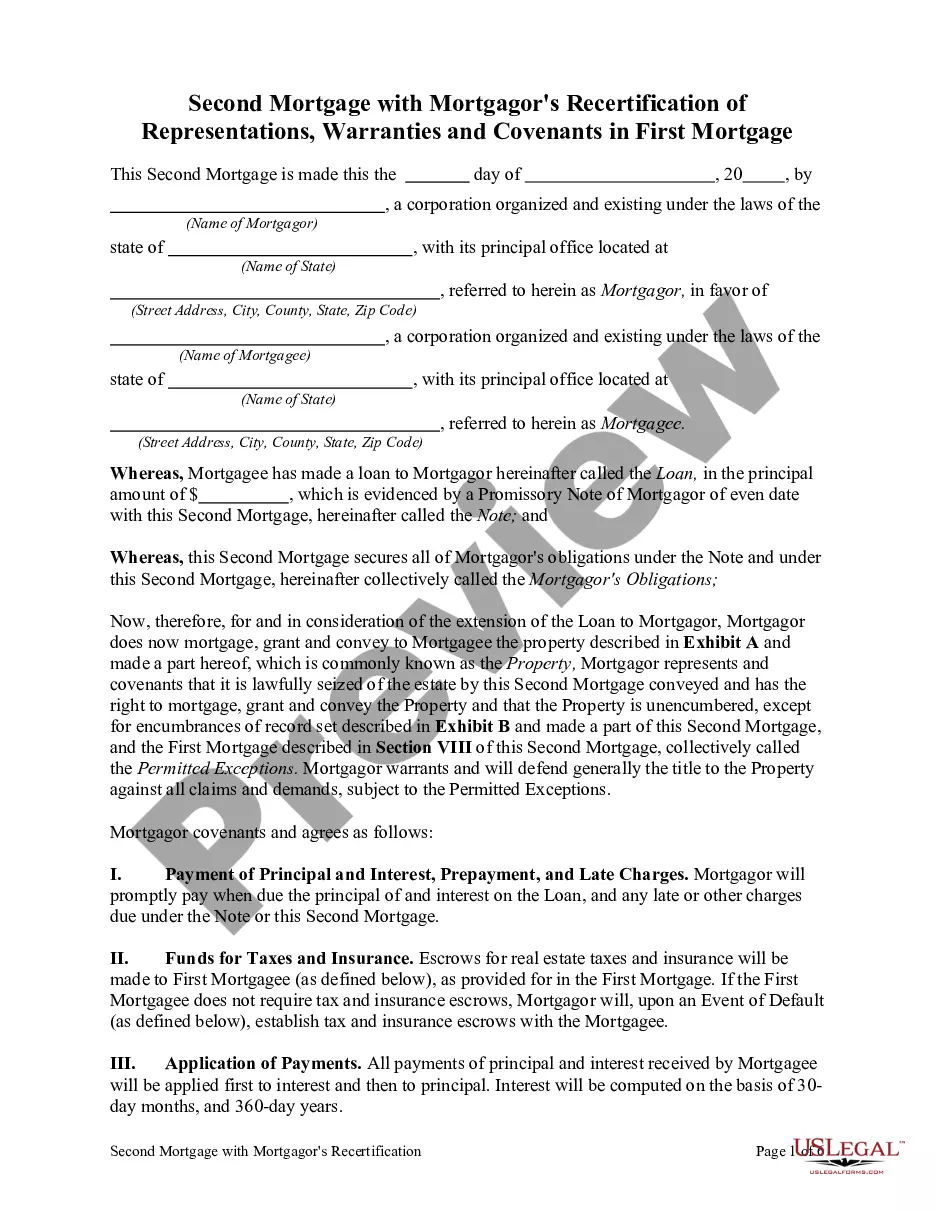

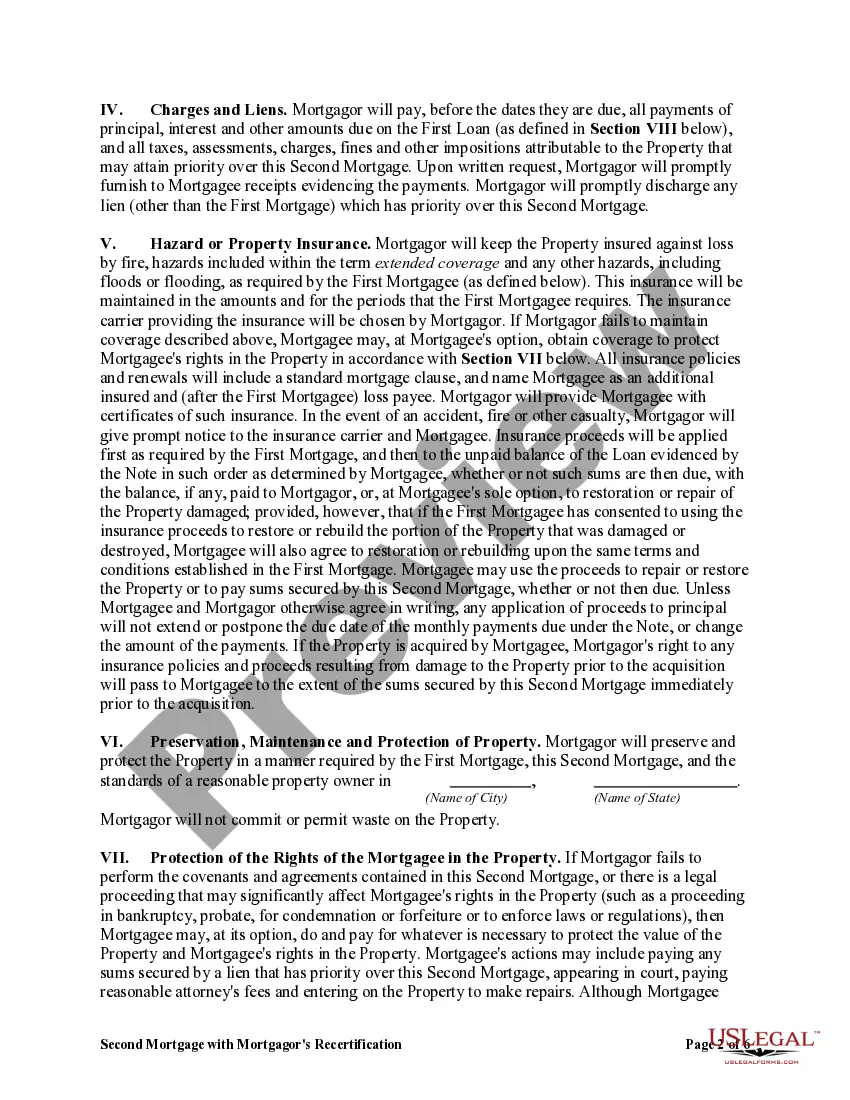

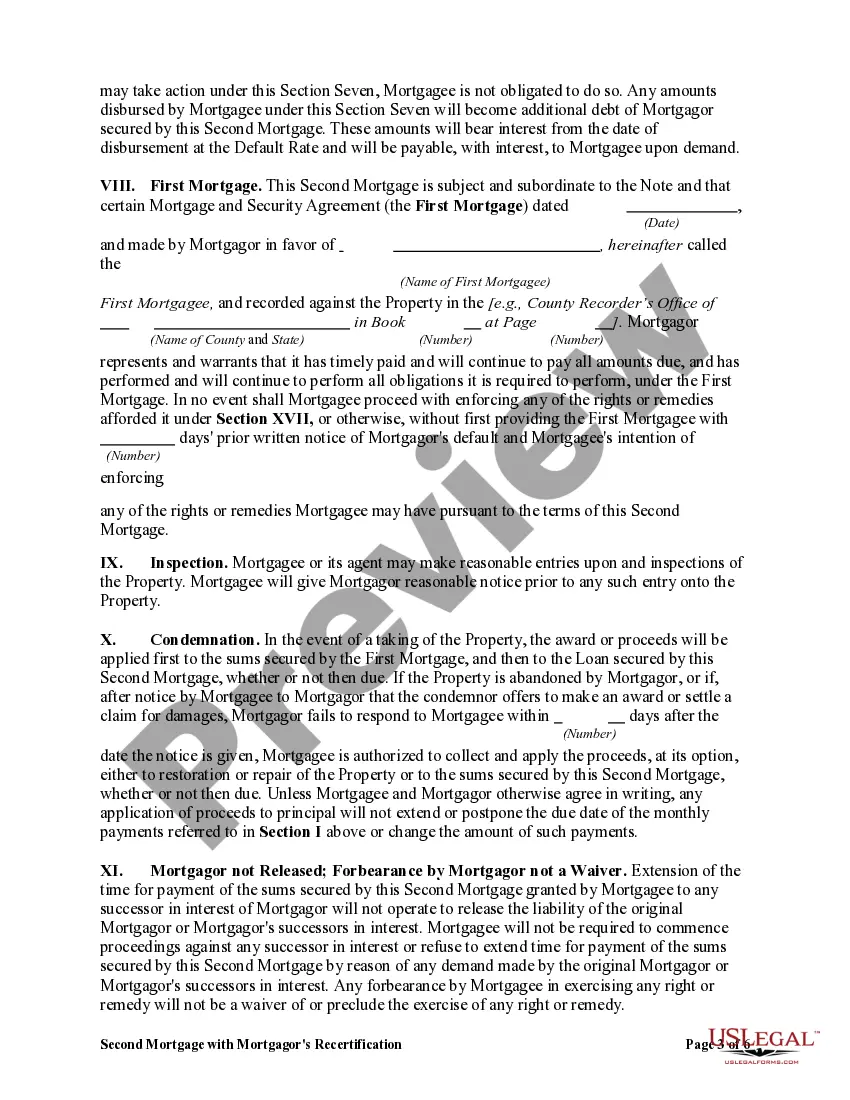

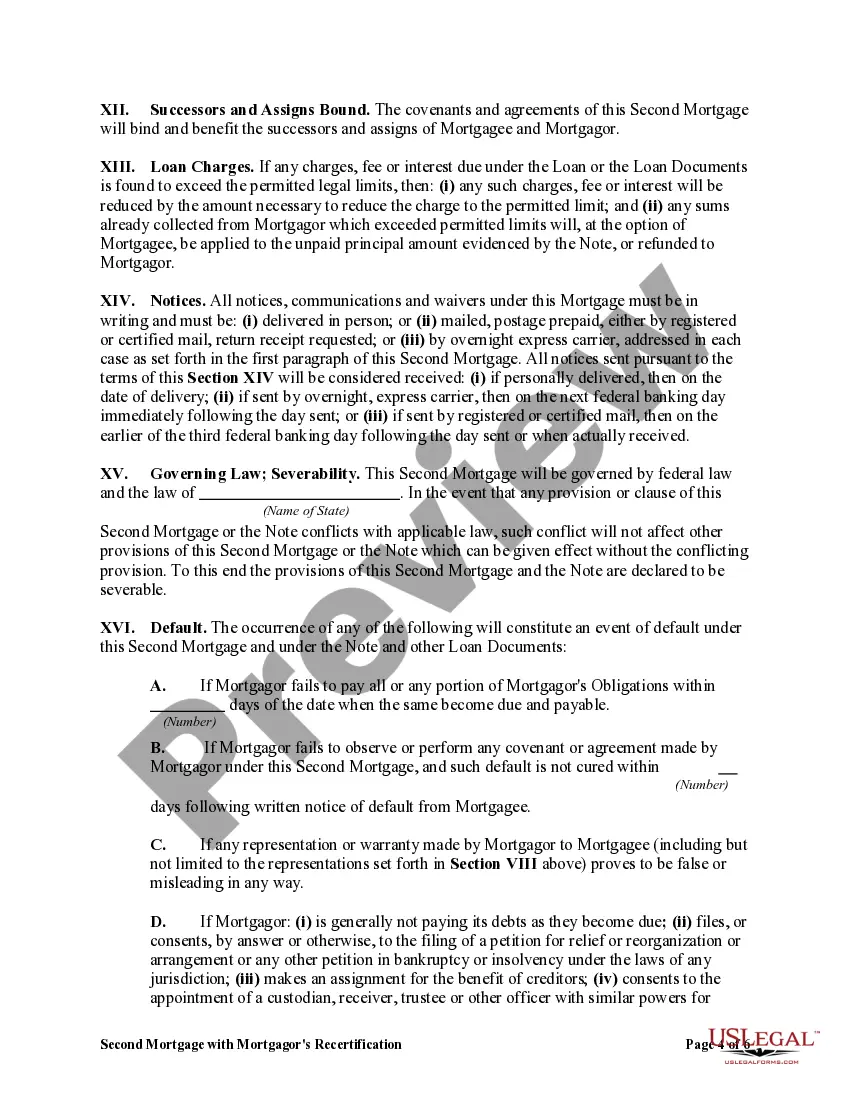

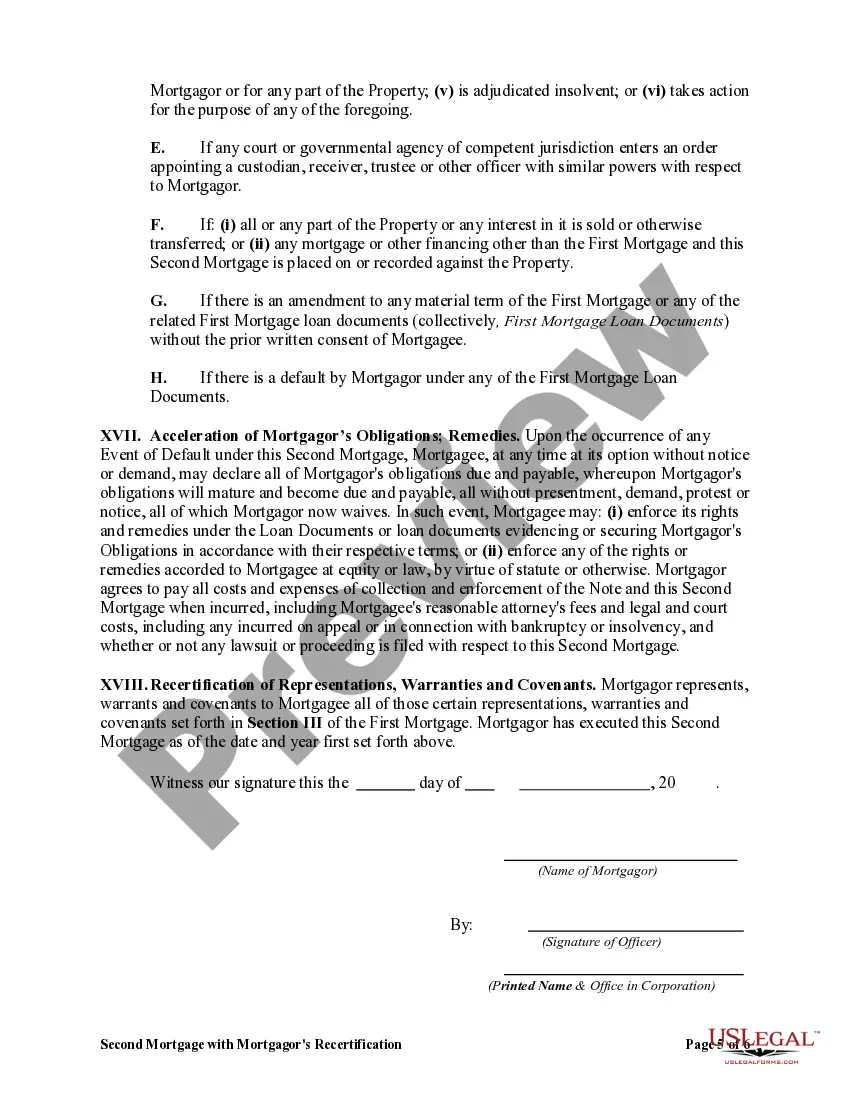

Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage is a financial agreement that involves securing a secondary loan against a property located in the state of Utah. This mortgage type requires the mortgagor (borrower) to reaffirm or recertify the representations, warranties, and covenants made in the original first mortgage. The purpose of recertification is to ensure that the mortgagor is still compliant with the terms and conditions of the first mortgage and to confirm the accuracy of the previously made representations and warranties. It serves as a protective measure for the second mortgage lender, allowing them to assess the updated financial standing of the borrower. Utah has various types of second mortgages wherein the mortgagor's recertification of representations, warranties, and covenants in the first mortgage is required. Some common types include: 1. Home Equity Line of Credit (HELOT): This type of second mortgage allows homeowners to access funds by borrowing against the equity in their Utah property. During the HELOT process, the mortgagor may be required to recertify their representations, warranties, and covenants made in the first mortgage. 2. Fixed-Rate Second Mortgage: In this Utah second mortgage type, the borrower receives a lump sum of money and pays it back in regular installments over a predetermined period. The mortgagor's recertification may be necessary when entering into this agreement. 3. Adjustable-Rate Second Mortgage: Unlike a fixed-rate second mortgage, an adjustable-rate mortgage's interest rate fluctuates over time. Depending on the terms, the mortgagor may have to recertify the representations, warranties, and covenants in the first mortgage when opting for an adjustable-rate second mortgage. The recertification process typically involves the completion of a detailed application and documentation submission, similar to the initial mortgage application. The lender reviews the recertification materials and verifies the borrower's financial information, creditworthiness, and property valuation to assess eligibility for the second mortgage. It is crucial for borrowers to understand the implications of recertification and adhere to the obligations outlined in the first mortgage's representations, warranties, and covenants. Failure to meet these conditions may lead to consequences such as loan default or foreclosure. In summary, Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage is a financial arrangement that enables borrowers to access additional funds by leveraging their property's equity. Through the recertification process, borrowers reaffirm their compliance with the original mortgage agreement, ensuring transparency and accountability for the secondary mortgage lender.

Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Utah Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

Discovering the right legal file design can be a struggle. Of course, there are tons of templates available online, but how would you get the legal type you will need? Use the US Legal Forms site. The service offers a large number of templates, for example the Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, that you can use for enterprise and personal needs. Each of the types are checked by professionals and satisfy federal and state requirements.

When you are previously listed, log in to the account and click the Obtain button to obtain the Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. Utilize your account to search with the legal types you might have bought earlier. Proceed to the My Forms tab of your respective account and obtain an additional copy of your file you will need.

When you are a brand new customer of US Legal Forms, allow me to share basic directions that you can adhere to:

- Initial, be sure you have chosen the appropriate type for the area/region. You are able to examine the shape using the Preview button and read the shape information to guarantee it is the best for you.

- If the type will not satisfy your needs, make use of the Seach industry to get the right type.

- Once you are certain that the shape is suitable, click the Acquire now button to obtain the type.

- Opt for the prices prepare you want and type in the necessary information. Make your account and pay money for the order making use of your PayPal account or Visa or Mastercard.

- Select the file structure and down load the legal file design to the gadget.

- Complete, edit and printing and signal the obtained Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

US Legal Forms may be the greatest catalogue of legal types where you will find numerous file templates. Use the company to down load professionally-manufactured paperwork that adhere to status requirements.