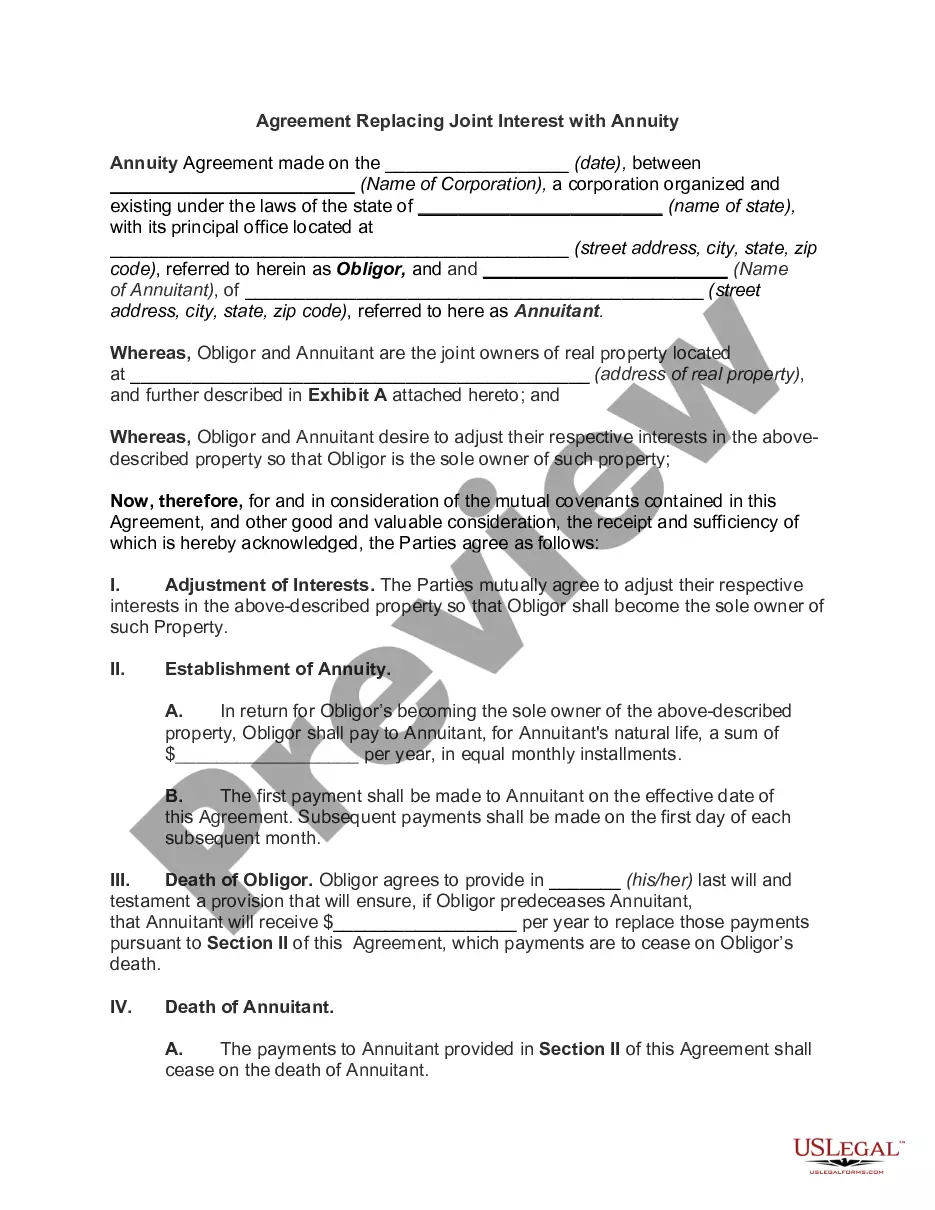

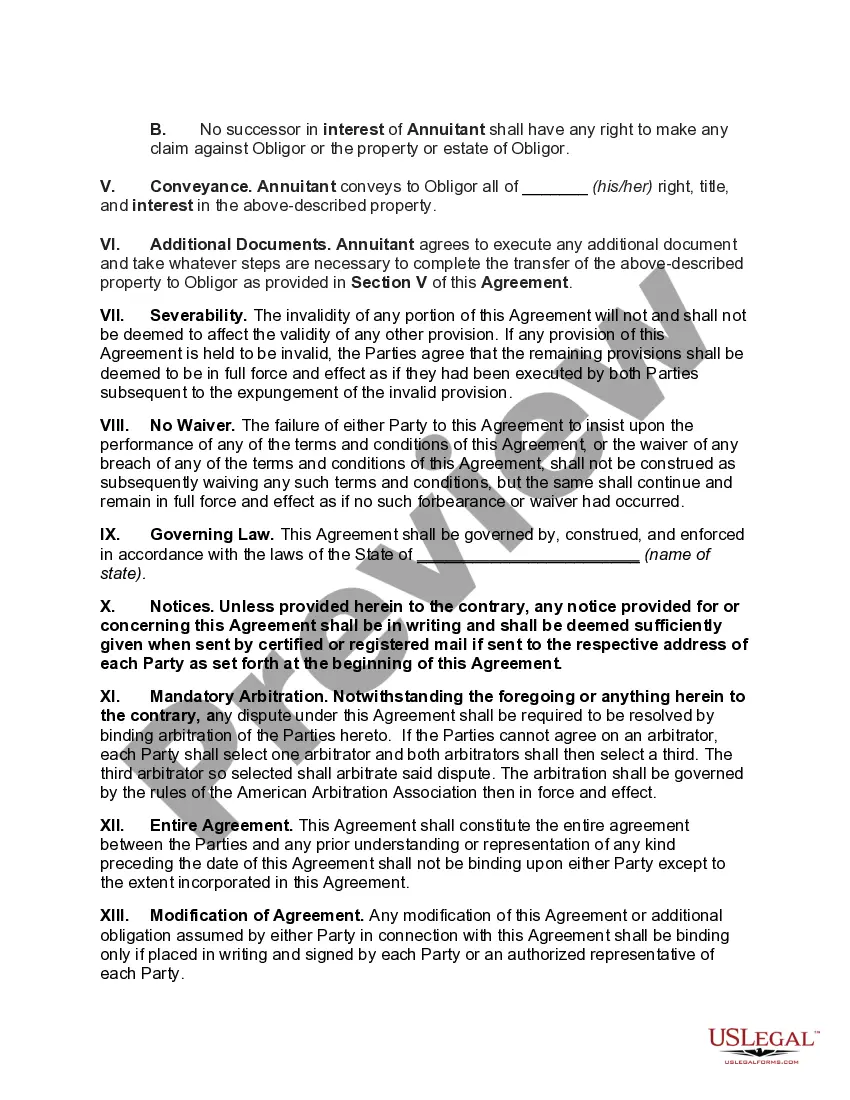

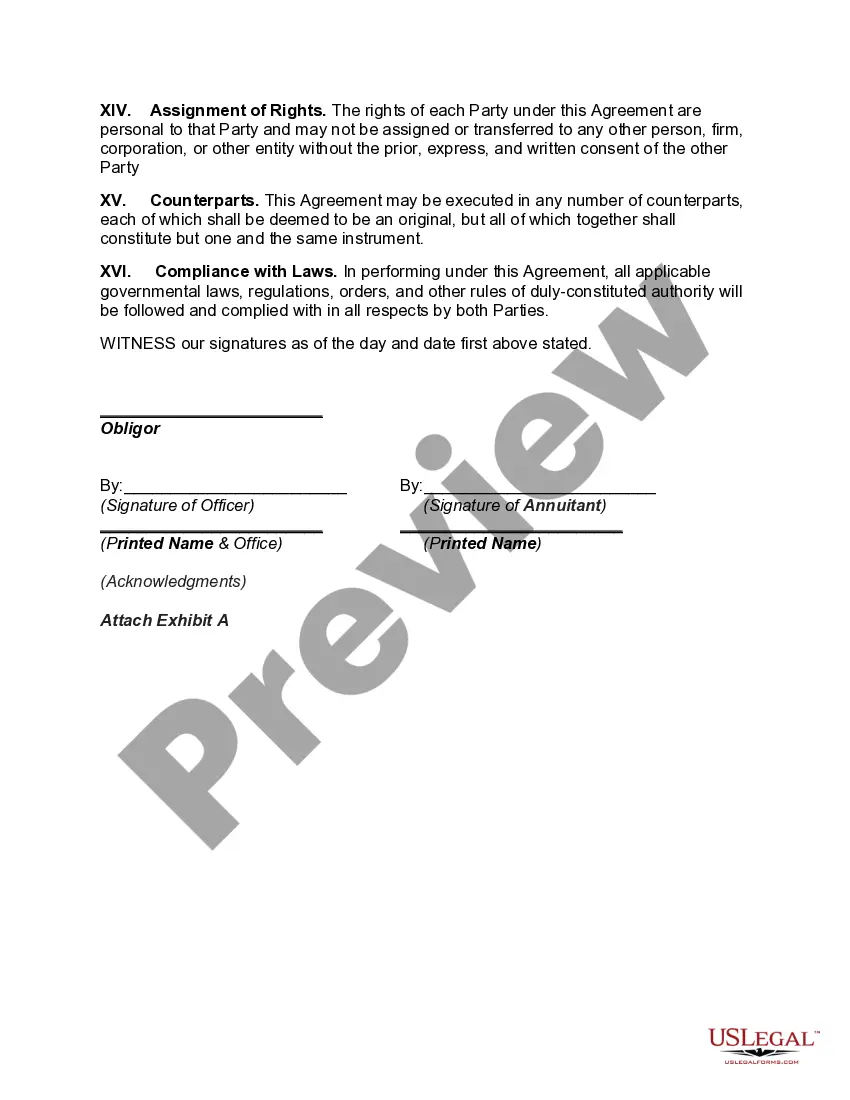

Utah Agreement Replacing Joint Interest with Annuity, also referred to as Utah Annuity Agreement, is a legal document entered into between parties involved in a joint interest arrangement. This agreement outlines the terms and conditions under which joint interest is replaced by an annuity. Here is a detailed description of Utah Agreement Replacing Joint Interest with Annuity, along with some different types: 1. Definition and Purpose: The Utah Agreement Replacing Joint Interest with Annuity is a legally binding contract that enables parties to convert their joint interest into annuities. The purpose of this agreement is to provide a structured payment plan that ensures a steady income stream for the annuity holder over a specified period. 2. Parties Involved: The agreement involves two primary parties — the annuitant and the issuer. The annuitant is the individual who currently holds a joint interest and wishes to convert it into an annuity. The issuer, typically an insurance company or financial institution, is responsible for funding the annuity and making periodic payments to the annuitant. 3. Terms and Conditions: The Utah Agreement Replacing Joint Interest with Annuity involves several crucial terms and conditions, including the following: a. Conversion Process: The agreement outlines the process through which joint interest is converted into an annuity. It includes necessary paperwork, disclosure requirements, and any applicable fees or charges. b. Annuity Options: Various annuity options are available in this agreement, including fixed annuities, variable annuities, and indexed annuities. Each option has its features, risks, and benefits. The agreement should specify the chosen annuity type and any additional customization. c. Payment Structure: The agreement determines the payment structure and frequency of annuity payments. Common options include monthly, quarterly, semi-annually, or yearly payments. The agreement may also allow for lump-sum payments under certain circumstances. d. Duration and Termination: The agreement defines the duration of the annuity, which can range from a fixed number of years to the lifetime of the annuitant. It may contain provisions for termination if certain conditions are met, such as death or any breach of contract. e. Tax and Legal Implications: Utah Agreement Replacing Joint Interest with Annuity should address the tax and legal consequences of converting joint interest into an annuity. Parties must comprehend the tax treatment of annuity income and any penalties for early withdrawal. 4. Types of Utah Agreement Replacing Joint Interest with Annuity: While the overall concept remains the same, there can be variations in the specific types of Utah Agreement Replacing Joint Interest with Annuity, depending on the annuity options and objectives. Here are a few common types: a. Fixed Annuity Agreement: In this type, the annuitant receives a fixed payment amount at regular intervals, ensuring a predictable income flow regardless of market conditions. b. Variable Annuity Agreement: Variable annuities provide the annuitant with the opportunity to invest in various investment options. The income received fluctuates based on the performance of the underlying investments. c. Indexed Annuity Agreement: An indexed annuity guarantees a minimum rate of return combined with the potential to earn higher returns linked to a specific index, such as the stock market or bond market. In conclusion, Utah Agreement Replacing Joint Interest with Annuity is a legal contract that facilitates the conversion of joint interest into annuity payments. It offers parties the option to secure a reliable income stream while choosing from various annuity types and payment structures. Understanding the terms, tax implications, and different types of agreements is crucial when considering this financial arrangement.

Utah Agreement Replacing Joint Interest with Annuity

Description

How to fill out Utah Agreement Replacing Joint Interest With Annuity?

US Legal Forms - one of the largest libraries of legal forms in America - offers a wide array of legal document themes you may download or print out. Making use of the internet site, you may get thousands of forms for business and individual reasons, categorized by types, claims, or keywords and phrases.You will find the newest versions of forms like the Utah Agreement Replacing Joint Interest with Annuity within minutes.

If you have a subscription, log in and download Utah Agreement Replacing Joint Interest with Annuity from your US Legal Forms local library. The Down load key will show up on each and every kind you look at. You gain access to all formerly downloaded forms from the My Forms tab of your profile.

If you would like use US Legal Forms initially, listed below are easy guidelines to obtain started off:

- Be sure to have picked out the correct kind for your personal area/state. Go through the Preview key to review the form`s articles. See the kind description to ensure that you have selected the correct kind.

- In the event the kind does not suit your demands, make use of the Search discipline at the top of the monitor to discover the one that does.

- Should you be pleased with the form, affirm your selection by clicking the Purchase now key. Then, opt for the costs program you like and provide your credentials to register for an profile.

- Method the transaction. Utilize your credit card or PayPal profile to complete the transaction.

- Find the structure and download the form on your own system.

- Make modifications. Fill out, edit and print out and sign the downloaded Utah Agreement Replacing Joint Interest with Annuity.

Each and every template you added to your account does not have an expiry day and is also your own for a long time. So, if you wish to download or print out an additional backup, just check out the My Forms segment and click around the kind you will need.

Gain access to the Utah Agreement Replacing Joint Interest with Annuity with US Legal Forms, the most comprehensive local library of legal document themes. Use thousands of professional and state-particular themes that fulfill your small business or individual requirements and demands.