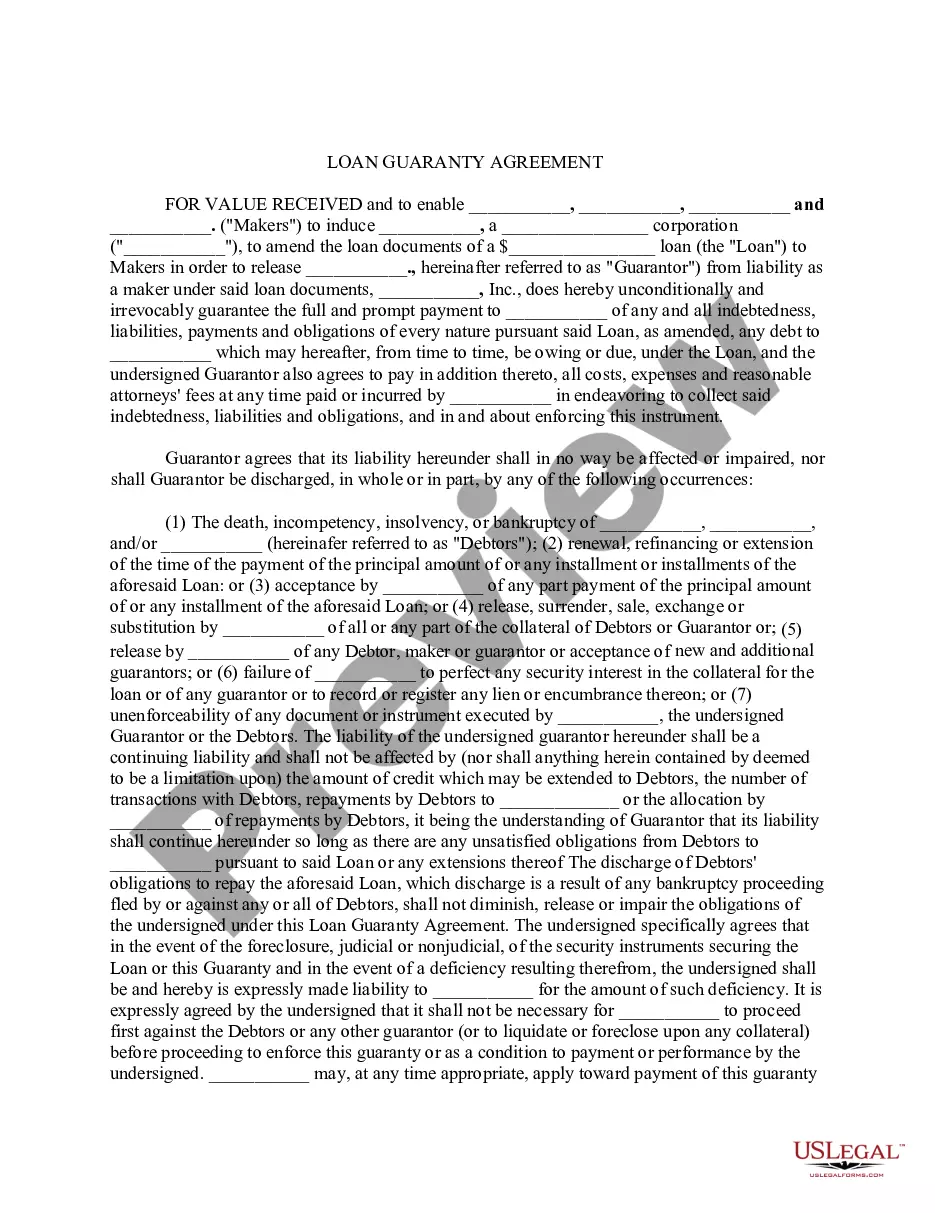

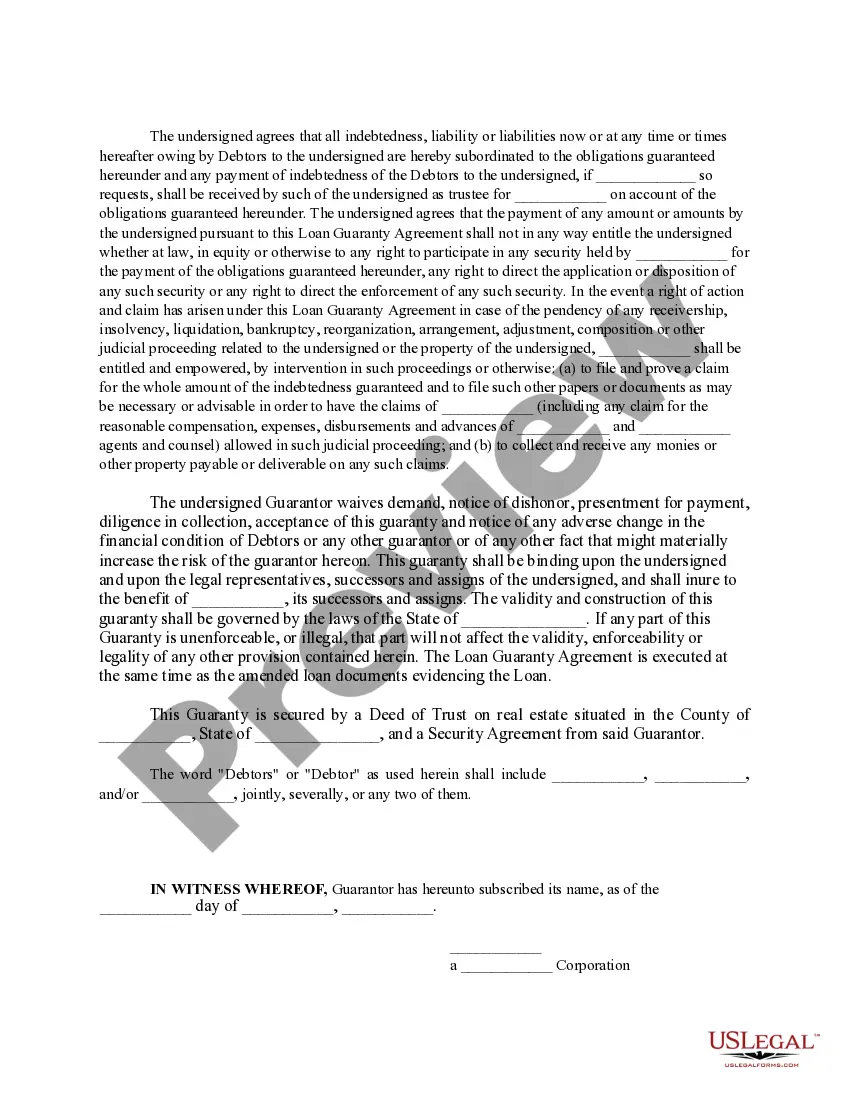

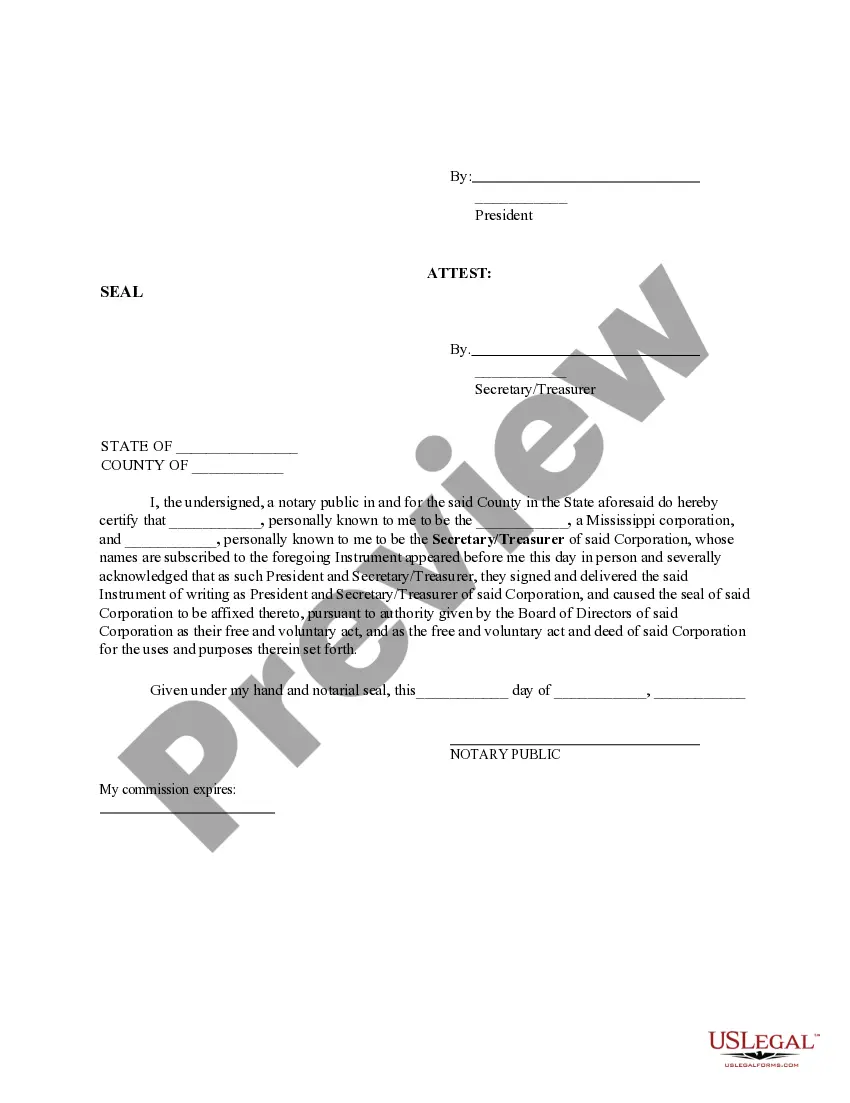

A Virginia Loan Guaranty Agreement is a legal document that outlines the terms and conditions for providing financial guarantee or backing to a borrower by a third-party guarantor in the state of Virginia. This agreement is usually entered into when a borrower is seeking a loan from a financial institution, and the lender requires additional security or assurance against potential default or non-payment. The Virginia Loan Guaranty Agreement specifies the obligations and responsibilities of the guarantor in case the borrower fails to honor their loan repayment obligations. This agreement serves as collateral for the lender, providing them with a financial safety net and reducing the risk associated with lending funds. There are several types of Virginia Loan Guaranty Agreements: 1. Personal Loan Guaranty Agreement: This type of agreement is commonly used when an individual is borrowing funds for personal use, such as education, home improvement, or debt consolidation. In this case, a second individual, usually a family member or close friend, acts as the guarantor and agrees to be held liable for the debt if the borrower defaults. 2. Business Loan Guaranty Agreement: This agreement is prevalent in the business world, where small businesses or startups require additional financing to grow their operations. A business loan guarantor, often an individual with a strong credit history or a business partner, pledges to repay the loan in case the business is unable to do so. 3. Government Loan Guaranty Agreement: This type of agreement involves the government, typically through the Virginia Small Business Financing Authority or a similar agency. The government acts as the guarantor, providing assurance to lenders that if a borrower defaults, they will step in and repay a portion of the loan on the borrower's behalf. 4. Real Estate Loan Guaranty Agreement: Real estate transactions often involve large sums of money, and lenders may require a guarantor to mitigate their risk. This type of agreement involves a third party, such as an individual, company, or the government, offering financial support in case the borrower fails to meet their obligations. Virginia Loan Guaranty Agreements are crucial in facilitating lending activities while minimizing the potential losses for lenders. By providing a legal framework for guaranteeing loans, these agreements promote access to credit and support economic growth in Virginia.

Virginia Loan Guaranty Agreement

Description

How to fill out Virginia Loan Guaranty Agreement?

You may devote hours on the Internet attempting to find the legal papers web template that suits the federal and state needs you will need. US Legal Forms supplies a large number of legal varieties that happen to be evaluated by specialists. It is possible to down load or print the Virginia Loan Guaranty Agreement from your services.

If you currently have a US Legal Forms accounts, you may log in and click on the Obtain switch. Following that, you may total, modify, print, or indication the Virginia Loan Guaranty Agreement. Each legal papers web template you acquire is your own property eternally. To acquire an additional backup of the acquired type, go to the My Forms tab and click on the corresponding switch.

Should you use the US Legal Forms site initially, adhere to the simple instructions beneath:

- Initially, be sure that you have selected the best papers web template to the state/town of your liking. See the type description to ensure you have selected the correct type. If readily available, make use of the Preview switch to look throughout the papers web template too.

- If you would like discover an additional model from the type, make use of the Research discipline to obtain the web template that meets your needs and needs.

- After you have found the web template you would like, click Acquire now to carry on.

- Find the pricing program you would like, type your credentials, and register for your account on US Legal Forms.

- Complete the transaction. You can utilize your bank card or PayPal accounts to cover the legal type.

- Find the formatting from the papers and down load it for your gadget.

- Make modifications for your papers if necessary. You may total, modify and indication and print Virginia Loan Guaranty Agreement.

Obtain and print a large number of papers web templates using the US Legal Forms web site, which offers the largest selection of legal varieties. Use professional and express-certain web templates to handle your small business or specific needs.