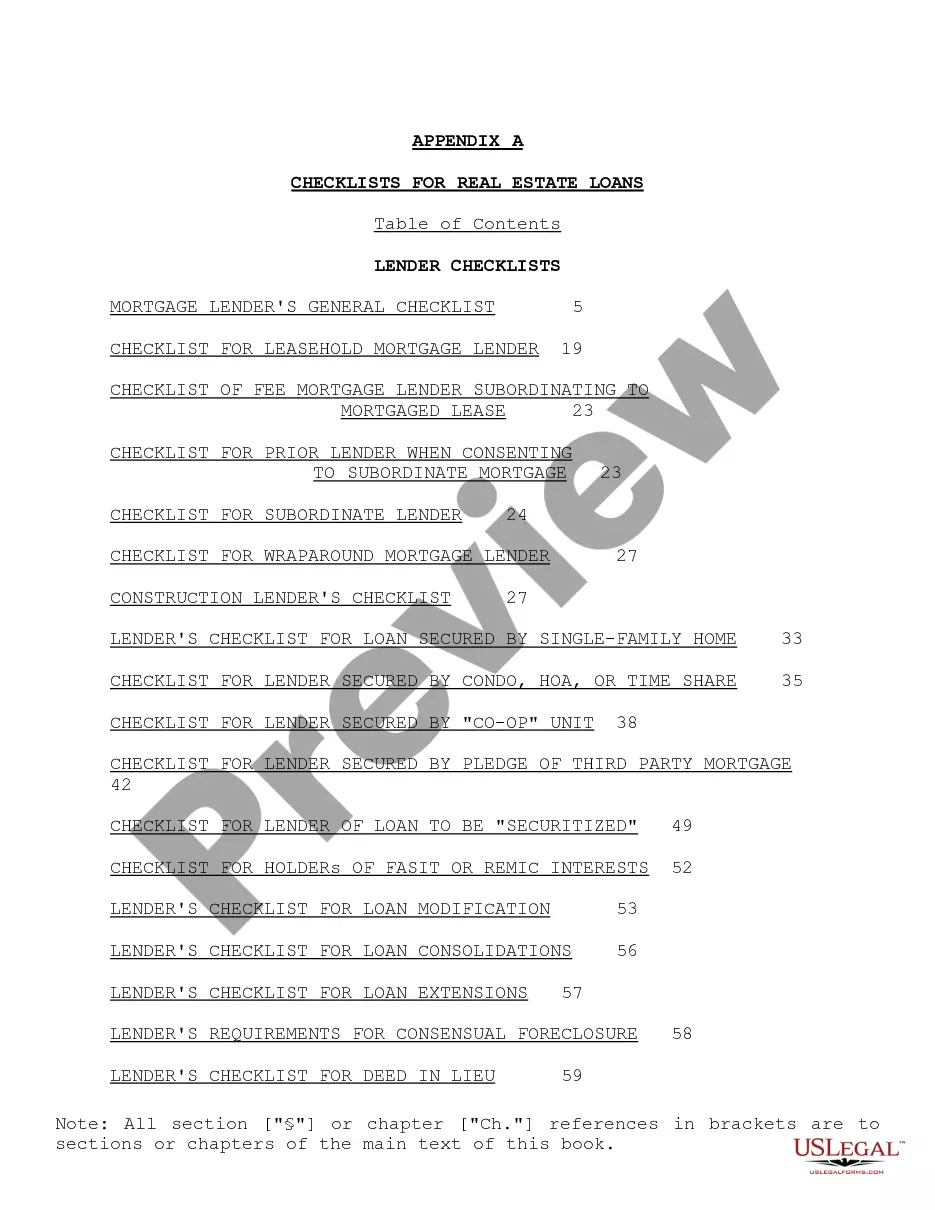

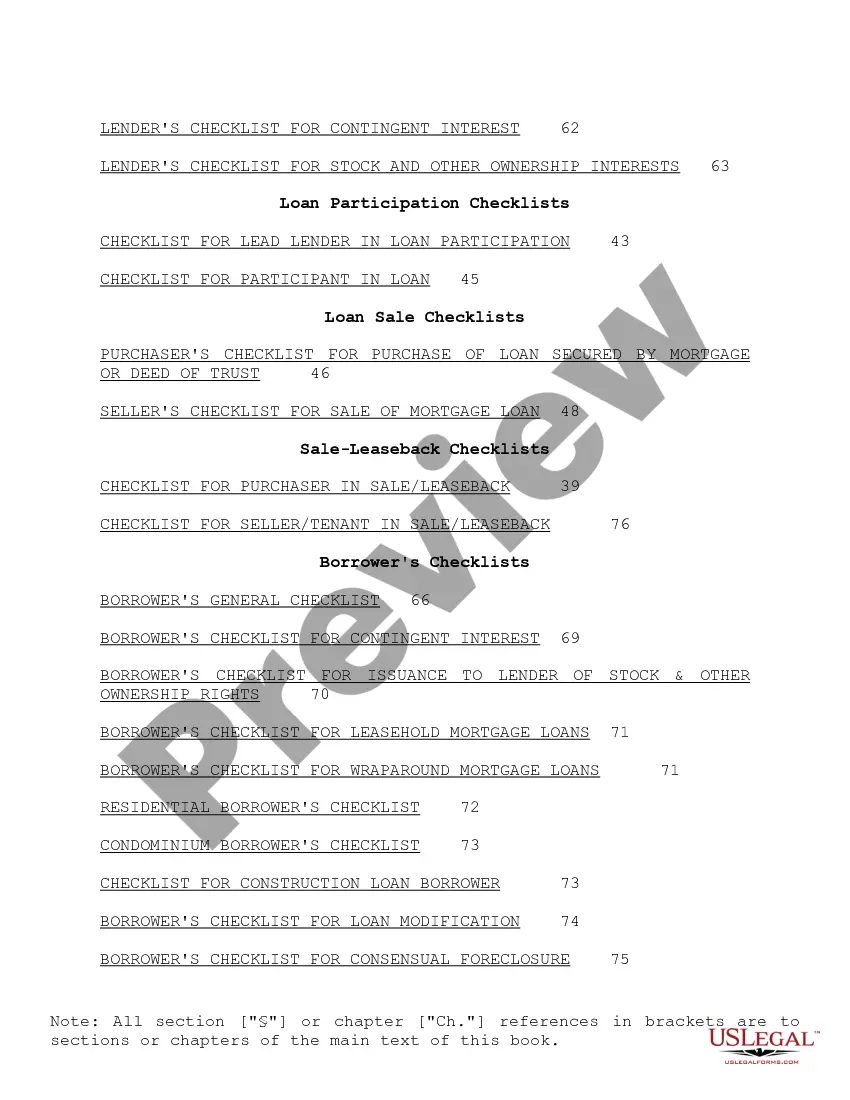

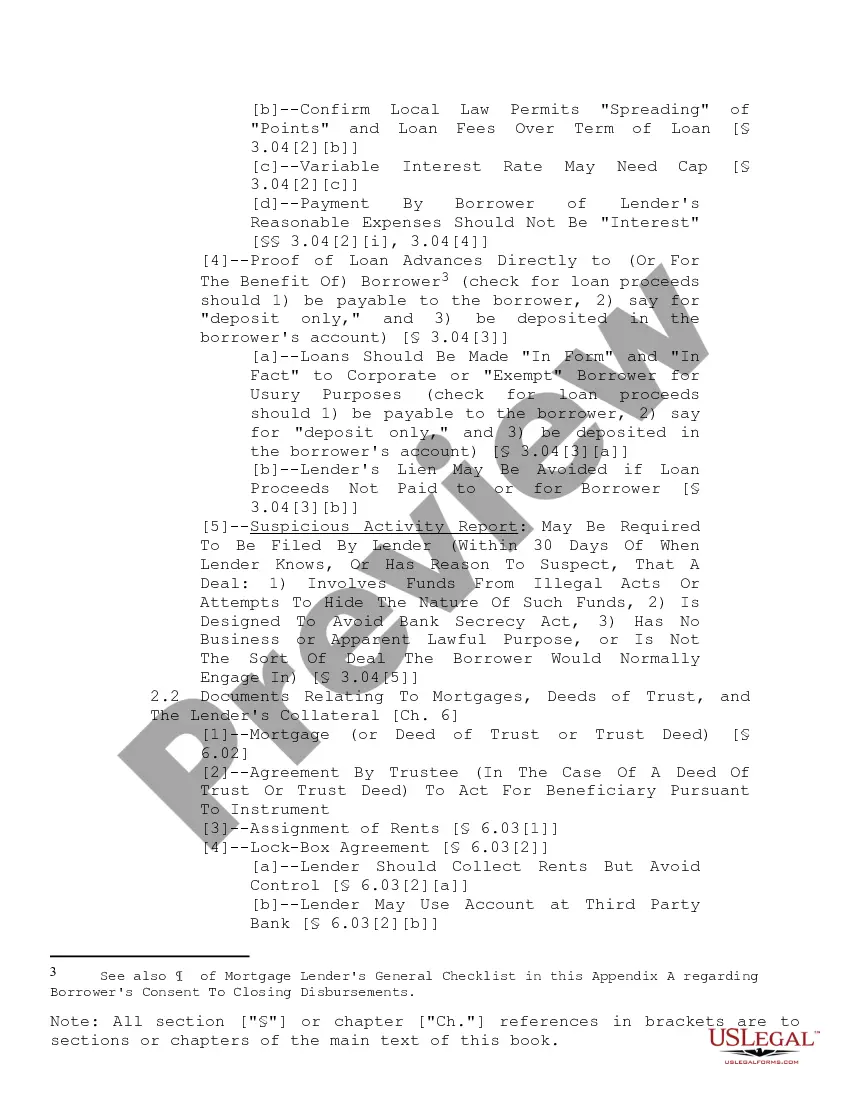

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Utah Checklist for Real Estate Loans: A Comprehensive Guide for Borrowers Introduction: If you are considering purchasing real estate in Utah, it is crucial to understand the checklist for acquiring a real estate loan. This detailed description will outline the various components involved in the Utah Checklist for Real Estate Loans, including essential documents, financial requirements, and specific considerations for different loan types. Whether you are a first-time homebuyer or an experienced investor, this guide will help you navigate through the loan application process smoothly. 1. Required Documents: To initiate the loan application process, certain documents are typically needed. These include: — Personal identification documents (driver's license, passport, etc.). — Social Security number— - Proof of income (pay stubs, tax returns, etc.). — Bank statements— - Employment verification. — Credit history reports— - Property-related documents (purchase agreement, property appraisal, etc.). — Insurance coverage details. 2. Financial Requirements: Lenders in Utah usually have specific financial benchmarks for loan approval. These may include: — Credit score: A strong FICO score is vital for obtaining favorable loan terms. — Debt-to-income ratio: Lenders consider your monthly debt payments in relation to your gross income. — Down payment: The amount you need to contribute up-front, usually a percentage of the property's purchase price. — Asset verification: Details of your existing assets, such as savings, investments, and real estate holdings, may be required. 3. Loan Types: There are various loan options available in Utah, each with its specific requirements and benefits: — Conventional Loans: Backed by private lenders, these loans typically require a higher credit score and a larger down payment. — FHA Loans: Insured by the Federal Housing Administration, these loans come with lower down payment and credit score requirements. — VA Loans: Exclusive to veterans, active-duty military personnel, and their eligible spouses, these loans offer favorable terms and low or no down payment options. — USDA Loans: Aimed at homebuyers in rural areas, these loans provide 100% financing and have income limitations. — Jumbo Loans: Designed for financing high-value properties exceeding conventional loan limits, these loans have stricter criteria. Conclusion: The Utah Checklist for Real Estate Loans encompasses various crucial factors to consider when seeking financing for property purchase. By understanding the required documents, financial requirements, and different loan options available in Utah, borrowers can successfully navigate the real estate loan application process. Consulting with a knowledgeable mortgage professional can further aid in ensuring a smooth loan approval process tailored to specific needs and circumstances.Utah Checklist for Real Estate Loans: A Comprehensive Guide for Borrowers Introduction: If you are considering purchasing real estate in Utah, it is crucial to understand the checklist for acquiring a real estate loan. This detailed description will outline the various components involved in the Utah Checklist for Real Estate Loans, including essential documents, financial requirements, and specific considerations for different loan types. Whether you are a first-time homebuyer or an experienced investor, this guide will help you navigate through the loan application process smoothly. 1. Required Documents: To initiate the loan application process, certain documents are typically needed. These include: — Personal identification documents (driver's license, passport, etc.). — Social Security number— - Proof of income (pay stubs, tax returns, etc.). — Bank statements— - Employment verification. — Credit history reports— - Property-related documents (purchase agreement, property appraisal, etc.). — Insurance coverage details. 2. Financial Requirements: Lenders in Utah usually have specific financial benchmarks for loan approval. These may include: — Credit score: A strong FICO score is vital for obtaining favorable loan terms. — Debt-to-income ratio: Lenders consider your monthly debt payments in relation to your gross income. — Down payment: The amount you need to contribute up-front, usually a percentage of the property's purchase price. — Asset verification: Details of your existing assets, such as savings, investments, and real estate holdings, may be required. 3. Loan Types: There are various loan options available in Utah, each with its specific requirements and benefits: — Conventional Loans: Backed by private lenders, these loans typically require a higher credit score and a larger down payment. — FHA Loans: Insured by the Federal Housing Administration, these loans come with lower down payment and credit score requirements. — VA Loans: Exclusive to veterans, active-duty military personnel, and their eligible spouses, these loans offer favorable terms and low or no down payment options. — USDA Loans: Aimed at homebuyers in rural areas, these loans provide 100% financing and have income limitations. — Jumbo Loans: Designed for financing high-value properties exceeding conventional loan limits, these loans have stricter criteria. Conclusion: The Utah Checklist for Real Estate Loans encompasses various crucial factors to consider when seeking financing for property purchase. By understanding the required documents, financial requirements, and different loan options available in Utah, borrowers can successfully navigate the real estate loan application process. Consulting with a knowledgeable mortgage professional can further aid in ensuring a smooth loan approval process tailored to specific needs and circumstances.