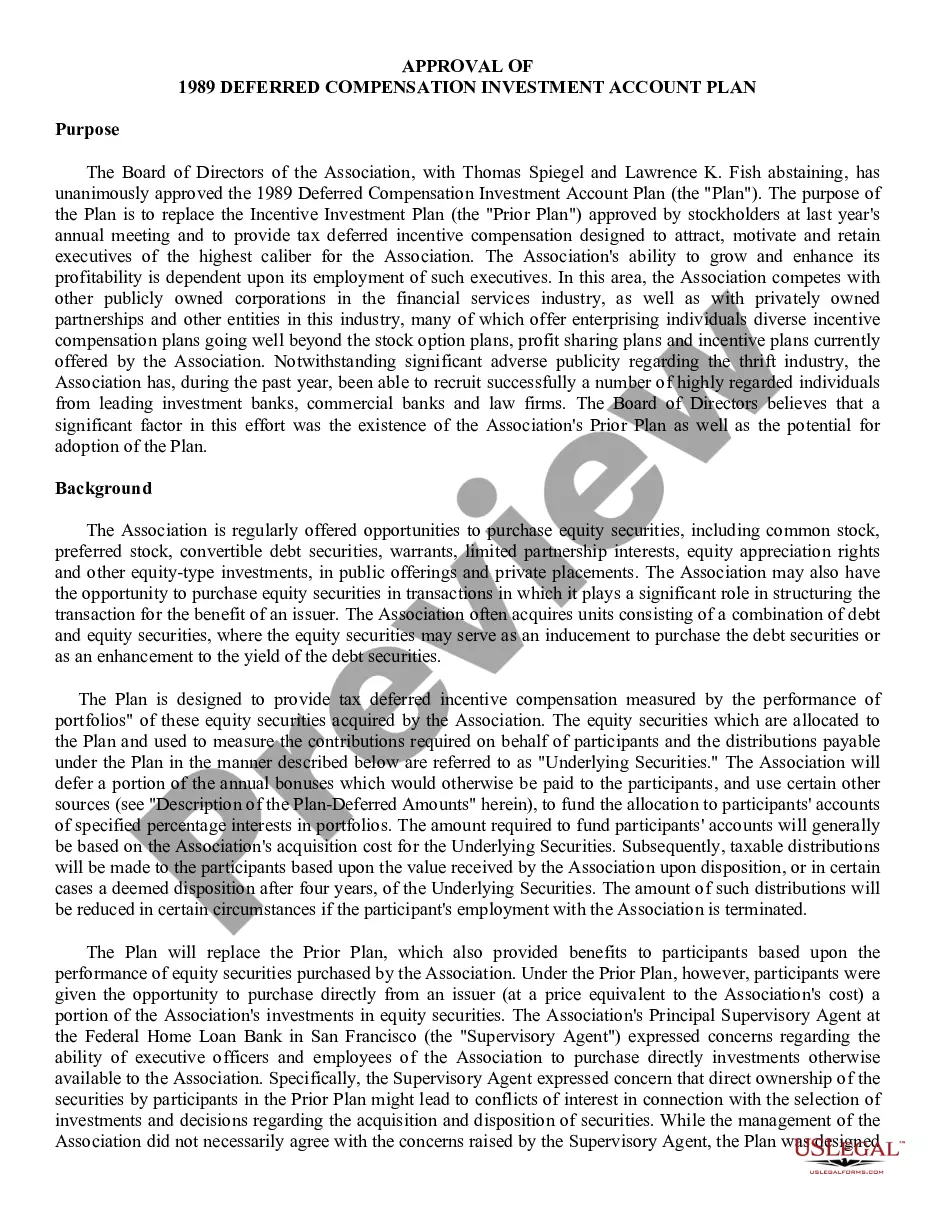

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Utah Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

US Legal Forms - one of the biggest libraries of lawful forms in the United States - gives a wide array of lawful document web templates you may download or print. Using the website, you can find thousands of forms for company and specific reasons, categorized by categories, states, or keywords.You will discover the most recent versions of forms much like the Utah Deferred Compensation Investment Account Plan within minutes.

If you already possess a membership, log in and download Utah Deferred Compensation Investment Account Plan in the US Legal Forms collection. The Download key will appear on each and every develop you view. You get access to all formerly downloaded forms in the My Forms tab of your own profile.

If you would like use US Legal Forms initially, listed here are simple instructions to obtain began:

- Ensure you have chosen the proper develop for your town/county. Go through the Review key to review the form`s articles. Look at the develop description to ensure that you have chosen the appropriate develop.

- When the develop does not fit your requirements, utilize the Research industry near the top of the display to get the the one that does.

- In case you are content with the form, verify your decision by clicking on the Acquire now key. Then, choose the costs prepare you prefer and give your references to sign up for the profile.

- Approach the transaction. Use your bank card or PayPal profile to accomplish the transaction.

- Select the file format and download the form on the gadget.

- Make modifications. Fill out, edit and print and indicator the downloaded Utah Deferred Compensation Investment Account Plan.

Each and every template you included in your account does not have an expiry day which is the one you have eternally. So, if you would like download or print one more copy, just visit the My Forms area and click on on the develop you will need.

Get access to the Utah Deferred Compensation Investment Account Plan with US Legal Forms, the most extensive collection of lawful document web templates. Use thousands of skilled and status-particular web templates that meet your organization or specific demands and requirements.

Form popularity

FAQ

The plans carry some inherent risk for the employees in that the deferred payments are unsecured and not guaranteed. So if the organization faces bankruptcy and creditor claims, the employees may not receive their promised funds. (In contrast, qualified plans such as 401(k)s are protected from bankruptcy creditors).

457(b) vs 403(b) On the whole, 457(b) plans have a lot in common with 403(b) plans. They are both employer-sponsored retirement savings accounts, they have the same standard contribution limits, and they use similar types of investment accounts to grow funds for retirement.

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, 401(k) retirement plans, and employee stock options.

Remember, when received, deferred compensation is taxable as income. If you're still employed, it's added to your income, which could increase your tax rate. I advise using a deferred comp plan on a limited basis, if at all, for shorter-term goals.

Deferred compensation has the potential to increase capital gains over time when offered as an investment account or a stock option. Rather than simply receiving the amount that was initially deferred, a 401(k) and other deferred compensation plans can increase in value before retirement.

As compared to a 401K plan, an NQDC offers less flexibility when it comes to withdrawals. There's no RMD (required minimum distribution), but you're bound to distribution elections made prior to contributions being made. You can sometimes change these elections, but it results in a five-year delay.

Deferring income to retirement might help avoid high state income taxes (ex: California, New York, etc) if you're planning to move to a low-tax state. The biggest risk of deferred compensation plans is they're not guaranteed; if your company goes bankrupt, you might receive none of the income you deferred.

Why Is Deferred Compensation Better Than a 401(k)? Deferred compensation is often considered better than a 401(k) for high-paid executives looking to reduce their tax burden. As well, contribution limits on deferred compensation plans can be much higher than 401(k) limits.