This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

Virginia Credit Inquiry

Category:

State:

Multi-State

Control #:

US-135-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Credit Inquiry?

Selecting the finest legal document template can be a challenge.

Certainly, there are numerous templates available online, but how do you acquire the legal form you require.

Utilize the US Legal Forms platform.

If you are a new user of US Legal Forms, here are some simple steps to follow: First, ensure you have selected the correct document for your locality. You can preview the form using the Preview button and review the form details to make sure this is indeed the right one for you.

- The service provides a plethora of templates, including the Virginia Credit Inquiry, suitable for both business and personal purposes.

- All forms are reviewed by specialists and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Download button to fetch the Virginia Credit Inquiry.

- Use your account to browse the legal documents you have previously obtained.

- Visit the My documents section of your account to download another copy of the document you need.

Form popularity

FAQ

Hard inquiries have a negative impact on your credit score, in the short term at least. While a hard inquiry will stay on your credit report for two years, it will usually only impact your credit for a few months.

No, requesting your credit report will not hurt your credit score. Checking your own credit report is not an inquiry about new credit, so it has no effect on your score.

Lenders use FICO Scores to help them quickly, consistently and objectively evaluate potential borrower's credit risk. Most lenders in the U.S., including Virginia Credit Union, use FICO® Scores as the industry standard for determining credit worthiness.

No. Your credit score does not go up when a hard inquiry drops off your credit report. Your score will not go down when a hard inquiry drops off, either. Instead, a hard inquiry (or hard credit pull) stops having an impact on your credit score after one year, which is one year before it drops off your credit report.

All new auto or mortgage loan or utility inquiries will show on your credit report; however, only one of the inquiries within a specified window of time will impact your credit score. This exception generally does not apply to other types of loans, such as credit cards.

According to FICO, a hard inquiry from a lender will decrease your credit score five points or less. If you have a strong credit history and no other credit issues, you may find that your scores drop even less than that.

No, requesting your credit report will not hurt your credit score. Checking your own credit report is not an inquiry about new credit, so it has no effect on your score.

According to FICO, a hard inquiry from a lender will decrease your credit score five points or less. If you have a strong credit history and no other credit issues, you may find that your scores drop even less than that. The drop is temporary.

Though prospective employers don't see your credit score in a credit check, they do see your open lines of credit (such as mortgages), outstanding balances, auto or student loans, foreclosures, late or missed payments, any bankruptcies and collection accounts.

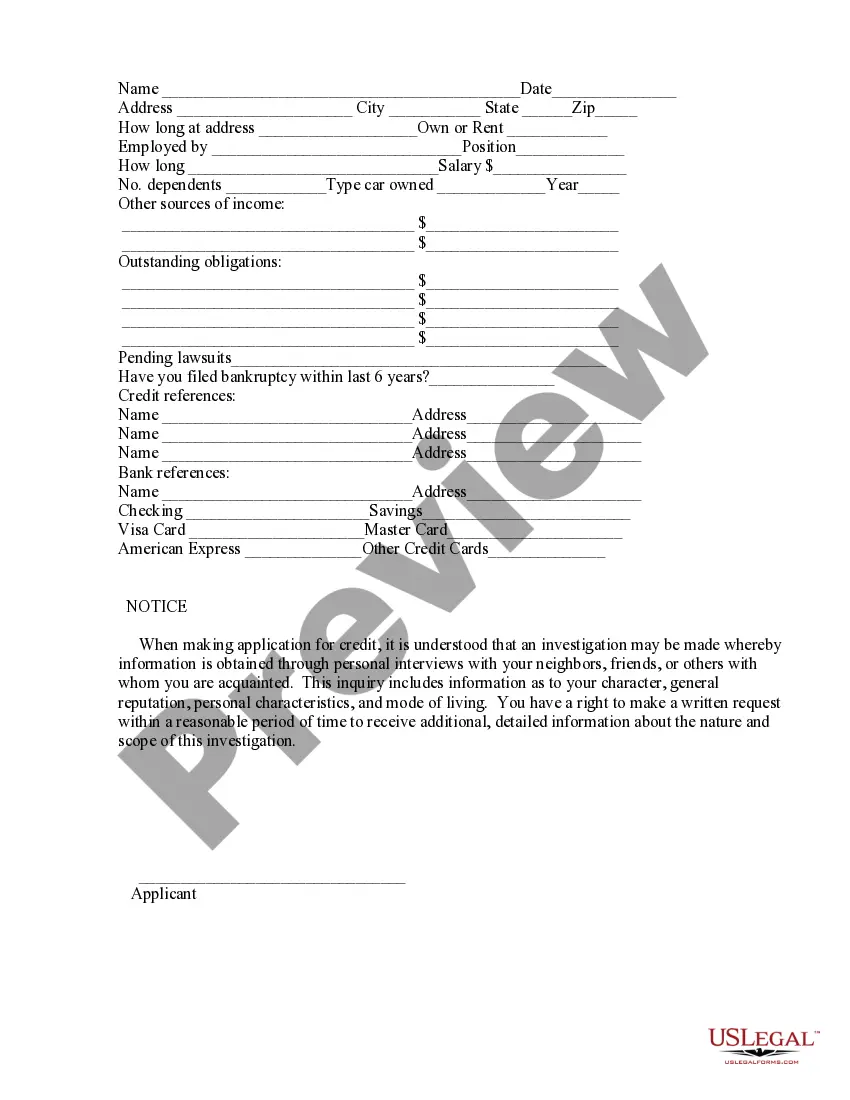

This information is reported to Equifax by your lenders and creditors and includes the types of accounts (for example, a credit card, mortgage, student loan, or vehicle loan), the date those accounts were opened, your credit limit or loan amount, account balances, and your payment history.