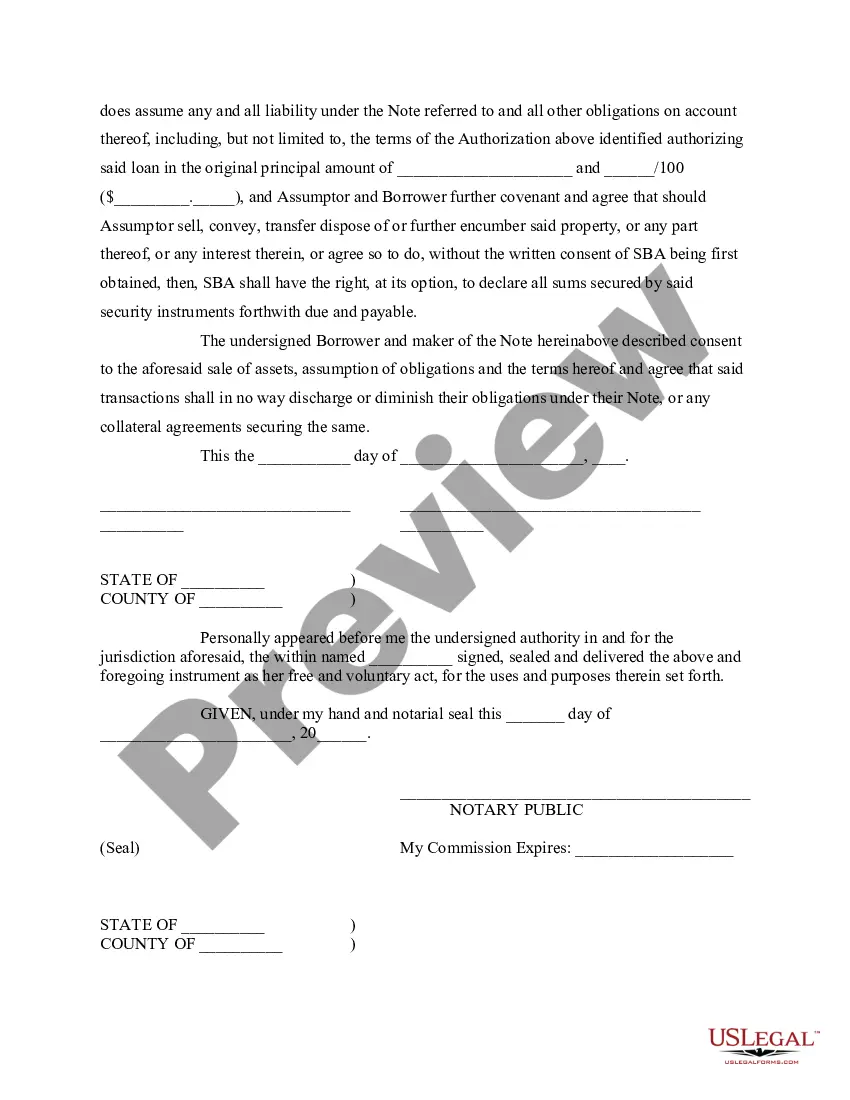

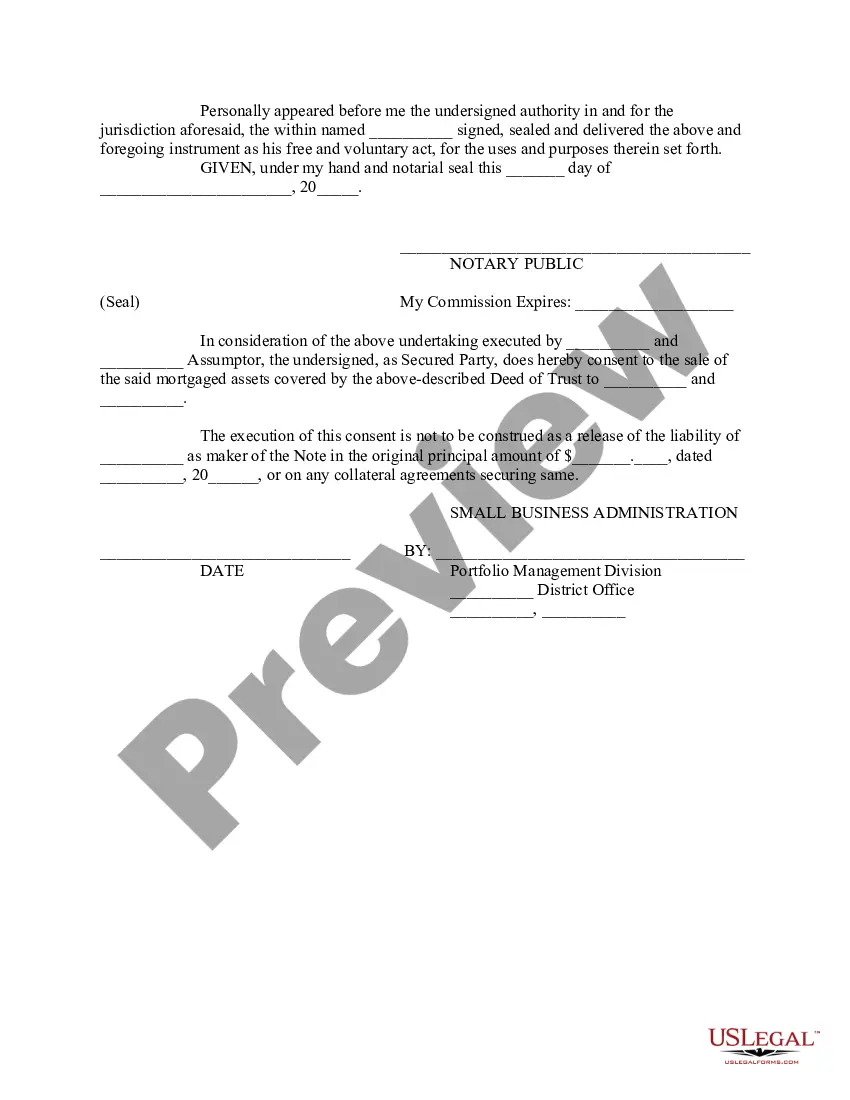

This form is an assumption agreement for a Small Business Administration (SBA) loan. Party assuming the loan agrees to continue payments thereon. SBA agrees to the assumption of the loan and release of original debtor. Adapt to fit your circumstances.

The Virginia Assumption Agreement of SBA Loan is a legal document that allows for the transfer of ownership and responsibility of a Small Business Administration (SBA) loan to a new borrower, typically when a business is being sold or transferred. This agreement is specific to loans obtained in the state of Virginia and follows the regulations and guidelines set forth by the SBA. The assumption agreement outlines the terms and conditions under which the new borrower assumes the existing loan obligations. It is crucial for all parties involved, including the original borrower, new borrower, and lenders, to carefully review and understand the agreement before signing. The agreement typically includes details such as the loan amount, the terms and conditions of the original loan, the interest rate, repayment schedule, and any fees or penalties associated with the loan. It also clarifies that the new borrower will assume all responsibilities for the loan, including making timely payments and complying with all SBA rules and regulations. There may be different types of Virginia Assumption Agreement of SBA Loans, depending on the specific circumstances of the loan transfer. Some of these types may include: 1. Full Assumption Agreement: This type of assumption agreement transfers the entire loan and its obligations from the original borrower to the new borrower. The new borrower becomes solely responsible for the loan repayment. 2. Partial Assumption Agreement: In certain cases, the original borrower may still retain some liability for the loan, while a portion of the loan is transferred to the new borrower. This type of agreement specifies the specific portion of the loan being assumed by the new borrower. 3. Assumption with Release: This type of assumption agreement may involve the release of collateral or personal guarantees of the original borrower upon assumption by the new borrower. This ensures that the original borrower is no longer responsible for the loan or its associated risks. Regardless of the type of assumption agreement, it is crucial for all parties involved to consult with legal professionals experienced in SBA lending and Virginia state laws to ensure compliance and protect their interests.

The Virginia Assumption Agreement of SBA Loan is a legal document that allows for the transfer of ownership and responsibility of a Small Business Administration (SBA) loan to a new borrower, typically when a business is being sold or transferred. This agreement is specific to loans obtained in the state of Virginia and follows the regulations and guidelines set forth by the SBA. The assumption agreement outlines the terms and conditions under which the new borrower assumes the existing loan obligations. It is crucial for all parties involved, including the original borrower, new borrower, and lenders, to carefully review and understand the agreement before signing. The agreement typically includes details such as the loan amount, the terms and conditions of the original loan, the interest rate, repayment schedule, and any fees or penalties associated with the loan. It also clarifies that the new borrower will assume all responsibilities for the loan, including making timely payments and complying with all SBA rules and regulations. There may be different types of Virginia Assumption Agreement of SBA Loans, depending on the specific circumstances of the loan transfer. Some of these types may include: 1. Full Assumption Agreement: This type of assumption agreement transfers the entire loan and its obligations from the original borrower to the new borrower. The new borrower becomes solely responsible for the loan repayment. 2. Partial Assumption Agreement: In certain cases, the original borrower may still retain some liability for the loan, while a portion of the loan is transferred to the new borrower. This type of agreement specifies the specific portion of the loan being assumed by the new borrower. 3. Assumption with Release: This type of assumption agreement may involve the release of collateral or personal guarantees of the original borrower upon assumption by the new borrower. This ensures that the original borrower is no longer responsible for the loan or its associated risks. Regardless of the type of assumption agreement, it is crucial for all parties involved to consult with legal professionals experienced in SBA lending and Virginia state laws to ensure compliance and protect their interests.