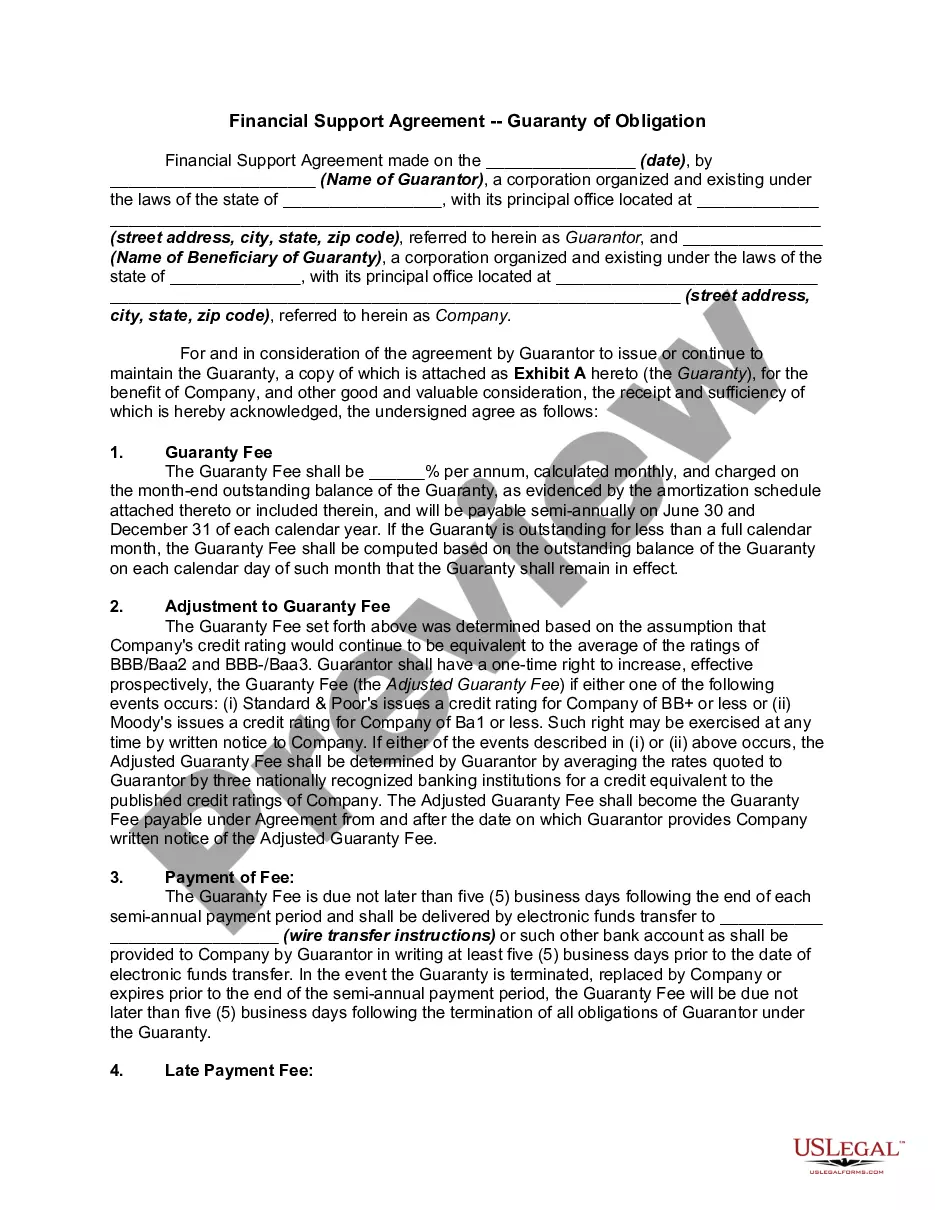

In this agreement, one corporation (the Guarantor) is providing financial assistance to another Corporation (the Corporation) by guaranteeing certain indebtedness for the Company in exchange for a guaranty fee.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Virginia Financial Support Agreement — Guaranty of Obligation is a legally binding document that outlines the financial assurances provided by a party, known as the guarantor, to ensure the fulfillment of certain obligations or debts owed by another party, referred to as the primary debtor. This agreement provides a form of security for the creditor, as it guarantees the payment or performance of the primary debtor's obligations in case of default or non-payment. Keywords: Virginia Financial Support Agreement, Guaranty of Obligation, financial assurances, obligations, debts, guarantor, primary debtor, security, creditor, payment, performance, default, non-payment. There are different types of Virginia Financial Support Agreement — Guaranty of Obligation that can be categorized based on their purpose and scope: 1. Unconditional Guaranty: In this type of agreement, the guarantor assumes full responsibility for the primary debtor's obligations without any conditions or limitations. The guarantor is obliged to fulfill all financial obligations of the primary debtor if they fail to do so. 2. Conditional Guaranty: This form of agreement imposes specific conditions or requirements on the guarantor to be liable for the primary debtor's obligations. The guarantor's responsibility is triggered only if these conditions are met. 3. Limited Guaranty: A limited guaranty is an agreement that restricts the guarantor's liability to a specific amount or period. It provides a predetermined limit on the guarantor's obligations, limiting their liability accordingly. 4. Continuing Guaranty: This type of agreement extends the guarantor's responsibilities beyond a specific transaction or period. It covers ongoing or future obligations that may arise during a long-term business relationship. 5. Absolute Guaranty: An absolute guaranty places an unconditional obligation on the guarantor to fulfill the primary debtor's obligations entirely. Regardless of any disputes, defenses, or counterclaims that the primary debtor may raise, the guarantor remains responsible. 6. Limited Recourse Guaranty: In a limited recourse guaranty, the guarantor's liability is restricted to specific assets or collateral held by the guarantor. If the primary debtor fails to fulfill their obligations, the creditor can only go after the designated assets specified in the agreement. It is crucial to carefully review and understand the terms and conditions of a Virginia Financial Support Agreement — Guaranty of Obligation to ensure that all parties involved comprehend their rights, duties, and obligations under the agreement. Seeking legal advice is recommended to ensure compliance with applicable laws and to protect the interests of the parties involved.The Virginia Financial Support Agreement — Guaranty of Obligation is a legally binding document that outlines the financial assurances provided by a party, known as the guarantor, to ensure the fulfillment of certain obligations or debts owed by another party, referred to as the primary debtor. This agreement provides a form of security for the creditor, as it guarantees the payment or performance of the primary debtor's obligations in case of default or non-payment. Keywords: Virginia Financial Support Agreement, Guaranty of Obligation, financial assurances, obligations, debts, guarantor, primary debtor, security, creditor, payment, performance, default, non-payment. There are different types of Virginia Financial Support Agreement — Guaranty of Obligation that can be categorized based on their purpose and scope: 1. Unconditional Guaranty: In this type of agreement, the guarantor assumes full responsibility for the primary debtor's obligations without any conditions or limitations. The guarantor is obliged to fulfill all financial obligations of the primary debtor if they fail to do so. 2. Conditional Guaranty: This form of agreement imposes specific conditions or requirements on the guarantor to be liable for the primary debtor's obligations. The guarantor's responsibility is triggered only if these conditions are met. 3. Limited Guaranty: A limited guaranty is an agreement that restricts the guarantor's liability to a specific amount or period. It provides a predetermined limit on the guarantor's obligations, limiting their liability accordingly. 4. Continuing Guaranty: This type of agreement extends the guarantor's responsibilities beyond a specific transaction or period. It covers ongoing or future obligations that may arise during a long-term business relationship. 5. Absolute Guaranty: An absolute guaranty places an unconditional obligation on the guarantor to fulfill the primary debtor's obligations entirely. Regardless of any disputes, defenses, or counterclaims that the primary debtor may raise, the guarantor remains responsible. 6. Limited Recourse Guaranty: In a limited recourse guaranty, the guarantor's liability is restricted to specific assets or collateral held by the guarantor. If the primary debtor fails to fulfill their obligations, the creditor can only go after the designated assets specified in the agreement. It is crucial to carefully review and understand the terms and conditions of a Virginia Financial Support Agreement — Guaranty of Obligation to ensure that all parties involved comprehend their rights, duties, and obligations under the agreement. Seeking legal advice is recommended to ensure compliance with applicable laws and to protect the interests of the parties involved.