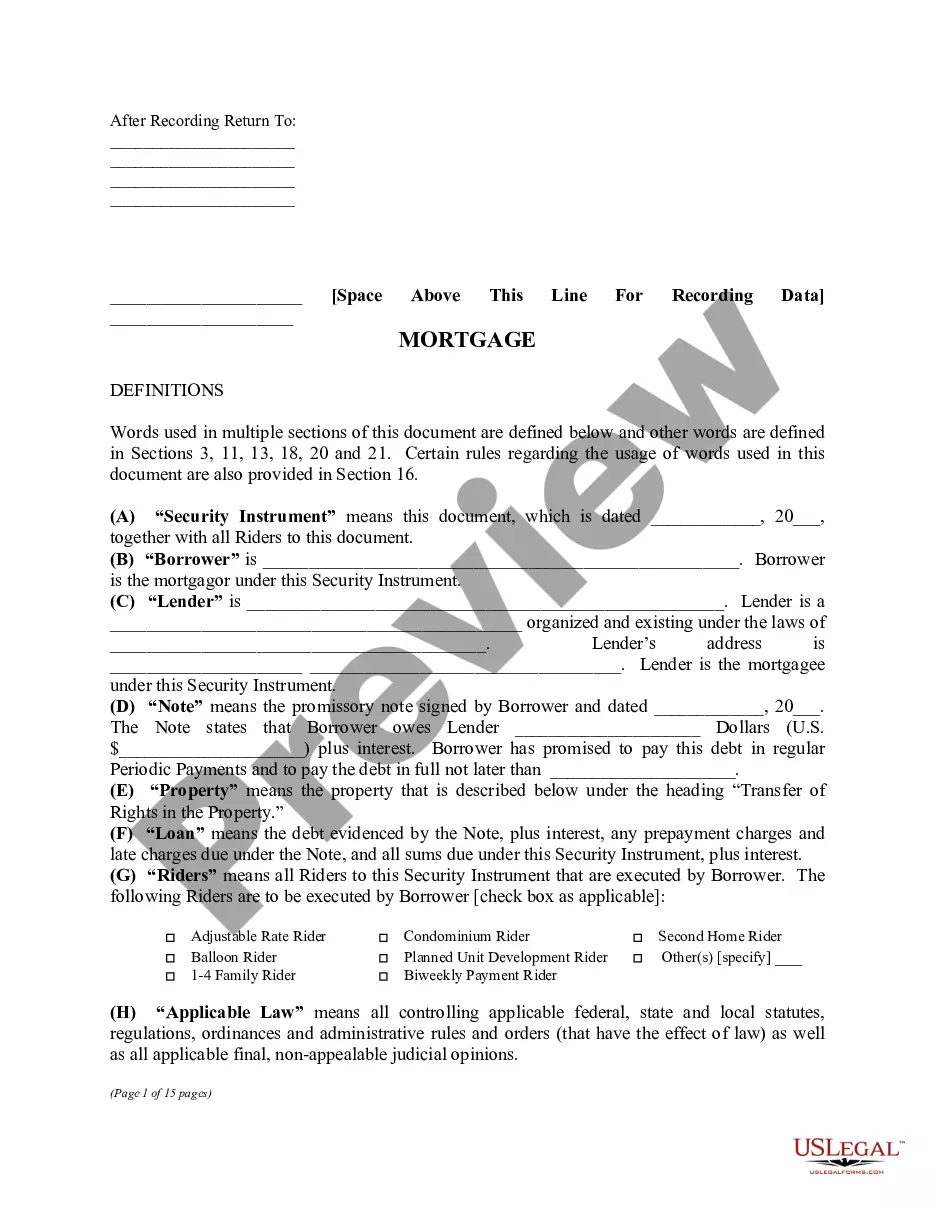

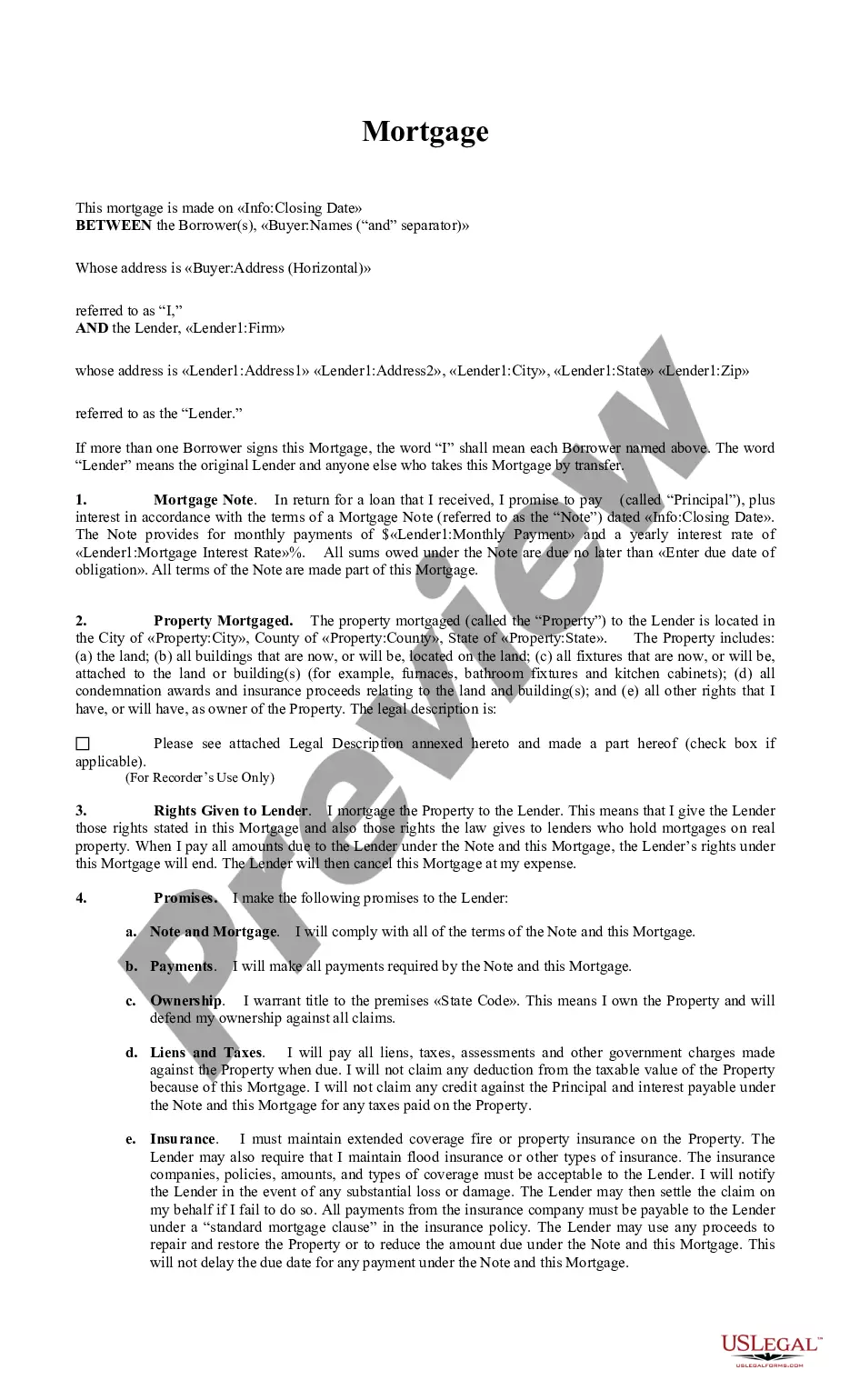

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

Virginia Home Equity Conversion Mortgage - Reverse Mortgage

State:

Multi-State

Control #:

US-01685BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Home Equity Conversion Mortgage - Reverse Mortgage?

If you require to complete, download, or print sanctioned document templates, utilize US Legal Forms, the largest assortment of legal forms available online. Utilize the site’s simple and user-friendly search to locate the documents you need. Various templates for business and specific purposes are organized by categories and claims, or search terms. Utilize US Legal Forms to find the Virginia Home Equity Conversion Mortgage - Reverse Mortgage with just a few clicks.

When you are already a US Legal Forms client, Log In to your account and click on the Obtain button to acquire the Virginia Home Equity Conversion Mortgage - Reverse Mortgage. You can also access forms you previously obtained in the My documents tab of your account.

If you are using US Legal Forms for the first time, refer to the instructions below: Step 1. Ensure you have selected the form for the correct city/region. Step 2. Use the Review option to examine the form’s contents. Do not forget to read the information. Step 3. If you are dissatisfied with the form, use the Lookup field at the top of the screen to find other versions of the legal form template. Step 4. Once you have located the form you need, select the Get now button. Choose the payment plan you prefer and enter your details to register for an account. Step 5. Process the payment. You can use your credit card or PayPal account to complete the transaction. Step 6. Select the format of the legal form and download it to your device. Step 7. Complete, modify and print or sign the Virginia Home Equity Conversion Mortgage - Reverse Mortgage.

Remember not to alter or remove any HTML tags. Only synonymize plain text outside of the HTML tags.

- Every legal document template you purchase is yours indefinitely.

- You have access to every form you acquired in your account.

- Visit the My documents section and select a form to print or download again.

- Stay competitive and download, and print the Virginia Home Equity Conversion Mortgage - Reverse Mortgage with US Legal Forms.

- There are thousands of professional and state-specific forms you can utilize for your business or individual needs.

Form popularity

FAQ

A Home Equity Conversion Mortgage (HECM), the most common type of reverse mortgage, is a special type of home loan only for homeowners who are 62 and older. This information only applies to Home Equity Conversion Mortgages (HECMs), which are the most common type of reverse mortgage loans.

Like the proprietary reverse mortgage, the HECM allows you to borrow against the equity in your home. What makes the HECM different is that it's insured by the FHA, which means it has loan limits and some additional guidelines in place to protect borrowers.

The most common term for reverse mortgages in the UK is equity release. A reverse mortgage is a loan that lets you get money from your home equity?and without having to sell your home. In the UK, you must be at least 55 years to take out a reverse mortgage.

Reverse mortgages represent one way to get the equity out of your home, but they aren't the only way. If you don't qualify for a reverse mortgage but still want to turn your equity to cash, there are options that you can consider.

A traditional private reverse mortgage is not necessarily backed by the federal government, whereas an HECM is not only underwritten by HUD, it is also regulated to consumer safety by the federal government as well. This allows interest rates charged to be far lower.

Cons of HECM You have to live in your home: When you get a HECM, your property must be your principal residence for much of the year. You'll have to pay back the HECM if you sell the home or want to move.

?A reverse mortgage is a home loan that you do not have to pay back for as long as you live in your home. It can be paid to you in one lump sum, as a regular monthly income, or at the times and in the amounts you want. The loan and interest are repaid only when you sell your home, permanently move away, or die.

Cons of HECM You have to live in your home: When you get a HECM, your property must be your principal residence for much of the year. You'll have to pay back the HECM if you sell the home or want to move.