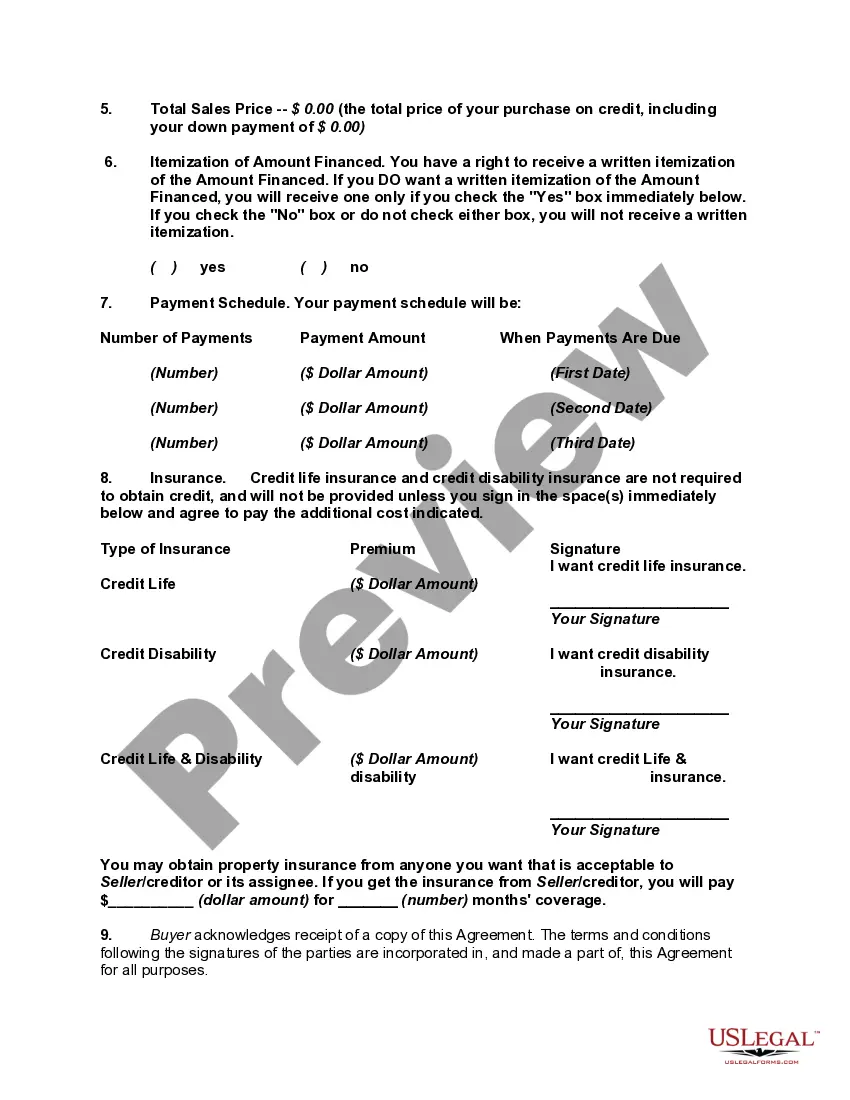

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

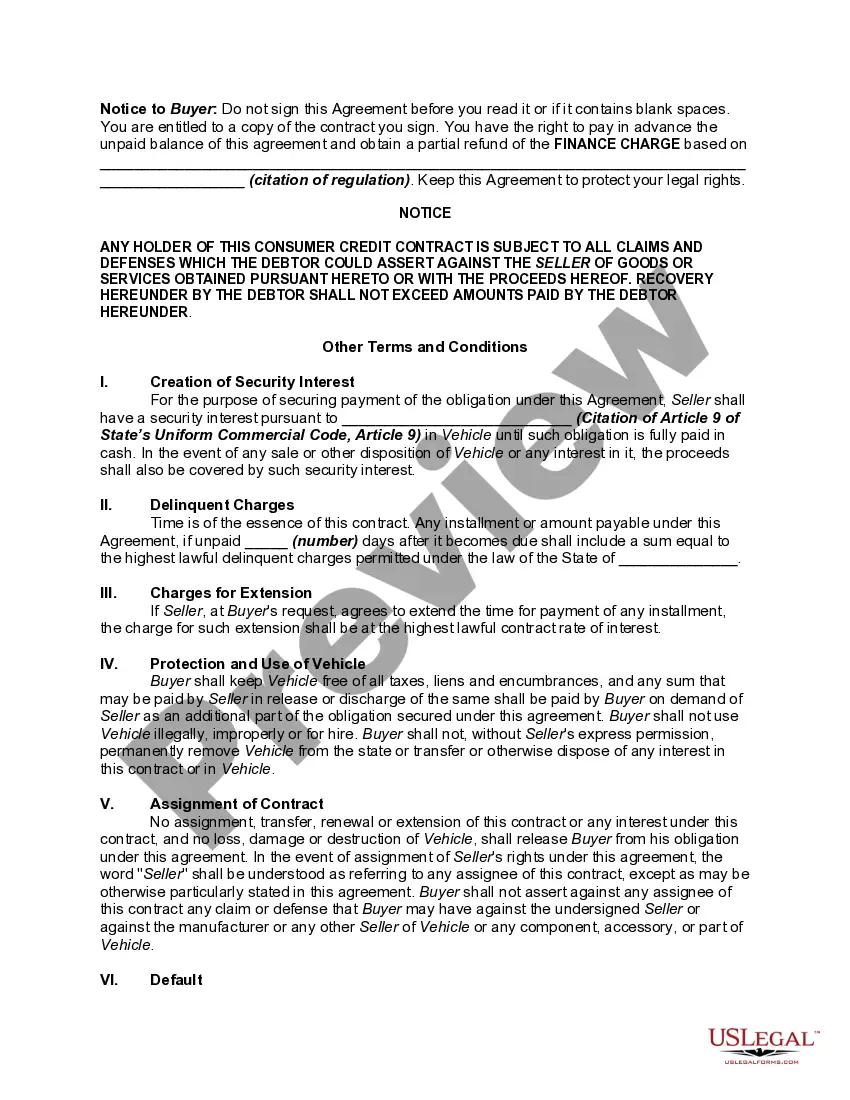

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

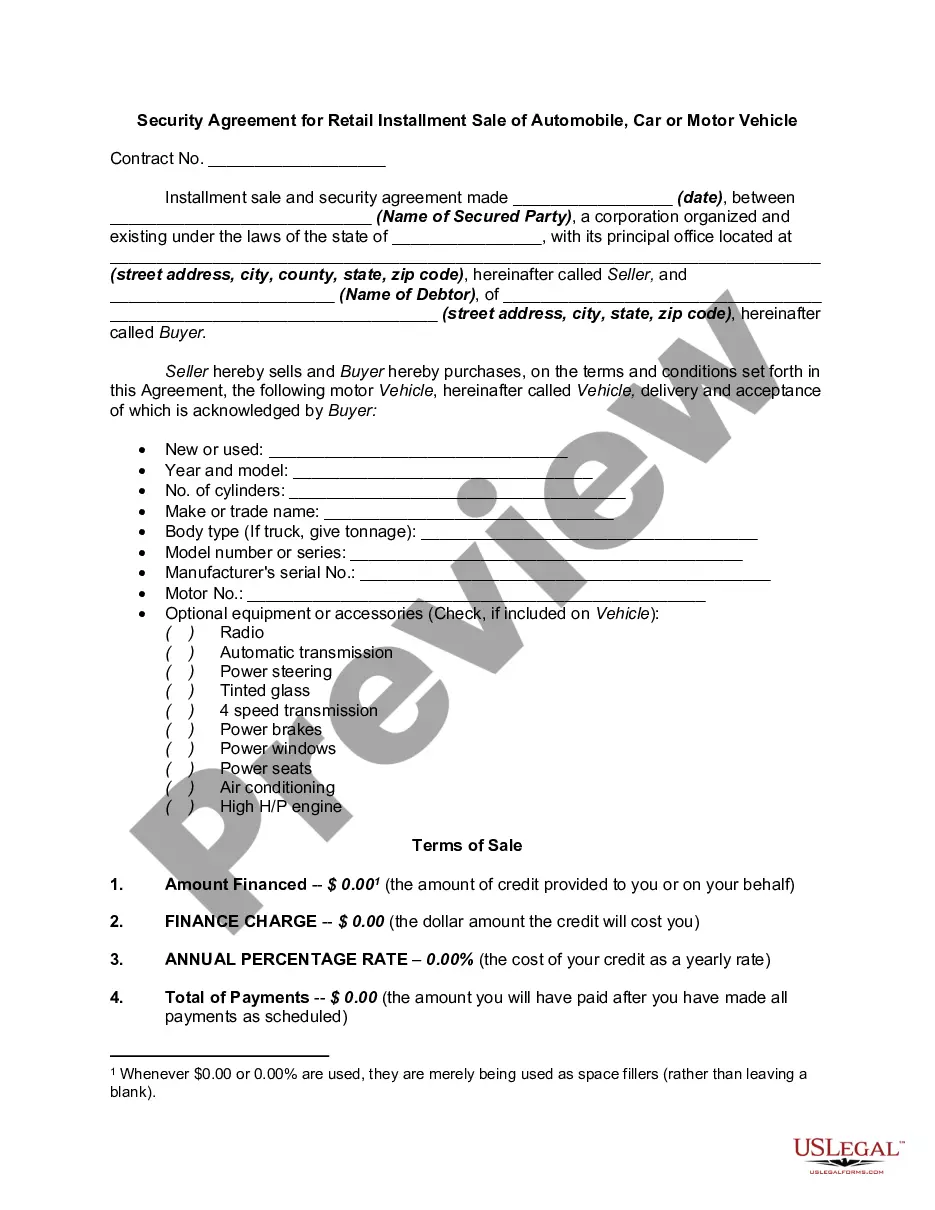

A Virginia Security Agreement is a legally binding document executed between a lender and a borrower in the context of a retail installment sale of an automobile, car, or motor vehicle. This agreement serves as a safeguard for the lender, providing them with a legal recourse in case the borrower defaults on their loan or fails to fulfill their repayment obligations. By entering into a security agreement, the lender can claim the vehicle as collateral in case of nonpayment. In Virginia, there are several types of security agreements for retail installment sales of automobiles, cars, or motor vehicles. These agreements may vary depending on the specific circumstances and parties involved. The most common types include the following: 1. Virginia Security Agreement for Retail Installment Sale of New Automobiles: This type of agreement pertains specifically to the sale of new vehicles and outlines the terms and conditions of the loan, including the repayment schedule, interest rates, and consequences of default. 2. Virginia Security Agreement for Retail Installment Sale of Used Cars: In the case of used cars, a different security agreement may be required. This agreement specifies the terms and conditions for purchasing pre-owned vehicles, including any warranties, maintenance responsibilities, and loan repayment details. 3. Virginia Security Agreement for Retail Installment Sale of Motorcycles: This agreement is specifically designed for motorcycle purchases. It covers the financing terms related to the sale of a motorcycle, including interest rates, repayment schedules, and policies regarding default. 4. Virginia Security Agreement for Retail Installment Sale of Recreational Vehicles: This type of agreement pertains to the sale of recreational vehicles such as motor homes, campers, or RVs. It outlines the terms and conditions for purchasing these specialized vehicles, including loan repayment and collateral terms. 5. Virginia Security Agreement for Retail Installment Sale of Commercial Vehicles: For the sale of commercial vehicles such as trucks or vans, a unique security agreement is often used. It includes specific provisions related to the commercial use of the vehicle, as well as repayment terms and conditions. Regardless of the specific type of Virginia Security Agreement for Retail Installment Sale of Automobile, Car, or Motor Vehicle, it is crucial for both lenders and borrowers to fully understand the terms outlined in the agreement. Seeking legal advice or consulting an attorney can help ensure that all parties are aware of their rights and responsibilities, thereby promoting a fair and transparent transaction.