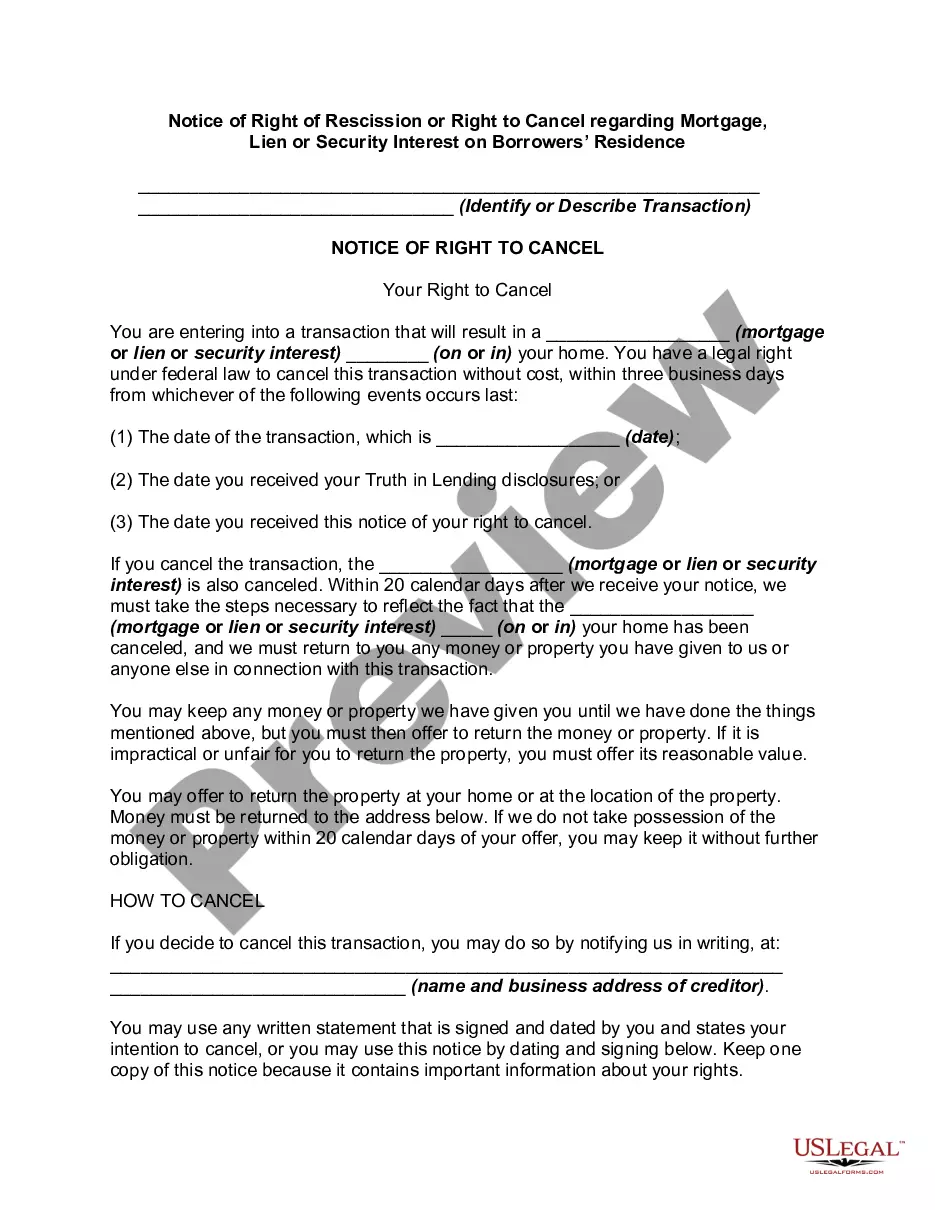

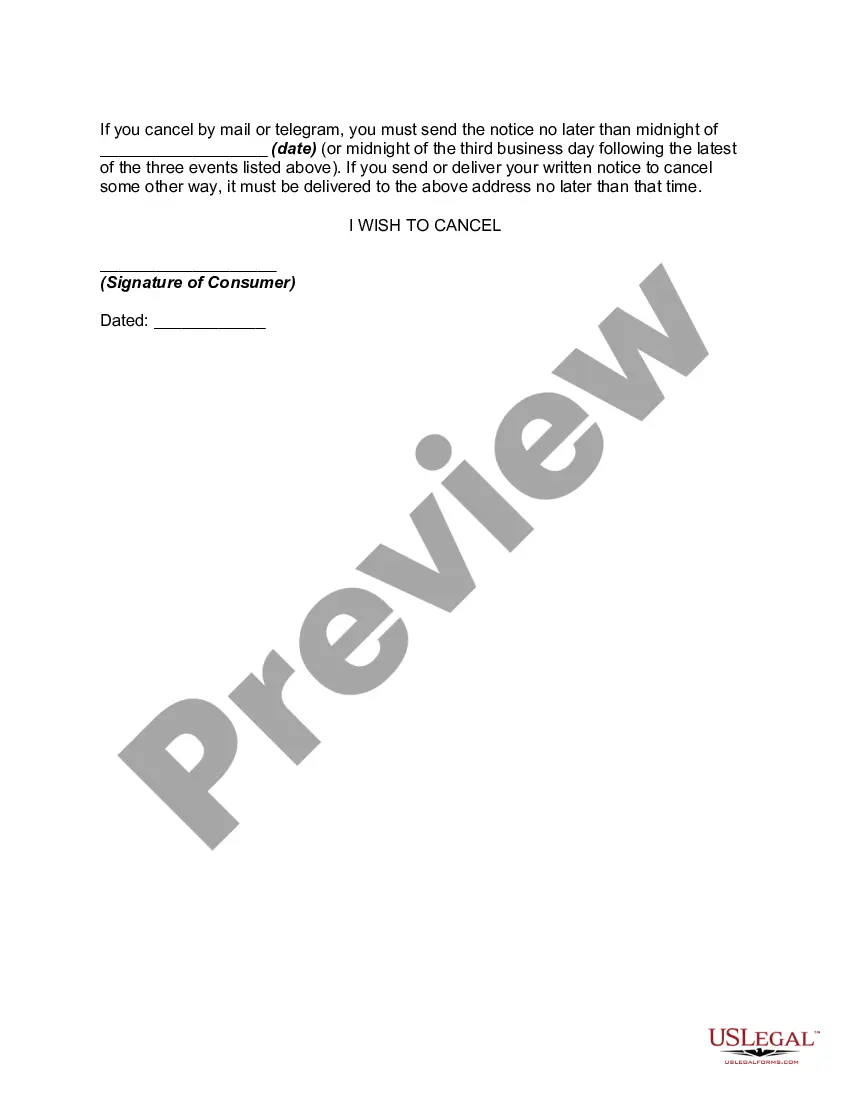

According to 12 CFR 226.23, in a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership interest is or will be subject to the security interest shall have the right to rescind the transaction, with some exceptions. To exercise the right to rescind, the consumer shall notify the creditor of the rescission by mail, telegram or other means of written communication. Notice is considered given when mailed, when filed for telegraphic transmission or, if sent by other means, when delivered to the creditor's designated place of business. The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice required by paragraph (b) of this section, or delivery of all material disclosures, whichever occurs last.

Utah Notice of Right of Rescission or Right to Cancel Regarding Mortgage, Lien, or Security Interest on Borrowers' Residence Explained In the state of Utah, borrowers enjoy certain protections and rights when it comes to their mortgage, lien, or security interest on their residence. The Utah Notice of Right of Rescission or Right to Cancel aims to provide borrowers with the opportunity to review and reconsider their decision to enter into a financial agreement and potentially cancel it within a specified timeframe. This detailed description will shed light on the purpose of the notice, the applicable regulations, and the different types of rescission or cancellation rights available to borrowers in Utah. The Utah Notice of Right of Rescission or Right to Cancel applies to various transactions associated with mortgages, liens, or security interests on borrowers' residences, primarily including home loans or refinancing agreements secured by the borrower's primary dwelling. The purpose of this notice is to give borrowers the chance to carefully review all the terms and conditions of these agreements and to enable them to withdraw from the transaction if desired, without facing any penalty or unfavorable consequences. One significant aspect of the Utah Notice of Right of Rescission or Right to Cancel is the specified timeframe within which borrowers can exercise their right to rescind or cancel the mortgage, lien, or security interest. In most cases, Utah law provides borrowers with three business days, excluding Sundays and federal holidays, starting from the date of the transaction or the receipt of the notice, to exercise their right to cancel without facing any financial liability. However, it is crucial for borrowers to understand that this right is not applicable to all types of transactions. Different types of Utah Notice of Right of Rescission or Right to Cancel may apply depending on the circumstances. Some common examples include: 1. Traditional Mortgage Loan: When borrowers obtain a traditional mortgage loan, be it for purchasing a home or refinancing an existing mortgage, they typically have three business days to review the terms, conditions, and associated costs before finalizing the agreement. If the borrowers decide to cancel during this period, they need to submit a written notice to the lender or service expressing their wish to exercise their right to rescind. 2. Home Equity Loan or Line of Credit: Borrowers in Utah who secure a home equity loan or open a home equity line of credit (HELOT) may also be entitled to a right of rescission. The timeframe for these types of transactions typically follows the same three-business-day rule, allowing borrowers to reconsider their decision to borrow against the equity in their home. It is important for borrowers to carefully read and understand the terms of any agreement they enter into regarding their mortgage, lien, or security interest on their residence. This will ensure they are fully informed about their rights and any applicable provisions for rescission or cancellation. If borrowers decide to exercise their right to rescind or cancel, they must do so before the specified deadline by providing written notice to the lender, mortgage company, or service involved in the transaction. In conclusion, the Utah Notice of Right of Rescission or Right to Cancel provides crucial safeguards for borrowers, allowing them to review, reconsider, and potentially cancel mortgage, lien, or security interest agreements on their residences within a specified timeframe. By understanding these rights, borrowers can confidently navigate the lending process and make informed decisions regarding their homeownership journey.Utah Notice of Right of Rescission or Right to Cancel Regarding Mortgage, Lien, or Security Interest on Borrowers' Residence Explained In the state of Utah, borrowers enjoy certain protections and rights when it comes to their mortgage, lien, or security interest on their residence. The Utah Notice of Right of Rescission or Right to Cancel aims to provide borrowers with the opportunity to review and reconsider their decision to enter into a financial agreement and potentially cancel it within a specified timeframe. This detailed description will shed light on the purpose of the notice, the applicable regulations, and the different types of rescission or cancellation rights available to borrowers in Utah. The Utah Notice of Right of Rescission or Right to Cancel applies to various transactions associated with mortgages, liens, or security interests on borrowers' residences, primarily including home loans or refinancing agreements secured by the borrower's primary dwelling. The purpose of this notice is to give borrowers the chance to carefully review all the terms and conditions of these agreements and to enable them to withdraw from the transaction if desired, without facing any penalty or unfavorable consequences. One significant aspect of the Utah Notice of Right of Rescission or Right to Cancel is the specified timeframe within which borrowers can exercise their right to rescind or cancel the mortgage, lien, or security interest. In most cases, Utah law provides borrowers with three business days, excluding Sundays and federal holidays, starting from the date of the transaction or the receipt of the notice, to exercise their right to cancel without facing any financial liability. However, it is crucial for borrowers to understand that this right is not applicable to all types of transactions. Different types of Utah Notice of Right of Rescission or Right to Cancel may apply depending on the circumstances. Some common examples include: 1. Traditional Mortgage Loan: When borrowers obtain a traditional mortgage loan, be it for purchasing a home or refinancing an existing mortgage, they typically have three business days to review the terms, conditions, and associated costs before finalizing the agreement. If the borrowers decide to cancel during this period, they need to submit a written notice to the lender or service expressing their wish to exercise their right to rescind. 2. Home Equity Loan or Line of Credit: Borrowers in Utah who secure a home equity loan or open a home equity line of credit (HELOT) may also be entitled to a right of rescission. The timeframe for these types of transactions typically follows the same three-business-day rule, allowing borrowers to reconsider their decision to borrow against the equity in their home. It is important for borrowers to carefully read and understand the terms of any agreement they enter into regarding their mortgage, lien, or security interest on their residence. This will ensure they are fully informed about their rights and any applicable provisions for rescission or cancellation. If borrowers decide to exercise their right to rescind or cancel, they must do so before the specified deadline by providing written notice to the lender, mortgage company, or service involved in the transaction. In conclusion, the Utah Notice of Right of Rescission or Right to Cancel provides crucial safeguards for borrowers, allowing them to review, reconsider, and potentially cancel mortgage, lien, or security interest agreements on their residences within a specified timeframe. By understanding these rights, borrowers can confidently navigate the lending process and make informed decisions regarding their homeownership journey.