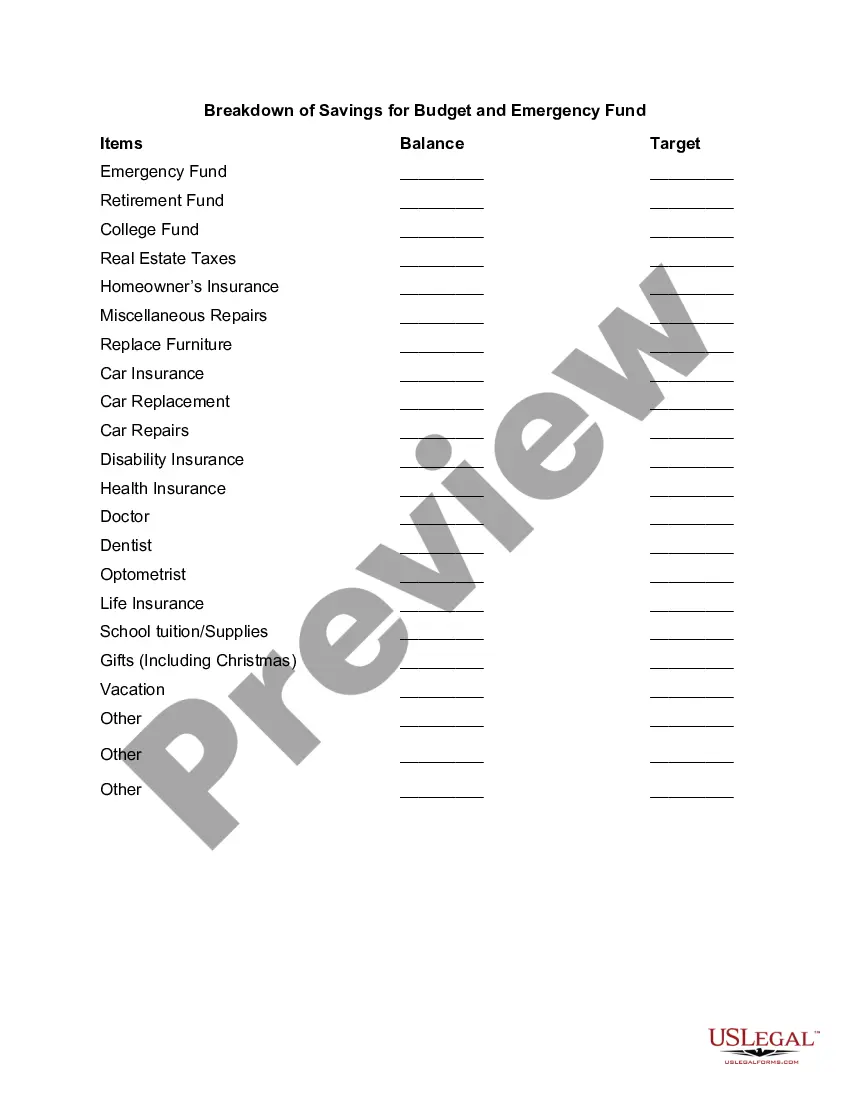

Title: Virginia Breakdown of Savings for Budget and Emergency Fund: Understanding Types and Importance Introduction: Having a well-structured savings plan is essential for financial stability and security. In Virginia, individuals prioritize saving their money to build both a budget and an emergency fund. This article aims to provide a detailed description of the breakdown of savings for budgeting and emergency funds, highlighting their importance and various types present in Virginia. 1. Budget Savings: Budget savings refer to setting aside a portion of income to cover regular expenses and achieve financial goals. These savings are further categorized into: a. Essential Expenses: This category includes bills, rent/mortgage payments, groceries, transportation, healthcare, and education expenses. It is crucial for Virginians to allocate a significant portion of their budget savings towards essential expenses. b. Discretionary Expenses: Discretionary expenses are non-essential, optional expenses such as dining out, entertainment, vacations, luxury purchases, and hobbies. Allocating a reasonable portion of budget savings towards discretionary expenses ensures a balanced lifestyle without overspending. c. Debt Repayment: Virginia residents must allocate a portion of their budget savings towards paying off debts like credit card balances, student loans, or outstanding loans. Prioritizing debt repayment can reduce interest costs and improve overall financial health. 2. Emergency Fund: An emergency fund acts as a financial safety net, providing stability in times of unexpected events, such as job loss, medical emergencies, or unplanned home repairs. Various types of emergency funds include: a. Basic Emergency Fund: This fund covers essential living expenses for a specific period, typically three to six months, in case of unemployment or other unforeseen circumstances. It helps Virginians maintain their financial stability during emergencies. b. Medical Emergency Fund: Many Virginians opt to create a separate emergency fund targeted specifically for medical expenses. This fund ensures that any unforeseen medical emergencies or surgeries are adequately covered, reducing financial burdens. c. Home Repair Fund: A dedicated home repair fund is crucial for homeowners in Virginia. It helps cover unexpected repairs or renovations, ensuring the maintenance and longevity of one's property. d. Education Emergency Fund: Virginia residents often prioritize setting aside funds for unexpected educational expenses, like funding their children's education or attending professional development courses. This type of emergency fund minimizes the impact of sudden education-related financial needs. Conclusion: Building a robust savings plan in Virginia is vital for financial peace of mind and stability. By understanding the breakdown of savings for budgeting and emergency funds, Virginians can effectively manage their income, cover essential expenses, and prepare for unexpected circumstances. The key lies in prioritizing budget savings, allocating funds toward essential and discretionary expenses, and establishing an emergency fund that caters to various potential emergencies such as medical, home repairs, and education.

Virginia Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Virginia Breakdown Of Savings For Budget And Emergency Fund?

You are able to commit time on the web attempting to find the legal papers design that meets the state and federal demands you will need. US Legal Forms offers thousands of legal kinds which can be reviewed by professionals. It is possible to download or produce the Virginia Breakdown of Savings for Budget and Emergency Fund from your assistance.

If you currently have a US Legal Forms accounts, you may log in and click the Down load switch. After that, you may full, change, produce, or indication the Virginia Breakdown of Savings for Budget and Emergency Fund. Every single legal papers design you acquire is your own forever. To have yet another version of the acquired kind, visit the My Forms tab and click the corresponding switch.

If you are using the US Legal Forms web site for the first time, adhere to the simple instructions under:

- Initially, ensure that you have chosen the correct papers design for the region/town of your choice. Browse the kind outline to make sure you have selected the appropriate kind. If readily available, take advantage of the Review switch to look from the papers design as well.

- If you wish to get yet another variation of the kind, take advantage of the Look for discipline to discover the design that meets your needs and demands.

- After you have discovered the design you would like, simply click Buy now to proceed.

- Select the pricing program you would like, type your qualifications, and register for a merchant account on US Legal Forms.

- Full the deal. You can utilize your charge card or PayPal accounts to pay for the legal kind.

- Select the file format of the papers and download it for your device.

- Make adjustments for your papers if needed. You are able to full, change and indication and produce Virginia Breakdown of Savings for Budget and Emergency Fund.

Down load and produce thousands of papers web templates utilizing the US Legal Forms Internet site, which provides the biggest variety of legal kinds. Use skilled and express-specific web templates to handle your organization or specific requires.