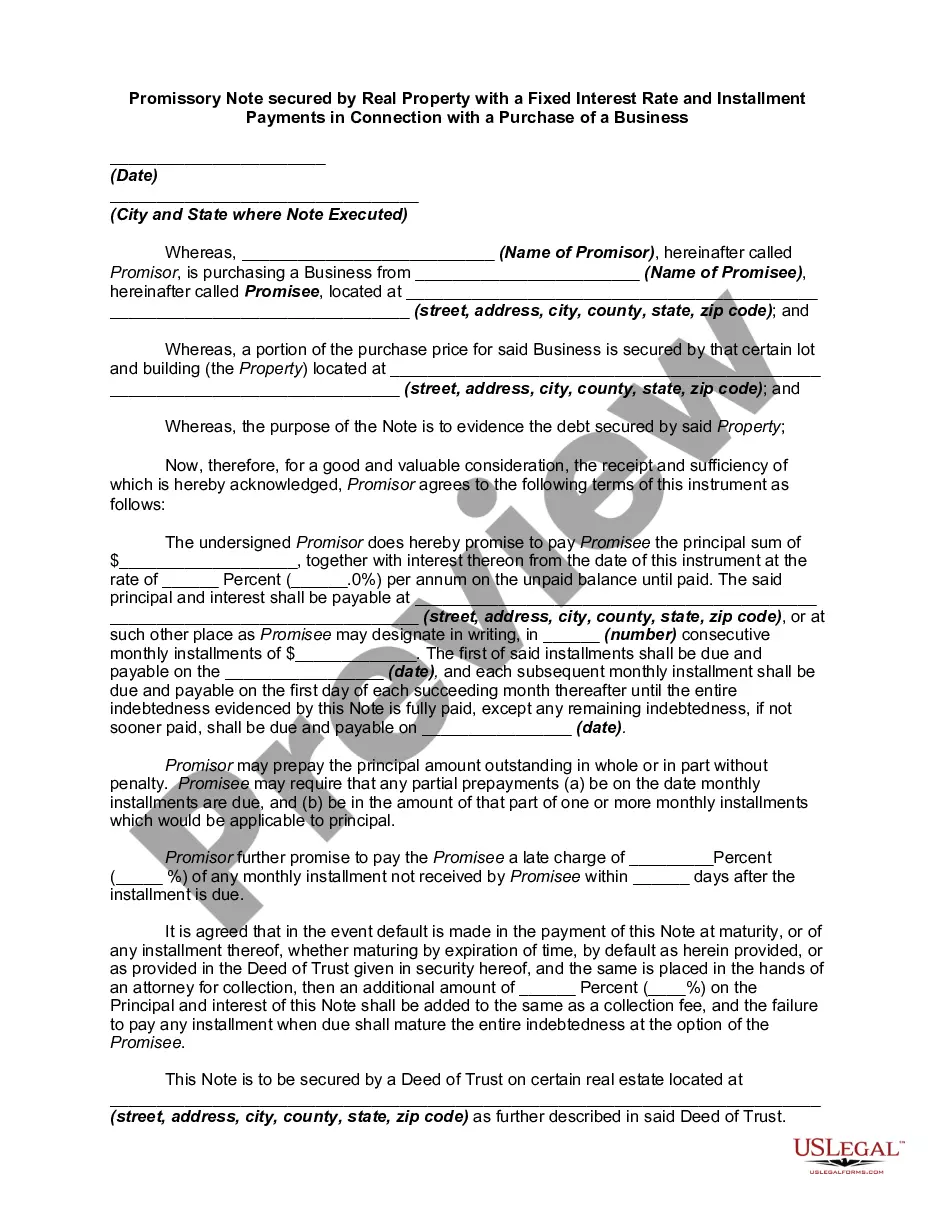

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan. Default terms (what happens if a payment is missed or the loan is not paid off by its due date) should also be spelled out in the promissory note.

A Virginia Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business is a legally binding document that outlines the terms and conditions of a loan agreement between a buyer and a seller in a business purchase transaction. This type of promissory note is commonly used when the buyer requires financing to acquire a business and uses real estate property as collateral to secure the loan. Here are some relevant keywords to understand the concept better: 1. Promissory Note: A written promise by a borrower to repay a specific amount of money within a defined timeframe, including the agreed-upon interest rate and payment terms. 2. Virginia: Refers to the state where the purchase and financing agreement takes place. Each state has its own laws and regulations governing promissory notes and real estate transactions. 3. Secured Loan: The promissory note is secured by real property, meaning that if the buyer defaults on the loan, the lender has the right to take possession of the designated property to recover their investment. 4. Real Property: Refers to land and any structures or improvements attached to it. In this case, the property being used as collateral for the loan is related to the business being purchased. 5. Fixed Interest Rate: The interest rate on the loan remains constant throughout the loan term, ensuring predictable monthly payments for the buyer. 6. Installment Payments: The loan is repaid over a set period in equal installments, typically monthly, including both principal and interest portions. This allows the buyer to manage their cash flow more effectively. Different types of Virginia Promissory Notes secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business may exist based on various factors such as the specific terms negotiated between the buyer and seller, the amount of the loan, and any additional provisions related to default, prepayment penalties, or other contingencies. Some common variations may include: 1. Commercial Promissory Note: When the business being purchased is primarily focused on commercial activities, such as a retail store, restaurant, or office space. 2. Residential Promissory Note: If the business being acquired involves residential real estate properties, such as rental houses or apartment complexes. 3. Bulk Sale Promissory Note: Specifically designed for the purchase of a business that involves high-volume transactions or bulk inventory sales, like a wholesale distribution business. 4. Seller-Financed Promissory Note: If the seller provides the financing directly to the buyer, acting as the lender instead of involving a traditional financial institution. It is crucial to consult with legal professionals or experienced financial advisors to draft a specific promissory note tailored to the unique circumstances of a Virginia business purchase transaction.A Virginia Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business is a legally binding document that outlines the terms and conditions of a loan agreement between a buyer and a seller in a business purchase transaction. This type of promissory note is commonly used when the buyer requires financing to acquire a business and uses real estate property as collateral to secure the loan. Here are some relevant keywords to understand the concept better: 1. Promissory Note: A written promise by a borrower to repay a specific amount of money within a defined timeframe, including the agreed-upon interest rate and payment terms. 2. Virginia: Refers to the state where the purchase and financing agreement takes place. Each state has its own laws and regulations governing promissory notes and real estate transactions. 3. Secured Loan: The promissory note is secured by real property, meaning that if the buyer defaults on the loan, the lender has the right to take possession of the designated property to recover their investment. 4. Real Property: Refers to land and any structures or improvements attached to it. In this case, the property being used as collateral for the loan is related to the business being purchased. 5. Fixed Interest Rate: The interest rate on the loan remains constant throughout the loan term, ensuring predictable monthly payments for the buyer. 6. Installment Payments: The loan is repaid over a set period in equal installments, typically monthly, including both principal and interest portions. This allows the buyer to manage their cash flow more effectively. Different types of Virginia Promissory Notes secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business may exist based on various factors such as the specific terms negotiated between the buyer and seller, the amount of the loan, and any additional provisions related to default, prepayment penalties, or other contingencies. Some common variations may include: 1. Commercial Promissory Note: When the business being purchased is primarily focused on commercial activities, such as a retail store, restaurant, or office space. 2. Residential Promissory Note: If the business being acquired involves residential real estate properties, such as rental houses or apartment complexes. 3. Bulk Sale Promissory Note: Specifically designed for the purchase of a business that involves high-volume transactions or bulk inventory sales, like a wholesale distribution business. 4. Seller-Financed Promissory Note: If the seller provides the financing directly to the buyer, acting as the lender instead of involving a traditional financial institution. It is crucial to consult with legal professionals or experienced financial advisors to draft a specific promissory note tailored to the unique circumstances of a Virginia business purchase transaction.