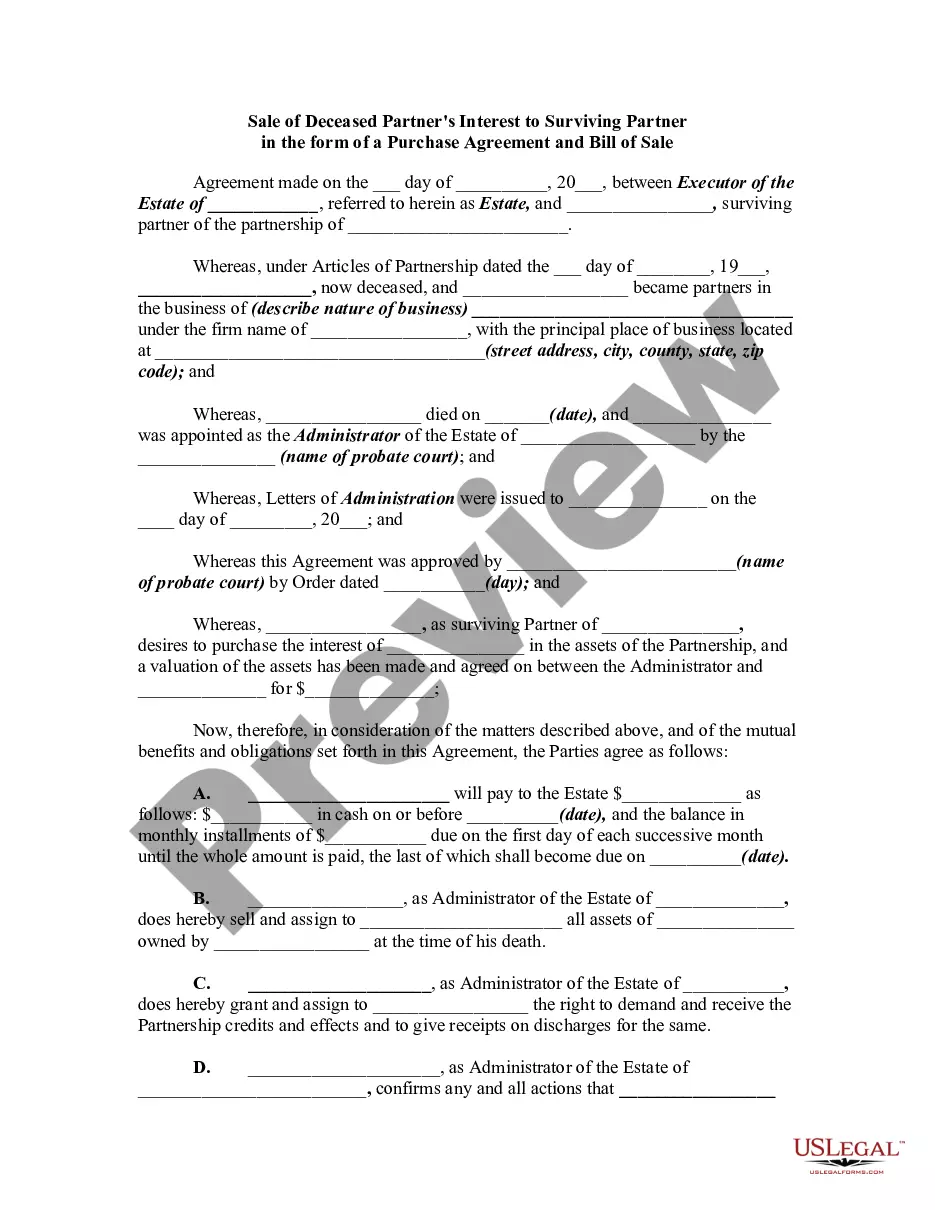

The Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale is a legal document that outlines the transfer of a deceased partner's ownership stake in a partnership to the surviving partner. This agreement ensures a smooth transition of ownership and provides clarity in terms of the purchase price, payment terms, and other relevant details. Keywords: Virginia, Sale of Deceased Partner's Interest, Surviving Partner, Purchase Agreement, Bill of Sale, partnership, transfer of ownership, smooth transition, purchase price, payment terms. Types of Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale: 1. Basic Purchase Agreement: This type of agreement is the standard version used for transferring a deceased partner's interest to the surviving partner. It includes essential information like the purchase price, payment terms, and responsibilities of both parties. 2. Lump Sum Payment Agreement: In cases where the surviving partner prefers to make a single payment for the deceased partner's interest, a lump sum payment agreement can be utilized. This agreement specifies the total amount to be paid, the payment schedule, and any applicable interest or penalty charges. 3. Installment Payment Agreement: If the surviving partner wishes to pay off the purchase price in installments, this type of agreement can be employed. It outlines the amount of each installment, the frequency of payments, and any interest or penalties for late or missed payments. 4. Promissory Note Agreement: In situations where the surviving partner needs to borrow funds to finance the purchase, a promissory note agreement can be used. This type of agreement includes the terms of the loan, such as the principal amount, interest rate, repayment schedule, and any collateral required. 5. Partnership Dissolution Agreement: If the sale of the deceased partner's interest results in the dissolution of the partnership, a partnership dissolution agreement may be necessary. This document addresses the distribution of assets, liabilities, and any remaining obligations between the partners. It's important to consult with a qualified attorney or legal professional to ensure that the specific requirements of the Virginia Sale of Deceased Partner's Interest to Surviving Partner are met and that the agreement is tailored to the unique circumstances of the partnership.

Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out Virginia Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

Discovering the right lawful document design can be quite a have a problem. Obviously, there are tons of layouts available on the Internet, but how can you discover the lawful develop you require? Use the US Legal Forms website. The assistance delivers 1000s of layouts, for example the Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale, which can be used for enterprise and personal needs. All of the kinds are checked out by experts and meet up with state and federal requirements.

If you are previously authorized, log in to your account and click on the Obtain button to get the Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale. Make use of account to check from the lawful kinds you possess purchased in the past. Proceed to the My Forms tab of your respective account and acquire one more duplicate of the document you require.

If you are a new end user of US Legal Forms, listed here are basic guidelines so that you can comply with:

- Very first, ensure you have selected the correct develop to your area/region. You are able to examine the shape making use of the Review button and browse the shape information to ensure it is the best for you.

- When the develop is not going to meet up with your requirements, utilize the Seach discipline to find the correct develop.

- Once you are certain that the shape is suitable, click the Get now button to get the develop.

- Select the pricing prepare you desire and enter the required details. Build your account and pay for the transaction making use of your PayPal account or charge card.

- Choose the submit format and acquire the lawful document design to your product.

- Comprehensive, revise and produce and indication the received Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale.

US Legal Forms is the biggest collection of lawful kinds for which you will find a variety of document layouts. Use the company to acquire appropriately-created documents that comply with state requirements.