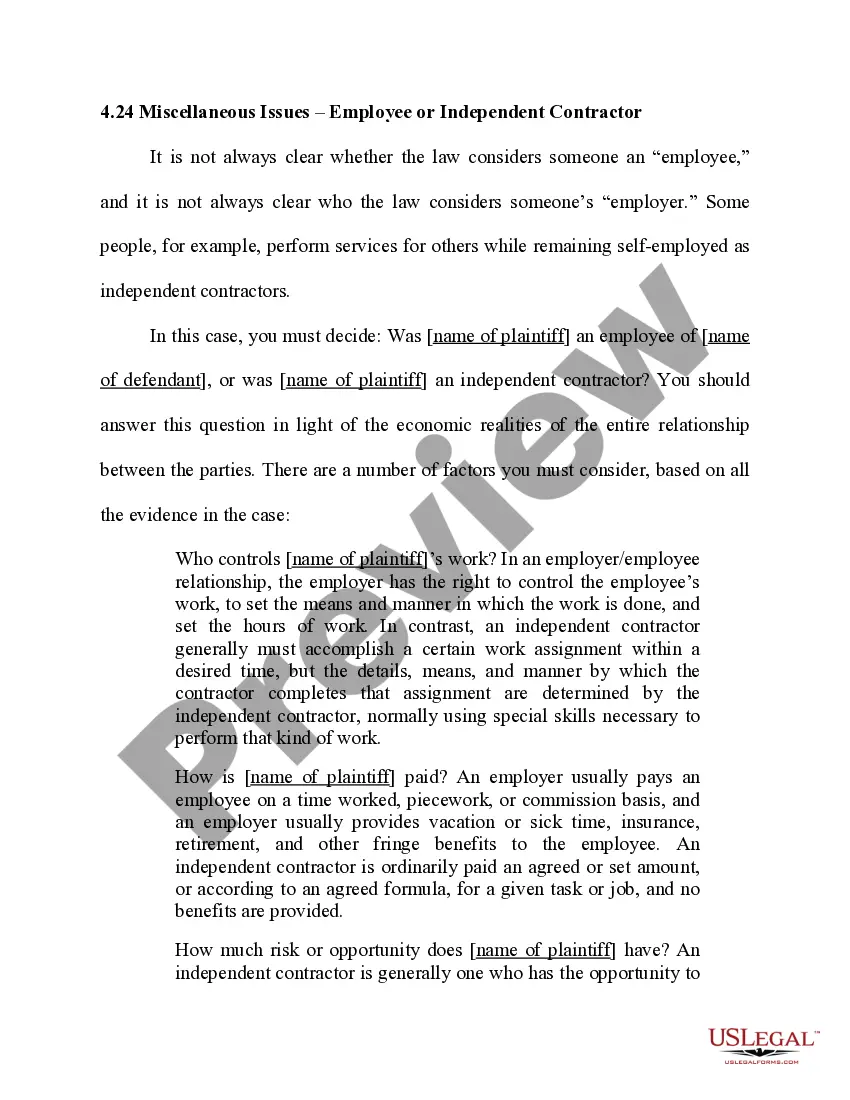

Utah Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor

Description

How to fill out Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor?

US Legal Forms - one of many largest libraries of legal varieties in the USA - delivers a wide array of legal file web templates you can obtain or print. While using internet site, you can find thousands of varieties for company and individual purposes, sorted by groups, states, or search phrases.You will discover the newest versions of varieties such as the Utah Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor within minutes.

If you have a subscription, log in and obtain Utah Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor through the US Legal Forms catalogue. The Acquire option will show up on each kind you view. You have accessibility to all in the past delivered electronically varieties from the My Forms tab of your bank account.

If you wish to use US Legal Forms initially, allow me to share basic guidelines to help you started:

- Be sure you have chosen the right kind to your area/county. Click on the Preview option to check the form`s articles. Read the kind outline to actually have selected the right kind.

- If the kind doesn`t suit your needs, utilize the Research industry towards the top of the screen to get the one who does.

- In case you are content with the shape, verify your choice by clicking the Buy now option. Then, select the pricing program you favor and offer your qualifications to sign up on an bank account.

- Process the transaction. Make use of Visa or Mastercard or PayPal bank account to perform the transaction.

- Select the formatting and obtain the shape on your own system.

- Make adjustments. Complete, edit and print and indicator the delivered electronically Utah Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor.

Each web template you put into your account lacks an expiry date and it is yours permanently. So, if you want to obtain or print one more copy, just visit the My Forms section and then click around the kind you will need.

Obtain access to the Utah Jury Instruction - 1.9.4.1 Employee Self-Employed Independent Contractor with US Legal Forms, one of the most substantial catalogue of legal file web templates. Use thousands of expert and state-particular web templates that satisfy your organization or individual needs and needs.

Form popularity

FAQ

The Utah Workers' Compensation Act defines an independent contractor as "any person engaged in the performance of any work for another who, while so engaged, is (A) independent of the employer in all that pertains to the execution of the work; (B) not subject to the routine rule or control of the employer; (C) engaged ...

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done.

Becoming an independent contractor is one of the many ways to be classified as self-employed. By definition, an independent contractor provides work or services on a contractual basis, whereas, self-employment is simply the act of earning money without operating within an employee-employer relationship.

The law further states that independent contractor status is evidenced if the worker: (1) has a substantial investment in the business other than personal services, (2) purports to be in business for himself or herself, (3) receives compensation by project rather than by time, (4) has control over the time and place ...

How to set up as an independent contractor in Canada Register your business in Canada. Avoid misclassification as an employee. Create compliant contracts that protect you. Invoice and collect payments from around the world.

If the worker is a self-employed individual, they must operate a business and be engaged in a business relationship with the payer. For more information, go to Businesses taxes.