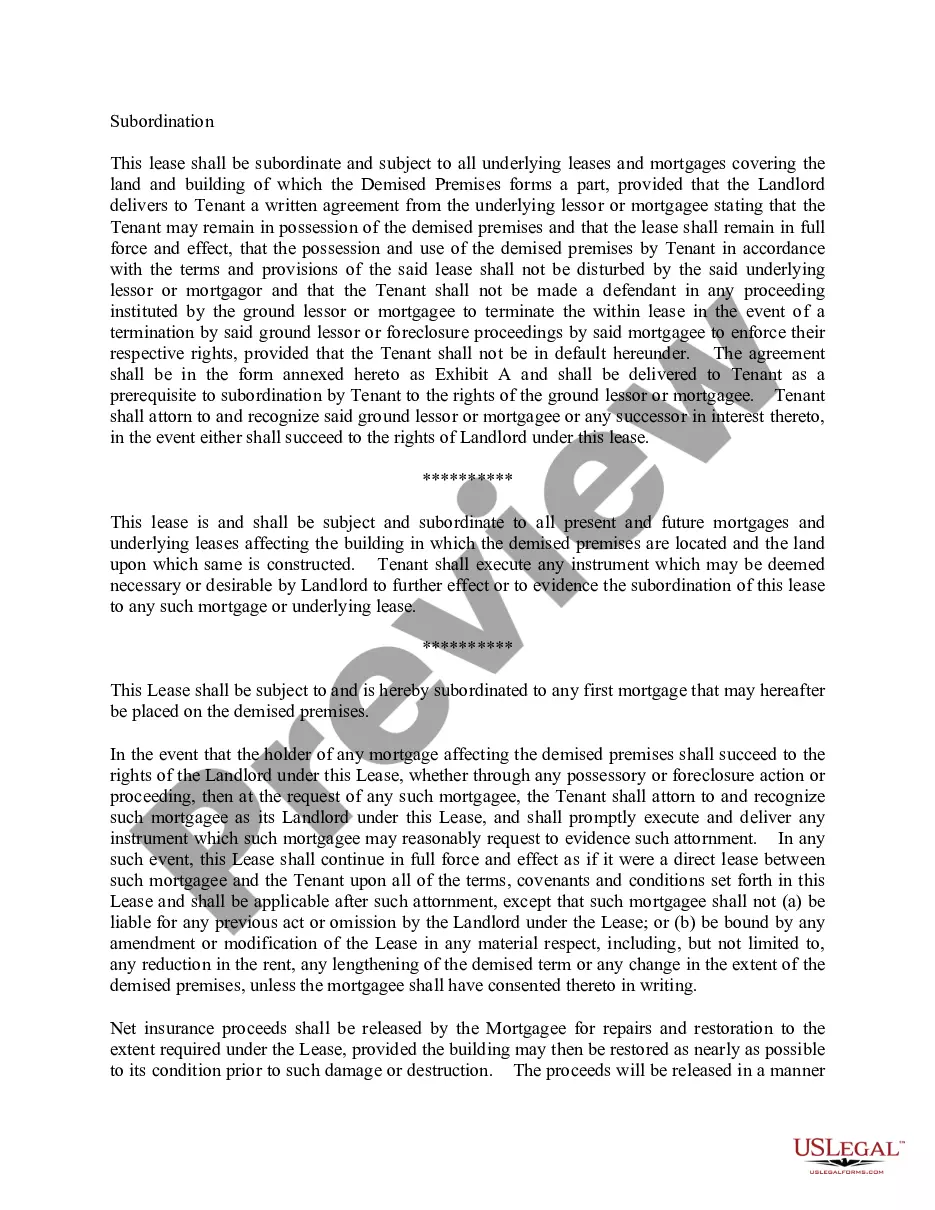

This office lease form is a more detailed, more complicated subordination provision stating that subordination is conditioned on the landlord providing the tenant with a satisfactory non-disturbance agreement.

Utah Detailed Subordination Provision

Category:

State:

Multi-State

Control #:

US-OL20022B

Format:

Word;

PDF

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Detailed Subordination Provision?

Are you currently within a situation that you require paperwork for either business or person uses nearly every time? There are tons of legal file themes available online, but discovering types you can rely is not straightforward. US Legal Forms delivers a huge number of develop themes, much like the Utah Detailed Subordination Provision, that are composed to satisfy state and federal specifications.

If you are presently informed about US Legal Forms web site and get your account, simply log in. After that, you are able to down load the Utah Detailed Subordination Provision template.

Unless you have an accounts and wish to begin using US Legal Forms, follow these steps:

- Get the develop you want and make sure it is for the correct town/county.

- Take advantage of the Preview button to check the shape.

- Read the information to ensure that you have selected the right develop.

- In case the develop is not what you are trying to find, make use of the Look for field to get the develop that fits your needs and specifications.

- Once you find the correct develop, click on Acquire now.

- Choose the prices strategy you would like, submit the specified information to make your money, and pay money for an order with your PayPal or credit card.

- Select a practical paper file format and down load your backup.

Discover all of the file themes you possess bought in the My Forms menu. You can aquire a additional backup of Utah Detailed Subordination Provision anytime, if required. Just click on the required develop to down load or print out the file template.

Use US Legal Forms, probably the most substantial selection of legal kinds, to conserve time as well as steer clear of mistakes. The service delivers professionally created legal file themes which you can use for an array of uses. Make your account on US Legal Forms and begin producing your daily life easier.

Form popularity

FAQ

A subordination clause serves to protect the lender if a homeowner defaults. If this happens, the lender then has the legal standing to repossess the home and cover their loan's outstanding balance first. If other subordinate mortgages are involved, the secondary liens will take a backseat in this process.

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.

The party that primarily benefits from a subordination clause in real estate is the lender. However, if you decide to pursue a second mortgage, then the subordination clause prioritizes the first lender's repayment and contract rights. The most common application of subordination clauses is when refinancing a property.

Subordination agreements are used to legally establish the order in which debts are to be repaid in the event of a foreclosure or bankruptcy. In return for the agreement, the lender with the subordinated debt will be compensated in some manner for the additional risk.

The Subordination Clause A subordination is a contractual agreement by the tenant that its leasehold interest in the collateral property, or portion thereof (the subject property of the lease), is subordinate either to the mortgage or to the lien of the mortgage.

A subordinate clause is a clause that cannot stand alone as a complete sentence; it merely complements a sentence's main clause, thereby adding to the whole unit of meaning. Because a subordinate clause is dependent upon a main clause to be meaningful, it is also referred to as a dependent clause.