Utah Loan Guaranty Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Guaranty Agreement?

If you want to total, obtain, or print out authorized papers templates, use US Legal Forms, the greatest variety of authorized kinds, which can be found on the Internet. Use the site`s easy and convenient search to discover the files you require. Different templates for company and person functions are sorted by groups and suggests, or search phrases. Use US Legal Forms to discover the Utah Loan Guaranty Agreement in just a couple of mouse clicks.

If you are currently a US Legal Forms client, log in to your profile and click the Down load button to obtain the Utah Loan Guaranty Agreement. You can even gain access to kinds you in the past saved in the My Forms tab of your own profile.

If you work with US Legal Forms initially, follow the instructions below:

- Step 1. Be sure you have selected the shape for your appropriate metropolis/land.

- Step 2. Take advantage of the Preview solution to look through the form`s articles. Don`t forget about to read through the explanation.

- Step 3. If you are not satisfied with the type, make use of the Look for industry towards the top of the monitor to find other types in the authorized type web template.

- Step 4. Once you have found the shape you require, go through the Purchase now button. Pick the rates program you favor and add your accreditations to register to have an profile.

- Step 5. Approach the financial transaction. You can use your charge card or PayPal profile to perform the financial transaction.

- Step 6. Select the file format in the authorized type and obtain it in your gadget.

- Step 7. Full, edit and print out or indicator the Utah Loan Guaranty Agreement.

Each authorized papers web template you acquire is the one you have eternally. You possess acces to each and every type you saved with your acccount. Go through the My Forms section and select a type to print out or obtain once again.

Be competitive and obtain, and print out the Utah Loan Guaranty Agreement with US Legal Forms. There are thousands of professional and condition-particular kinds you can utilize for the company or person needs.

Form popularity

FAQ

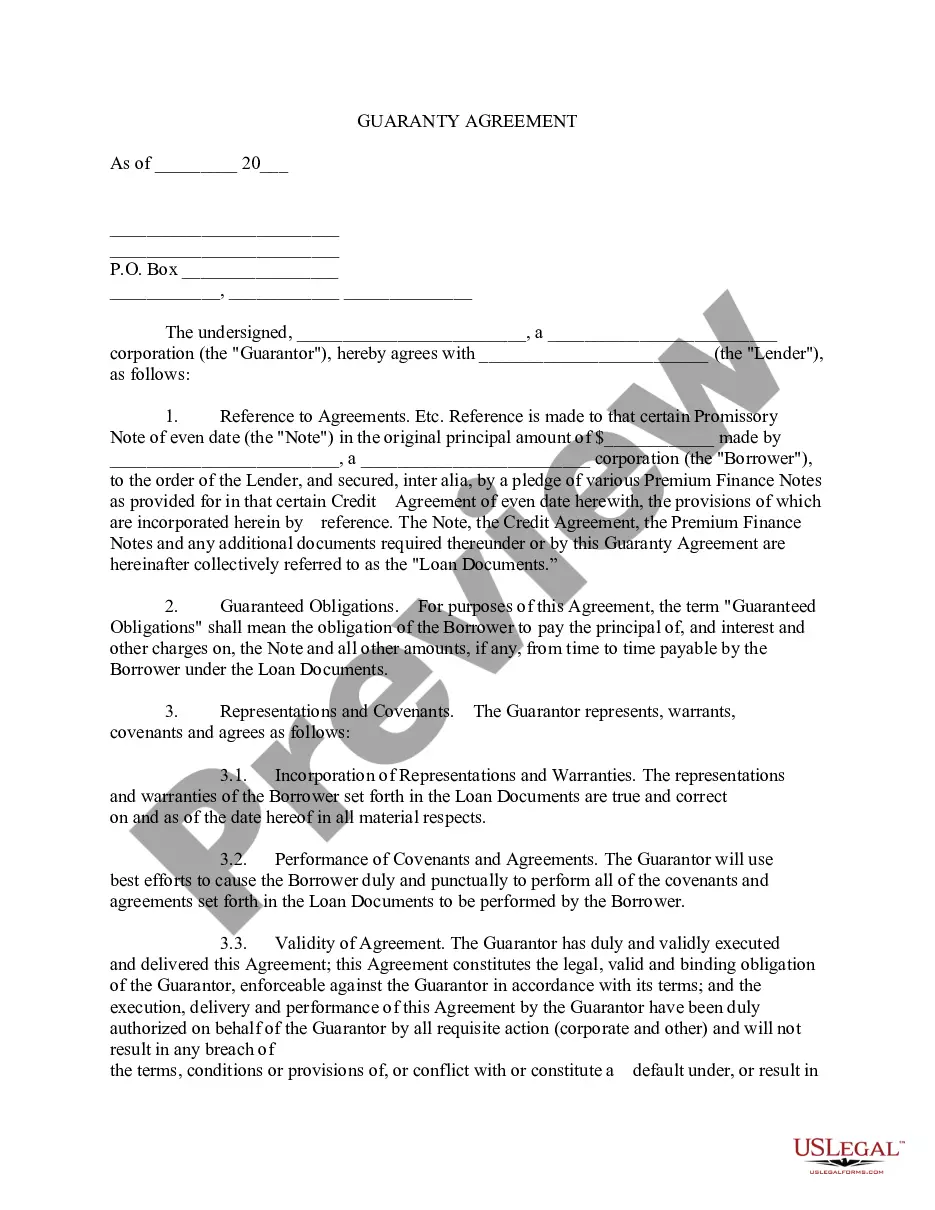

The guarantor unconditionally guarantees the payment obligations of the obligor (the borrower or debtor) for the benefit of the beneficiary (the lender or creditor). This Standard Clause has integrated notes with important explanations and drafting and negotiating tips.

Payment guarantee - What is a payment guarantee? A payment guarantee provides the beneficiary with financial security should the applicant fail to make payment for the goods or services supplied.

The United States shall guarantee to every State in this Union a Republican Form of Government, and shall protect each of them against Invasion; and on Application of the Legislature, or of the Executive (when the Legislature cannot be convened) against domestic Violence.

Guarantee of payment means a loan guarantee under which the authority agrees to pay ing to the terms of the guarantee agreement if the instrument is not paid when due.

A guaranty agreement, in the realm of commercial insurance, refers to a legally binding contract where one party, known as the guarantor, promises to be responsible for the obligations or debts of another party, known as the debtor, if they fail to fulfill their financial commitments.

However, while a co-signer is responsible for every payment that a borrower misses, a guarantor is generally not responsible for repayment unless the borrower fails to repay the loan or lease. Simply becoming a guarantor will generally not impact your credit reports and credit scores.

A guaranty agreement is a contract between two parties where one party agrees to pay a debt or perform a duty in the event that the original party fails to do so. The party who makes the guaranty is called the guarantor. An agreement of this nature is often used in real estate, insurance, or financial transactions.

A Payment Terms clause in a Terms and Conditions agreement is where you set out some key points regarding how you handle and accept payments.