Utah Split-Dollar Life Insurance

Description

How to fill out Split-Dollar Life Insurance?

Choosing the best authorized document web template could be a struggle. Obviously, there are plenty of web templates available on the net, but how will you discover the authorized kind you want? Utilize the US Legal Forms site. The services offers 1000s of web templates, for example the Utah Split-Dollar Life Insurance, that you can use for company and personal requires. Each of the forms are examined by experts and meet state and federal requirements.

In case you are previously signed up, log in in your accounts and click the Acquire option to have the Utah Split-Dollar Life Insurance. Make use of accounts to search with the authorized forms you possess bought earlier. Check out the My Forms tab of the accounts and acquire yet another backup from the document you want.

In case you are a brand new end user of US Legal Forms, allow me to share easy instructions for you to comply with:

- Initially, make certain you have chosen the correct kind for your city/state. You are able to look over the shape using the Preview option and study the shape explanation to make certain this is the best for you.

- If the kind fails to meet your preferences, utilize the Seach discipline to obtain the proper kind.

- When you are sure that the shape would work, click the Buy now option to have the kind.

- Select the rates program you would like and enter the needed info. Design your accounts and pay money for your order using your PayPal accounts or credit card.

- Pick the document format and download the authorized document web template in your system.

- Comprehensive, revise and print and indicator the obtained Utah Split-Dollar Life Insurance.

US Legal Forms is the most significant library of authorized forms for which you can discover a variety of document web templates. Utilize the service to download professionally-manufactured papers that comply with status requirements.

Form popularity

FAQ

The best way is to contact the policy's issuer (the life insurance company). Their records are key: even if you see your name listed on an old policy document, the deceased may have changed their beneficiaries (or the allocation of benefits among those beneficiaries) after that document was printed.

Employers are responsible for making split-dollar life insurance premiums, regardless of the plan's type. However, it is important to note that under loan arrangements, employees must repay the premiums via collateral assignments made to their employer.

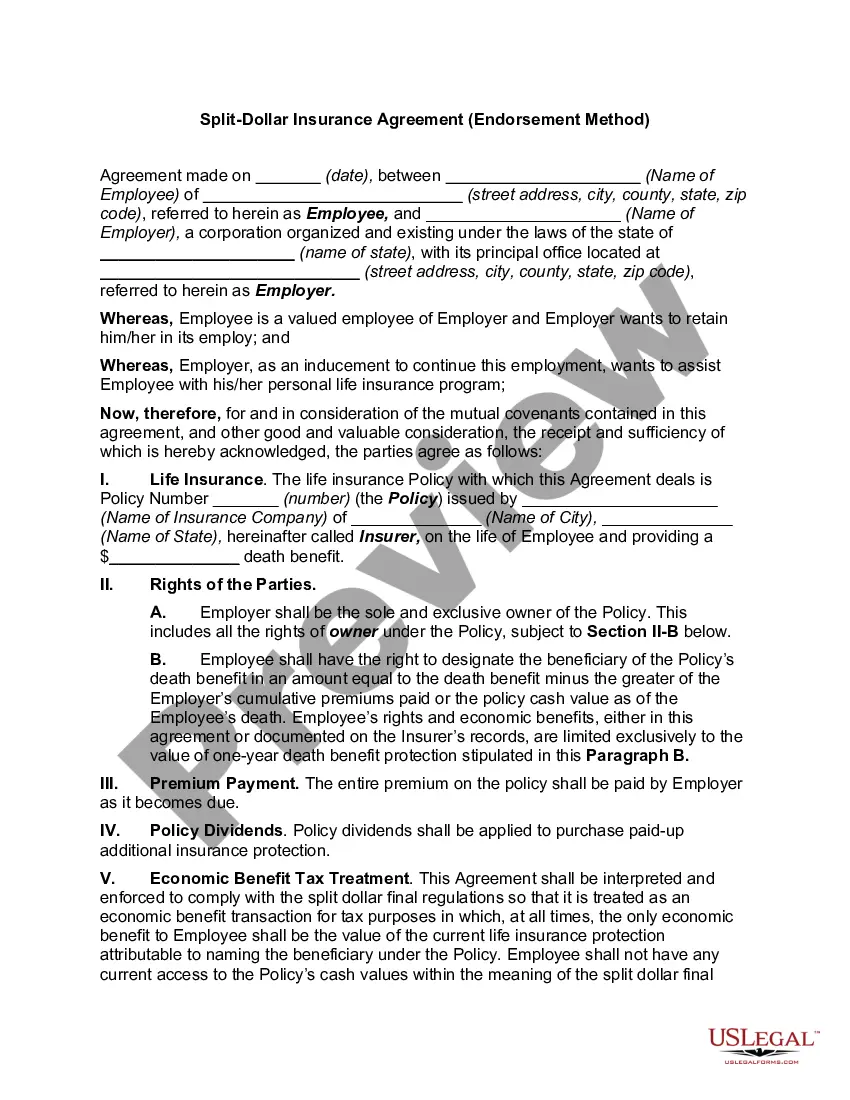

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

With a classic split-dollar plan, the employer pays some of the premium (the part that is equal to cash value), while the employee pays the rest. If the employees dies, or the plan is terminated, the surrender cash value is paid to the company, and the death benefits are paid out to beneficiaries.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.

Split Dollar Loan Regime Agreement & Contract Generally, at the employee's death, the employer receives a portion of the death benefit (usually equal to the total premiums plus interest from the loan) and the employee's beneficiary receives the balance.

dollar life insurance plan is an agreement between an employer and an employee in which they hold joint ownership of a permanent cashvalue life insurance policy, including its benefits and premiums.