Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

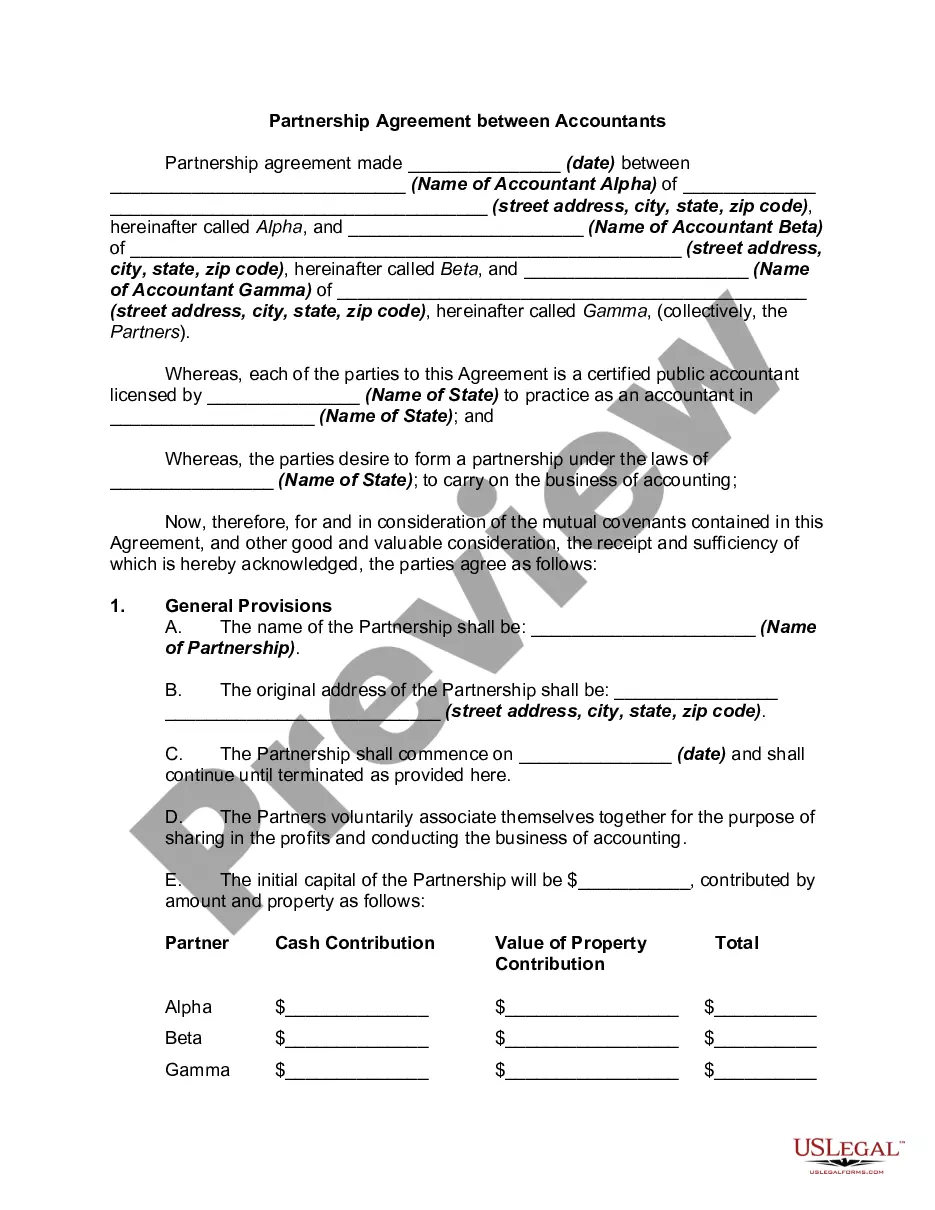

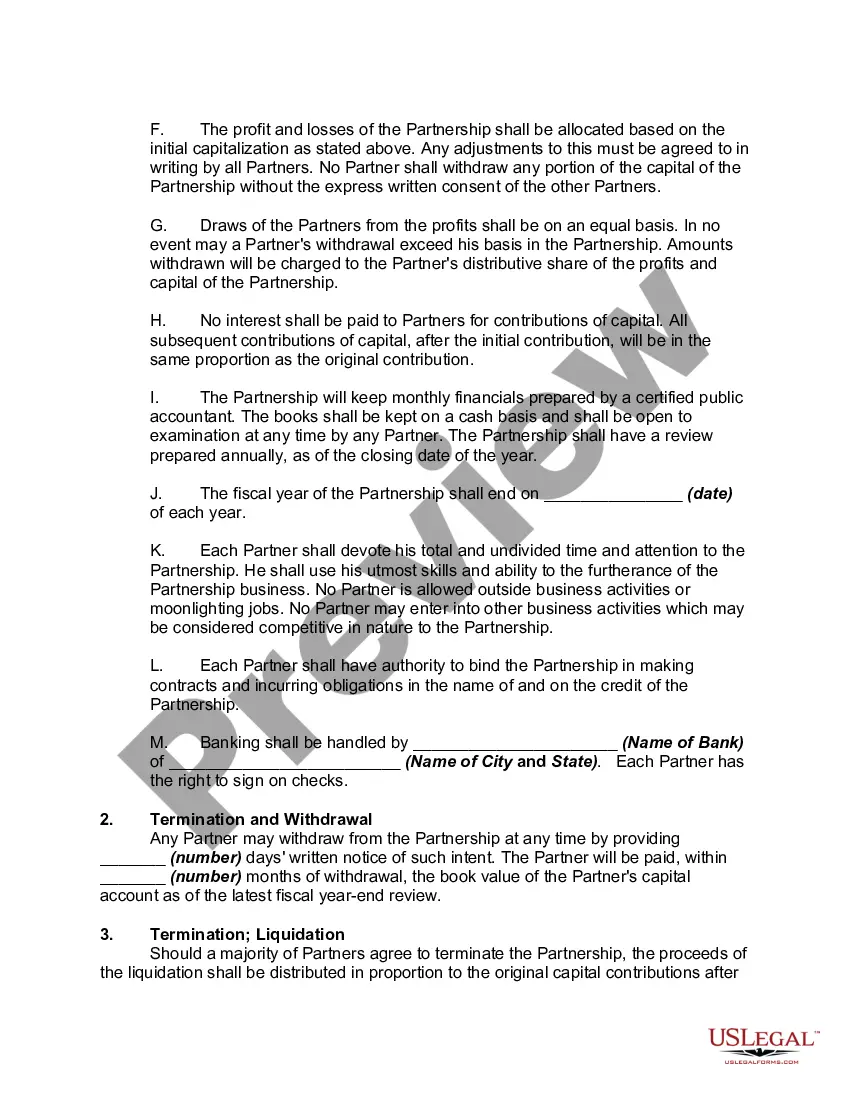

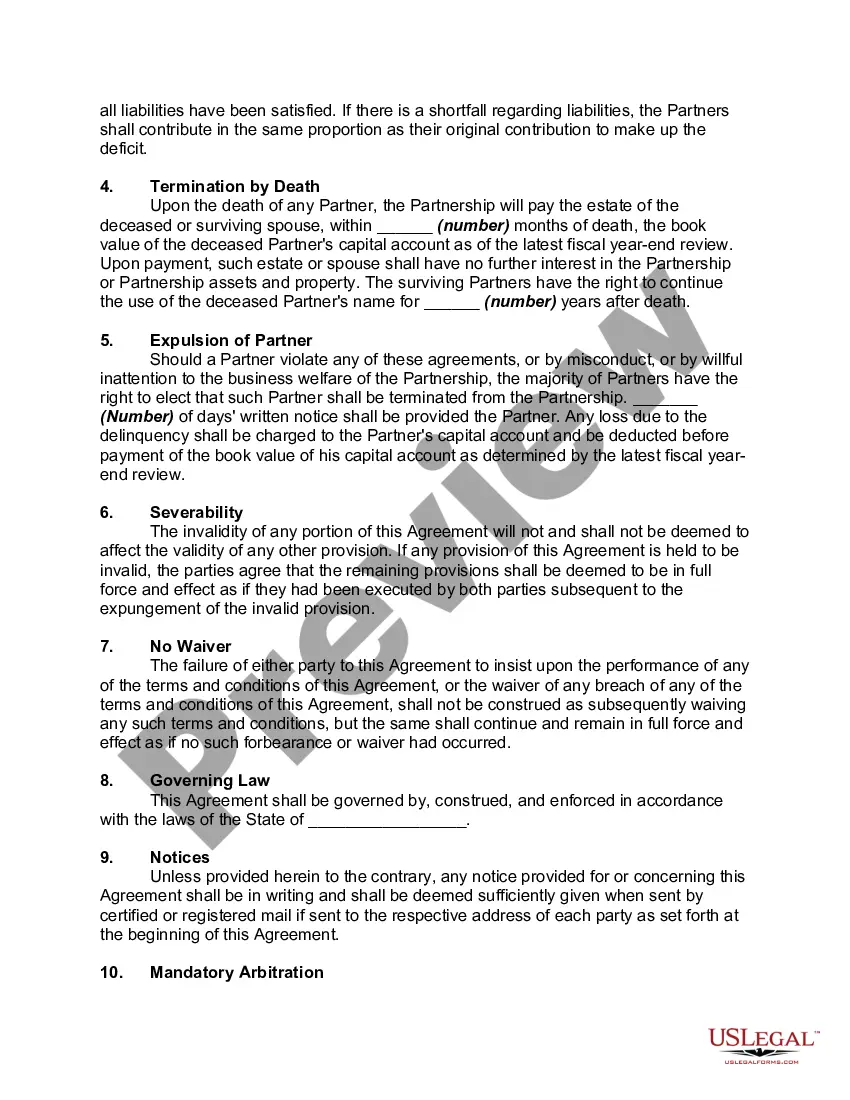

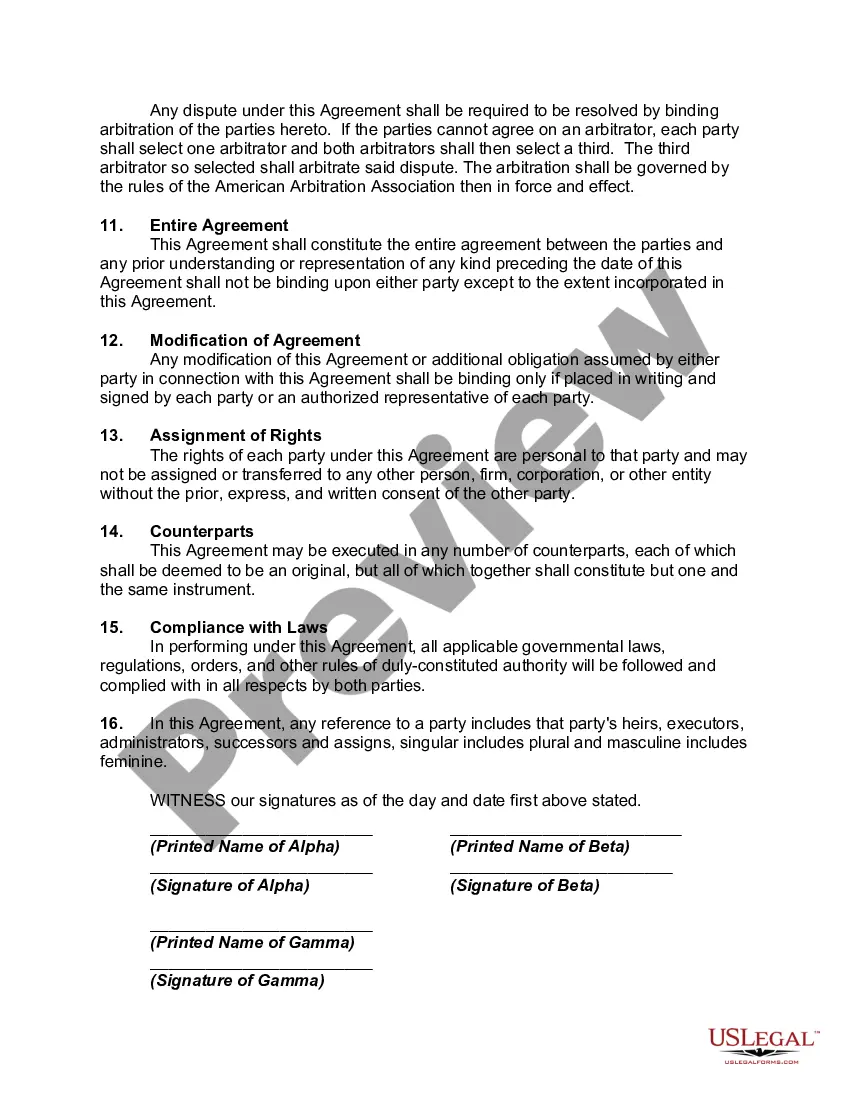

Virginia Partnership Agreement Between Accountants is a legal document that outlines the rights, responsibilities, and obligations of two or more accountants who have decided to form a partnership in the state of Virginia. This agreement ensures a clear understanding between the partners and helps establish a framework for their professional relationship. A Partnership Agreement is essential for accountants looking to set up their practice in Virginia and provides a comprehensive guide on how the partnership will operate. The agreement covers various essential aspects, including partnership contributions, profit-sharing, decision-making, dispute resolution, and partner withdrawal or dissolution. In Virginia, there are typically two types of Partnership Agreements between accountants: 1. General Partnership Agreement: In a general partnership, all partners assume equal responsibility and liability for the firm's operations. This agreement allows partners to share profits and losses equally, contributing their accounting expertise and financial resources to the partnership. The general partnership agreement should clearly outline each partner's role, authority, and financial contribution. 2. Limited Partnership Agreement: In a limited partnership, there are two types of partners — general partners and limited partners. General partners actively manage the accounting firm and bear unlimited liability for the partnership's obligations. On the other hand, limited partners are passive investors who enjoy limited liability for the partnership's debts and liabilities. This agreement specifies the roles, responsibilities, and profit distribution between general and limited partners. Key elements typically found in a Virginia Partnership Agreement Between Accountants include: — Partnership Name: The official name of the accounting partnership. — Purpose: Clearly defines the objectives and scope of the partnership. — Capital Contributions: Specifies the initial financial contributions made by each partner and clarifies how additional capital will be raised if needed. — Profits and Losses: Describes how profits and losses will be distributed among partners, such as equally or based on a predetermined percentage. — Decision-Making: Outlines the decision-making process for the partnership, including voting rights, quorum requirements, and procedures for resolving disagreements. — Partner Withdrawal or Dissolution: Details the process for a partner to withdraw or dissolve the partnership, including buyout options and any associated consequences. — Non-compete Clauses: May include restrictions on partners competing with the partnership during or after its existence. — Dispute Resolution: Specifies mechanisms for resolving disputes, such as mediation or arbitration, to avoid potential litigation. — Governing Law: Identifies the state laws, particularly Virginia partnership laws, that govern the agreement and the partnership's activities. Overall, a Virginia Partnership Agreement Between Accountants establishes a strong foundation for a professional partnership, ensuring clarity, fairness, and legal compliance in all aspects of the accounting practice. It is recommended that partners seek legal counsel to draft or review the agreement to protect their interests and ensure its enforceability under Virginia law.Virginia Partnership Agreement Between Accountants is a legal document that outlines the rights, responsibilities, and obligations of two or more accountants who have decided to form a partnership in the state of Virginia. This agreement ensures a clear understanding between the partners and helps establish a framework for their professional relationship. A Partnership Agreement is essential for accountants looking to set up their practice in Virginia and provides a comprehensive guide on how the partnership will operate. The agreement covers various essential aspects, including partnership contributions, profit-sharing, decision-making, dispute resolution, and partner withdrawal or dissolution. In Virginia, there are typically two types of Partnership Agreements between accountants: 1. General Partnership Agreement: In a general partnership, all partners assume equal responsibility and liability for the firm's operations. This agreement allows partners to share profits and losses equally, contributing their accounting expertise and financial resources to the partnership. The general partnership agreement should clearly outline each partner's role, authority, and financial contribution. 2. Limited Partnership Agreement: In a limited partnership, there are two types of partners — general partners and limited partners. General partners actively manage the accounting firm and bear unlimited liability for the partnership's obligations. On the other hand, limited partners are passive investors who enjoy limited liability for the partnership's debts and liabilities. This agreement specifies the roles, responsibilities, and profit distribution between general and limited partners. Key elements typically found in a Virginia Partnership Agreement Between Accountants include: — Partnership Name: The official name of the accounting partnership. — Purpose: Clearly defines the objectives and scope of the partnership. — Capital Contributions: Specifies the initial financial contributions made by each partner and clarifies how additional capital will be raised if needed. — Profits and Losses: Describes how profits and losses will be distributed among partners, such as equally or based on a predetermined percentage. — Decision-Making: Outlines the decision-making process for the partnership, including voting rights, quorum requirements, and procedures for resolving disagreements. — Partner Withdrawal or Dissolution: Details the process for a partner to withdraw or dissolve the partnership, including buyout options and any associated consequences. — Non-compete Clauses: May include restrictions on partners competing with the partnership during or after its existence. — Dispute Resolution: Specifies mechanisms for resolving disputes, such as mediation or arbitration, to avoid potential litigation. — Governing Law: Identifies the state laws, particularly Virginia partnership laws, that govern the agreement and the partnership's activities. Overall, a Virginia Partnership Agreement Between Accountants establishes a strong foundation for a professional partnership, ensuring clarity, fairness, and legal compliance in all aspects of the accounting practice. It is recommended that partners seek legal counsel to draft or review the agreement to protect their interests and ensure its enforceability under Virginia law.