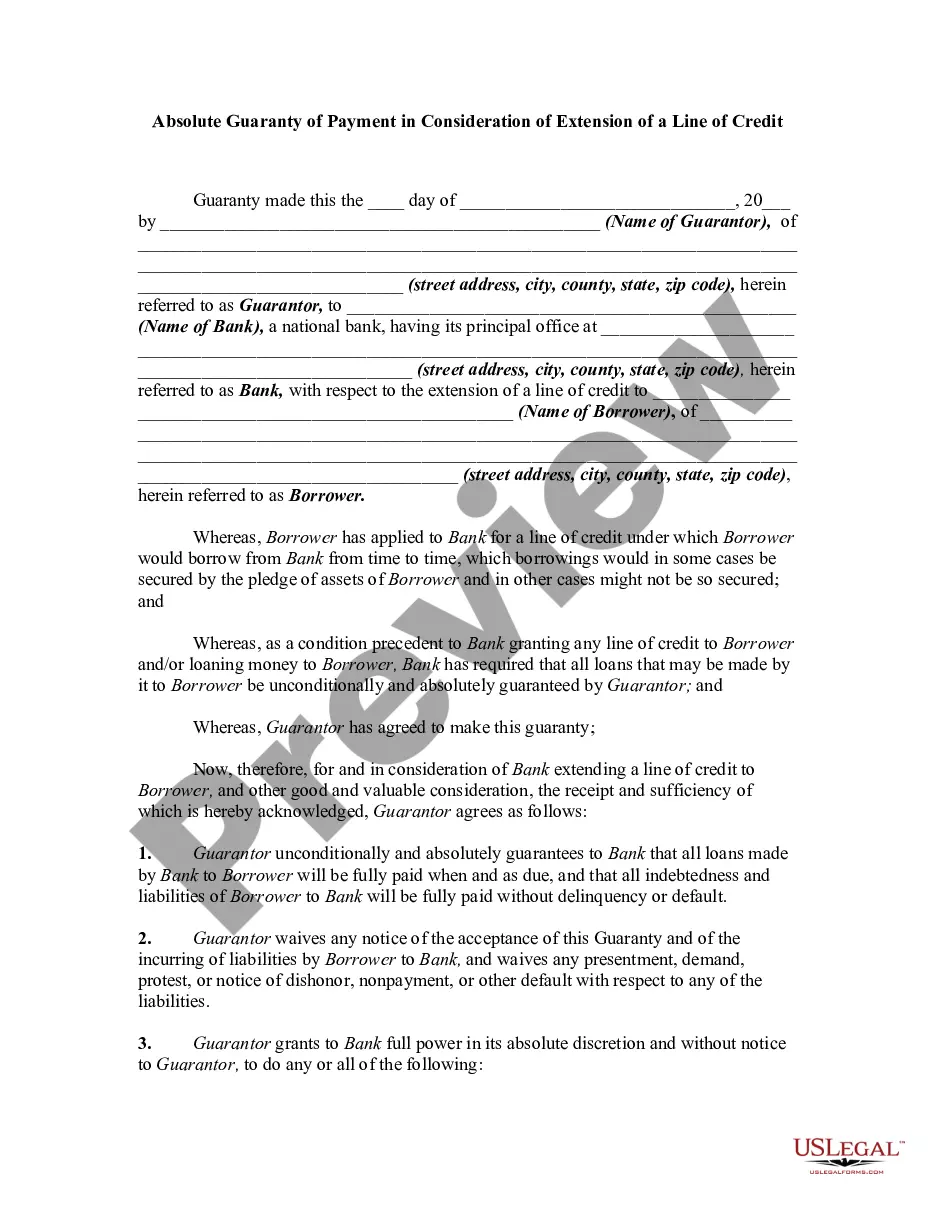

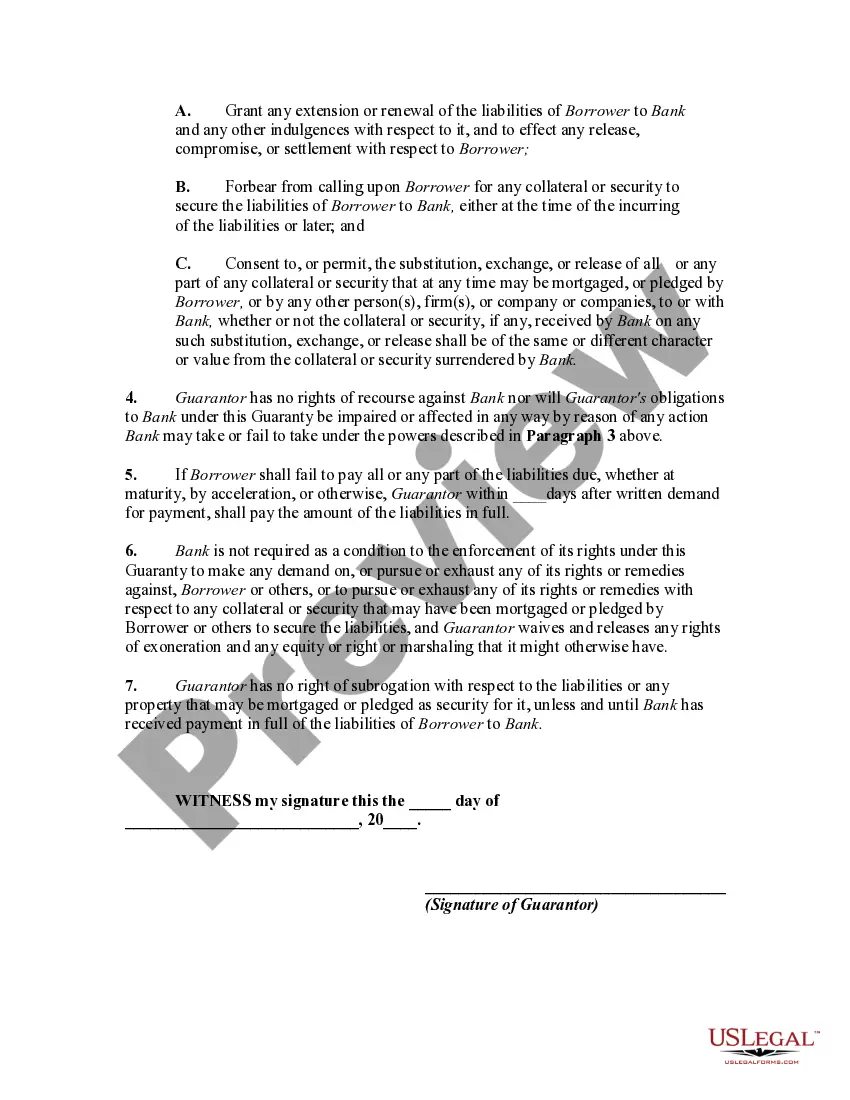

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor.

The contract of guaranty may be absolute or it may be conditional. An absolute guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A line of credit is an arrangement in which a lender extends a specified amount of credit to borrower for a specified time period.

The Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legally binding agreement that provides additional security for the lender when extending a line of credit to a borrower. This type of guarantee ensures that the borrower's obligations will be fulfilled, even if they default on their payments. The Virginia Absolute Guaranty of Payment serves as a safeguard for lenders by holding a third-party guarantor accountable for the borrower's debt in case of default. The guarantor assumes full responsibility for repaying the outstanding amount borrowed under the line of credit. There are different variations of the Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit, including: 1. Individual Guaranty: This type of guaranty involves a single person assuming the responsibility for the borrower's debt. The individual's personal assets and creditworthiness are at stake in case of default. 2. Corporate Guaranty: In this case, a corporation acts as the guarantor, providing assurance that the borrower's debt will be repaid. The corporation's assets and financial stability are liable for repayment if the borrower defaults. 3. Limited Guaranty: A limited guaranty restricts the guarantor's liability to a specific portion or amount of the borrower's debt. This type of guarantee may include limitations on the guarantor's responsibility, such as time restrictions or capping the liability to a certain monetary value. 4. Continuing Guaranty: This type of guaranty covers future extensions of credit, not just the initial line of credit. It ensures that the guarantor remains responsible for any additional credit extended to the borrower beyond the initial agreement. The Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit offers lenders a higher level of security and confidence when providing a line of credit to borrowers. By engaging a third-party guarantor, lenders mitigate their risk and increase the likelihood of full repayment, even in cases of default. It is crucial for all parties involved to thoroughly understand the terms and conditions outlined in the agreement to ensure compliance and protect their interests.The Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legally binding agreement that provides additional security for the lender when extending a line of credit to a borrower. This type of guarantee ensures that the borrower's obligations will be fulfilled, even if they default on their payments. The Virginia Absolute Guaranty of Payment serves as a safeguard for lenders by holding a third-party guarantor accountable for the borrower's debt in case of default. The guarantor assumes full responsibility for repaying the outstanding amount borrowed under the line of credit. There are different variations of the Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit, including: 1. Individual Guaranty: This type of guaranty involves a single person assuming the responsibility for the borrower's debt. The individual's personal assets and creditworthiness are at stake in case of default. 2. Corporate Guaranty: In this case, a corporation acts as the guarantor, providing assurance that the borrower's debt will be repaid. The corporation's assets and financial stability are liable for repayment if the borrower defaults. 3. Limited Guaranty: A limited guaranty restricts the guarantor's liability to a specific portion or amount of the borrower's debt. This type of guarantee may include limitations on the guarantor's responsibility, such as time restrictions or capping the liability to a certain monetary value. 4. Continuing Guaranty: This type of guaranty covers future extensions of credit, not just the initial line of credit. It ensures that the guarantor remains responsible for any additional credit extended to the borrower beyond the initial agreement. The Virginia Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit offers lenders a higher level of security and confidence when providing a line of credit to borrowers. By engaging a third-party guarantor, lenders mitigate their risk and increase the likelihood of full repayment, even in cases of default. It is crucial for all parties involved to thoroughly understand the terms and conditions outlined in the agreement to ensure compliance and protect their interests.