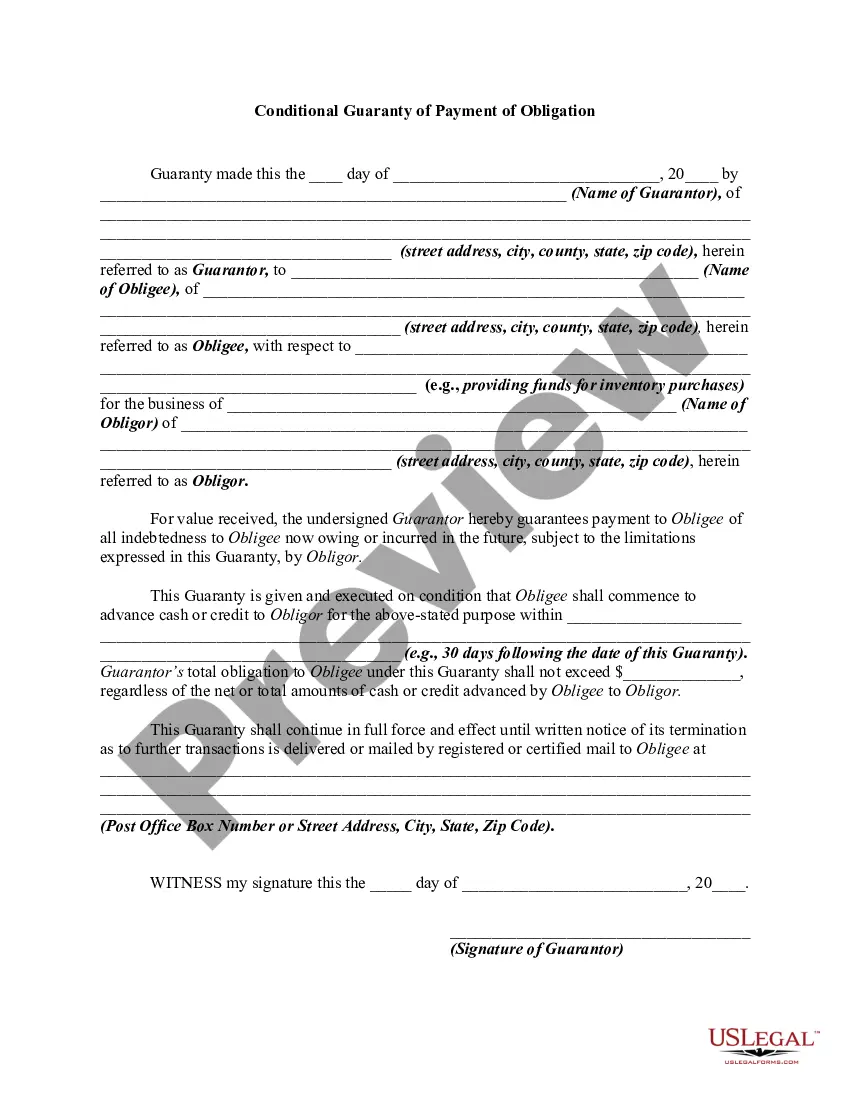

A guaranty is a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law. A conditional guaranty contemplates, as a condition to liability on the part of the guarantor, the happening of some contingent event. A guaranty of the payment of a debt is distinguished from a guaranty of the collection of the debt, the former being absolute and the latter conditional.

A Virginia Conditional Guaranty of Payment of Obligation is a legally binding agreement between a guarantor and a lender, typically used in commercial transactions. This type of guaranty provides an additional layer of security for the lender by ensuring that if the borrower fails to meet their payment obligations, the guarantor will step in and cover the debt. In Virginia, there are different types of conditional guaranties of payment of obligation that can be customized to suit the needs of the parties involved. Some common types include: 1. Unconditional Guaranty: This is the most common type of guaranty where the guarantor agrees to unconditionally fulfill the borrower's payment obligations in the event of default. The guarantor's liability under this type of guaranty is not dependent on any conditions or contingencies. 2. Conditional Guaranty: In a conditional guaranty, the guarantor's liability is triggered by specific conditions or events, such as the borrower's insolvency or failure to make a certain number of payments. This type of guaranty provides some protection to the guarantor as their liability is only activated under specified circumstances. 3. Limited Guaranty: A limited guaranty restricts the guarantor's liability to a certain maximum amount or for a specific period of time. This type of guaranty allows the guarantor to limit their exposure to potential losses and provides a measure of protection for their assets. 4. Continuing Guaranty: A continuing guaranty remains in effect until it is formally terminated by the guarantor, even if the underlying obligation has been satisfied or discharged. This ensures that the lender continues to have recourse to the guarantor's assets for any future defaults by the borrower. 5. Joint and Several guaranties: Under a joint and several guaranties, multiple guarantors are held equally responsible for the borrower's obligations. This means that the lender can pursue anyone or all of the guarantors for the full amount owed, providing greater security to the lender in case one guarantor becomes insolvent. When drafting a Virginia Conditional Guaranty of Payment of Obligation, it is essential to include specific terms and provisions that accurately reflect the intentions and requirements of the parties involved. These may include details about the underlying obligation, the triggering events for guarantor liability, the scope of guarantor's obligations, any limitations or conditions, and provisions for enforcement and dispute resolution. Overall, a Virginia Conditional Guaranty of Payment of Obligation provides lenders with an additional level of assurance and protection in commercial transactions, ensuring that the loan will be repaid even if the borrower defaults.A Virginia Conditional Guaranty of Payment of Obligation is a legally binding agreement between a guarantor and a lender, typically used in commercial transactions. This type of guaranty provides an additional layer of security for the lender by ensuring that if the borrower fails to meet their payment obligations, the guarantor will step in and cover the debt. In Virginia, there are different types of conditional guaranties of payment of obligation that can be customized to suit the needs of the parties involved. Some common types include: 1. Unconditional Guaranty: This is the most common type of guaranty where the guarantor agrees to unconditionally fulfill the borrower's payment obligations in the event of default. The guarantor's liability under this type of guaranty is not dependent on any conditions or contingencies. 2. Conditional Guaranty: In a conditional guaranty, the guarantor's liability is triggered by specific conditions or events, such as the borrower's insolvency or failure to make a certain number of payments. This type of guaranty provides some protection to the guarantor as their liability is only activated under specified circumstances. 3. Limited Guaranty: A limited guaranty restricts the guarantor's liability to a certain maximum amount or for a specific period of time. This type of guaranty allows the guarantor to limit their exposure to potential losses and provides a measure of protection for their assets. 4. Continuing Guaranty: A continuing guaranty remains in effect until it is formally terminated by the guarantor, even if the underlying obligation has been satisfied or discharged. This ensures that the lender continues to have recourse to the guarantor's assets for any future defaults by the borrower. 5. Joint and Several guaranties: Under a joint and several guaranties, multiple guarantors are held equally responsible for the borrower's obligations. This means that the lender can pursue anyone or all of the guarantors for the full amount owed, providing greater security to the lender in case one guarantor becomes insolvent. When drafting a Virginia Conditional Guaranty of Payment of Obligation, it is essential to include specific terms and provisions that accurately reflect the intentions and requirements of the parties involved. These may include details about the underlying obligation, the triggering events for guarantor liability, the scope of guarantor's obligations, any limitations or conditions, and provisions for enforcement and dispute resolution. Overall, a Virginia Conditional Guaranty of Payment of Obligation provides lenders with an additional level of assurance and protection in commercial transactions, ensuring that the loan will be repaid even if the borrower defaults.