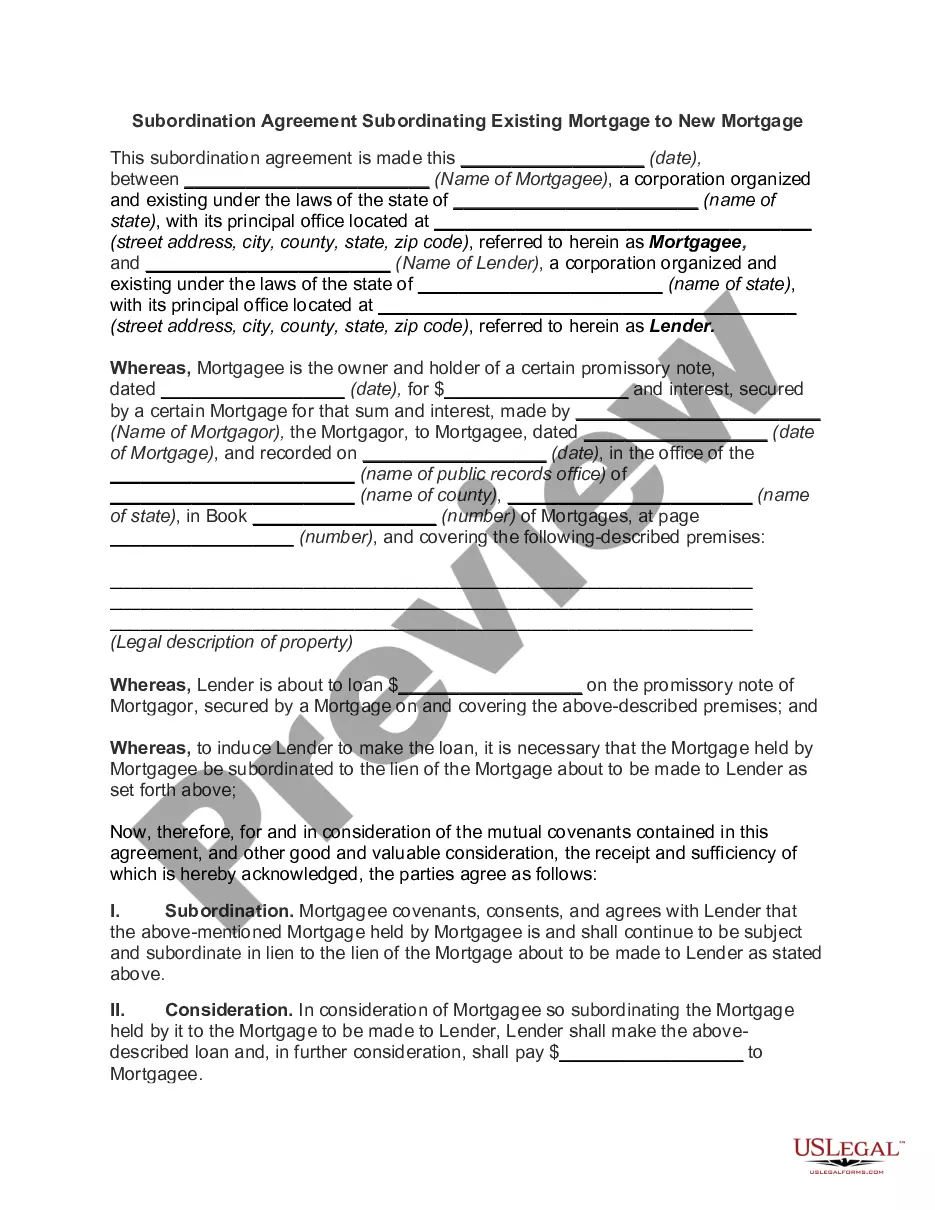

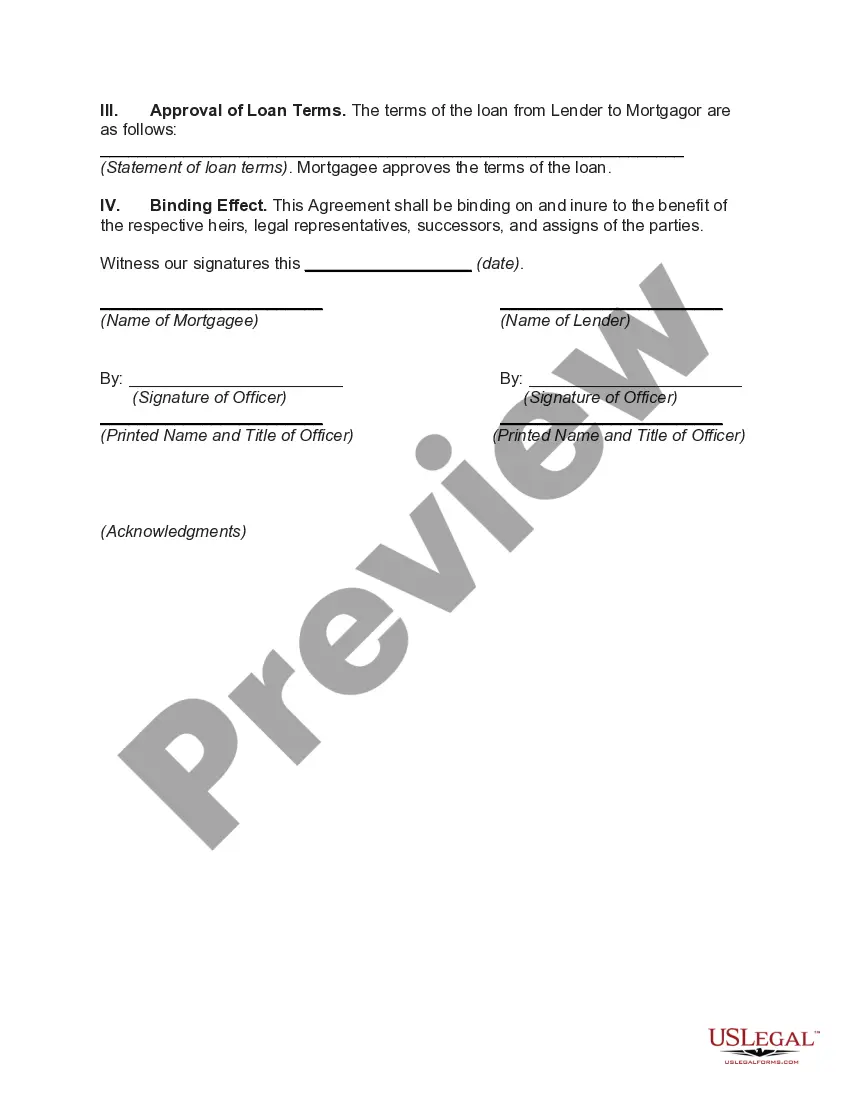

A Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document that is utilized when a property owner wishes to refinance their existing mortgage with a new mortgage while retaining the priority position of their original mortgage. In Virginia, there are primarily two types of Subordination Agreements that can be used in the context of subordinating an existing mortgage to a new mortgage: 1. Virginia Subordination Agreement for Home Equity Loans: This type of agreement is common when homeowners choose to take out a home equity loan or line of credit while the original mortgage is still in place. It allows the new lender to have a secondary lien on the property, with the original mortgage retaining its priority position. 2. Virginia Subordination Agreement for Mortgage Assumptions: When a property with an existing mortgage is being sold or transferred to a new owner who intends to assume the existing mortgage, a subordination agreement is typically required. The agreement allows the new owner's lender to take a subordinate position to the original mortgage, ensuring the existing lender's priority interest in the property. In both cases, the purpose of the Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage is to establish the rights and priorities of the parties involved, ensuring that the new mortgage does not supersede the original mortgage in terms of priority. The agreement outlines the terms and conditions of the subordination, including any fees or considerations involved. Keywords: Virginia, Subordination Agreement, Subordinating, Existing Mortgage, New Mortgage, Home Equity Loans, Mortgage Assumptions, Refinance, Priority Position, Lien, Legal Document, Property, Owner, Original Mortgage, Homeowners, Secondary Lien, Assumption, Rights, Parties, Terms, Conditions, Fees.

Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Virginia Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

US Legal Forms - one of several biggest libraries of legitimate varieties in the USA - delivers a wide array of legitimate papers layouts you can acquire or produce. Utilizing the site, you can find thousands of varieties for business and specific functions, categorized by classes, says, or keywords and phrases.You will find the latest models of varieties much like the Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage within minutes.

If you have a registration, log in and acquire Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage from the US Legal Forms catalogue. The Down load switch can look on every type you look at. You have access to all formerly downloaded varieties in the My Forms tab of your accounts.

If you want to use US Legal Forms initially, listed below are easy guidelines to get you started out:

- Be sure to have picked out the correct type for your town/area. Click on the Preview switch to review the form`s articles. Look at the type explanation to actually have chosen the proper type.

- In case the type does not suit your specifications, utilize the Look for area on top of the screen to get the one which does.

- When you are pleased with the shape, verify your choice by visiting the Purchase now switch. Then, choose the rates plan you favor and supply your accreditations to register for an accounts.

- Procedure the deal. Make use of bank card or PayPal accounts to perform the deal.

- Select the structure and acquire the shape on your own product.

- Make alterations. Complete, revise and produce and signal the downloaded Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

Each and every design you put into your account lacks an expiry particular date and is yours permanently. So, if you wish to acquire or produce yet another version, just go to the My Forms portion and click on on the type you need.

Get access to the Virginia Subordination Agreement Subordinating Existing Mortgage to New Mortgage with US Legal Forms, by far the most considerable catalogue of legitimate papers layouts. Use thousands of skilled and state-certain layouts that fulfill your small business or specific requires and specifications.