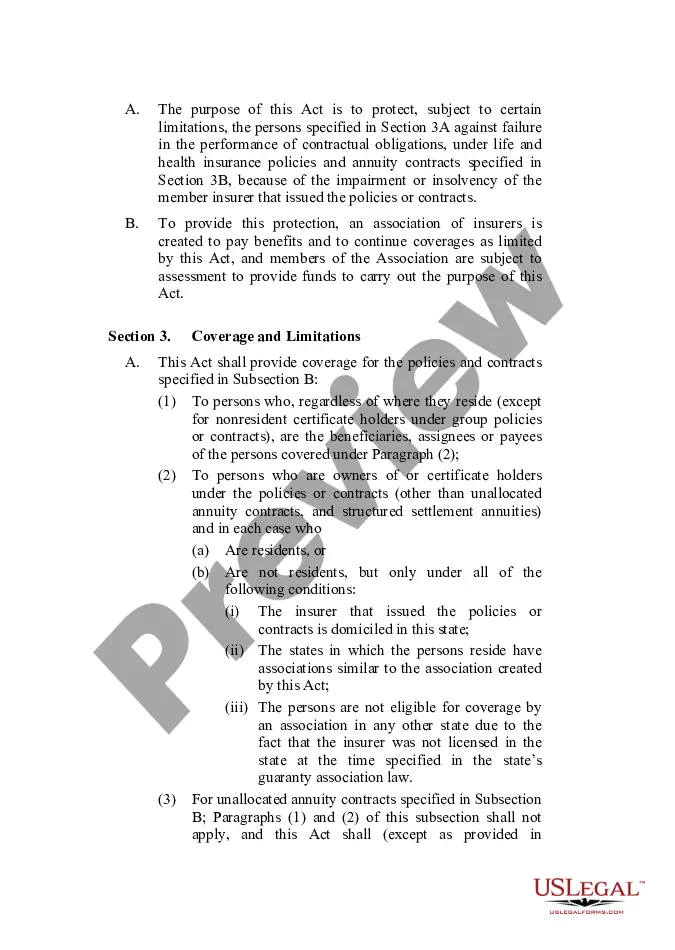

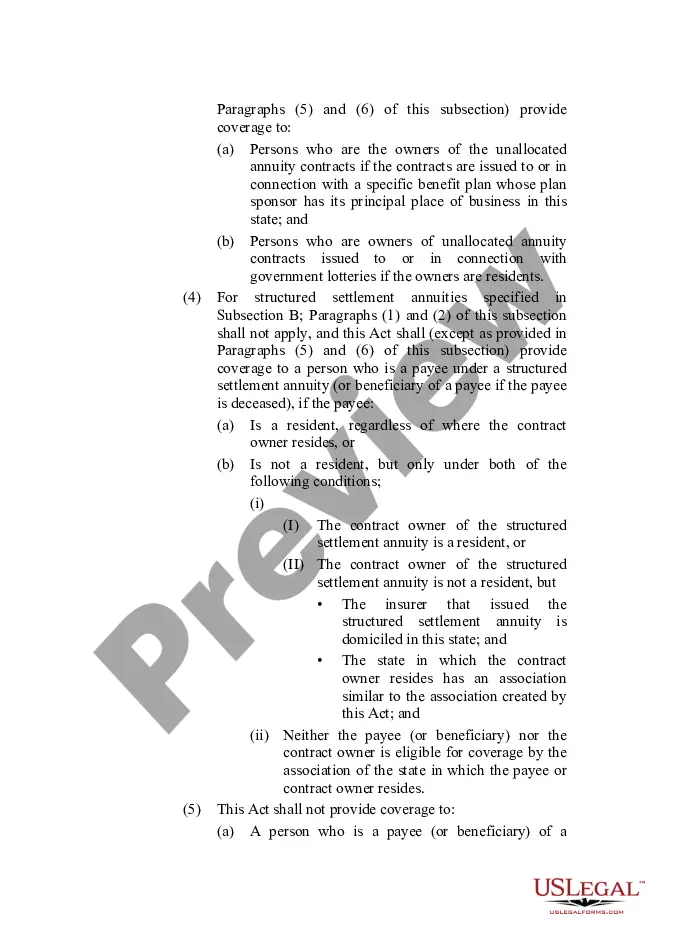

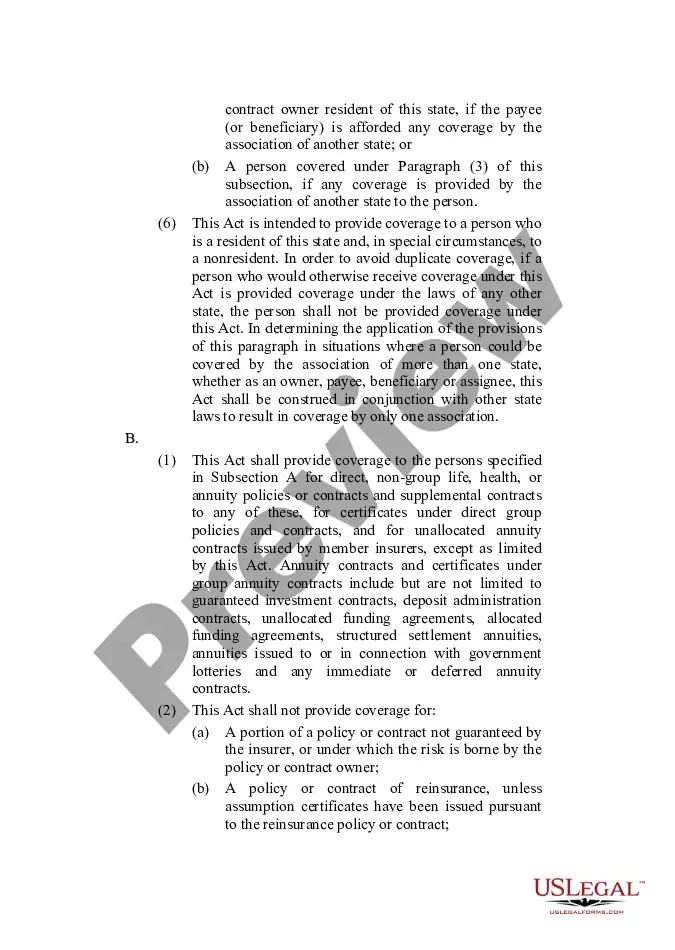

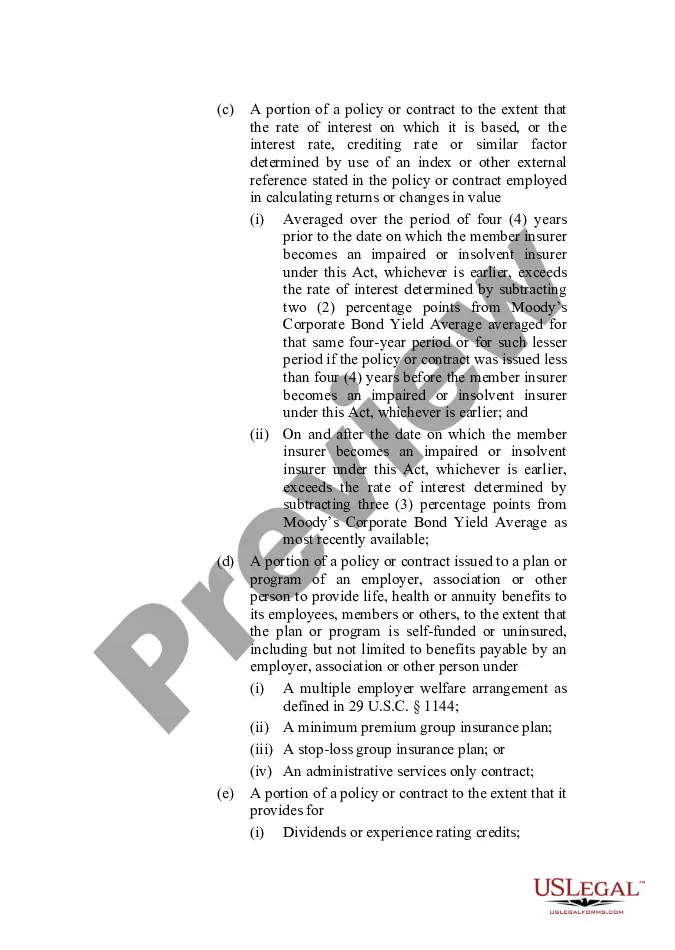

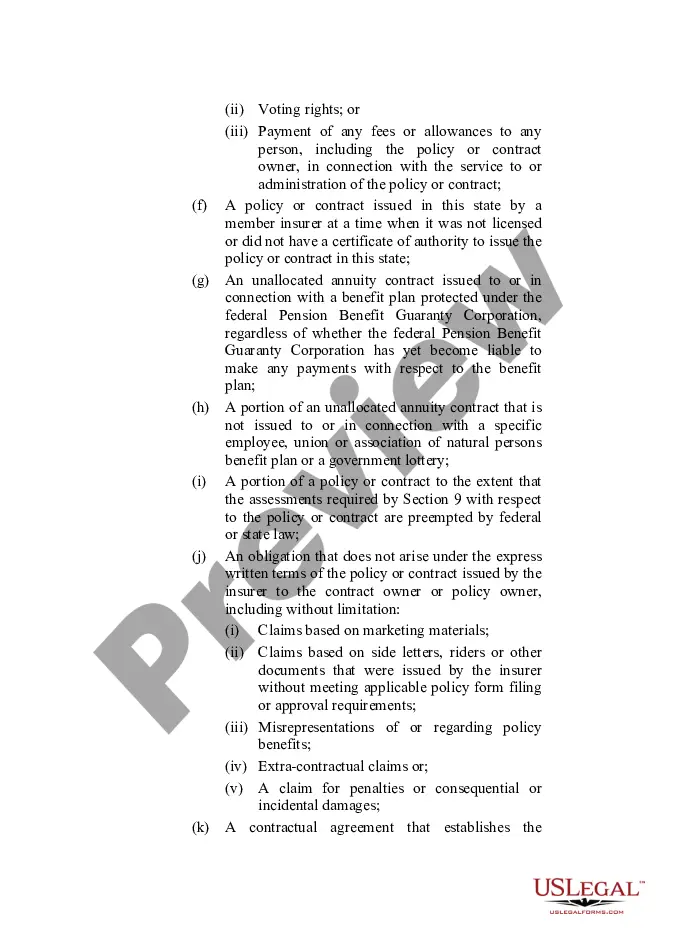

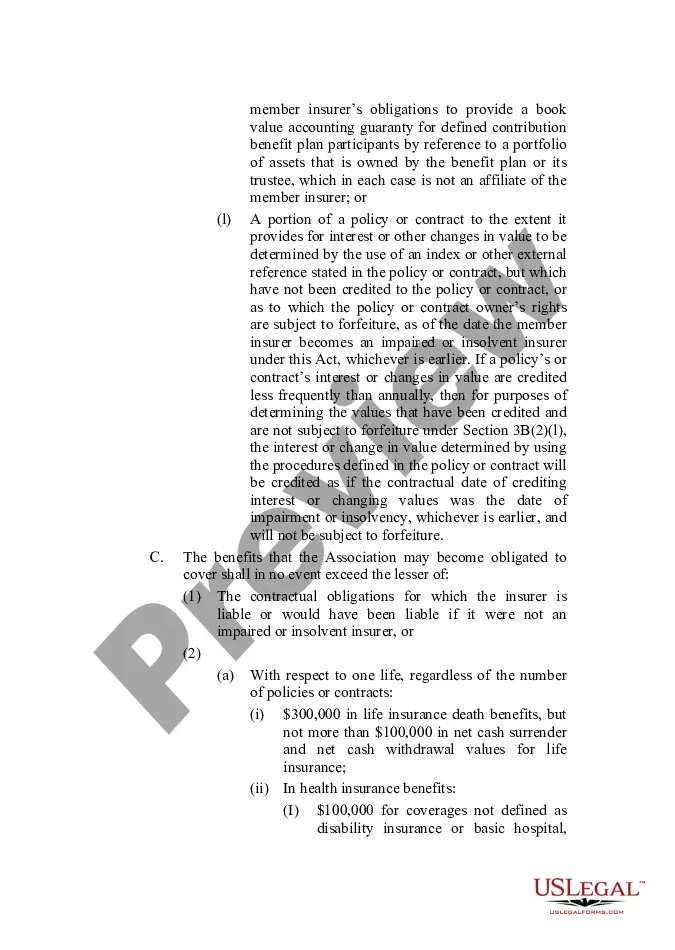

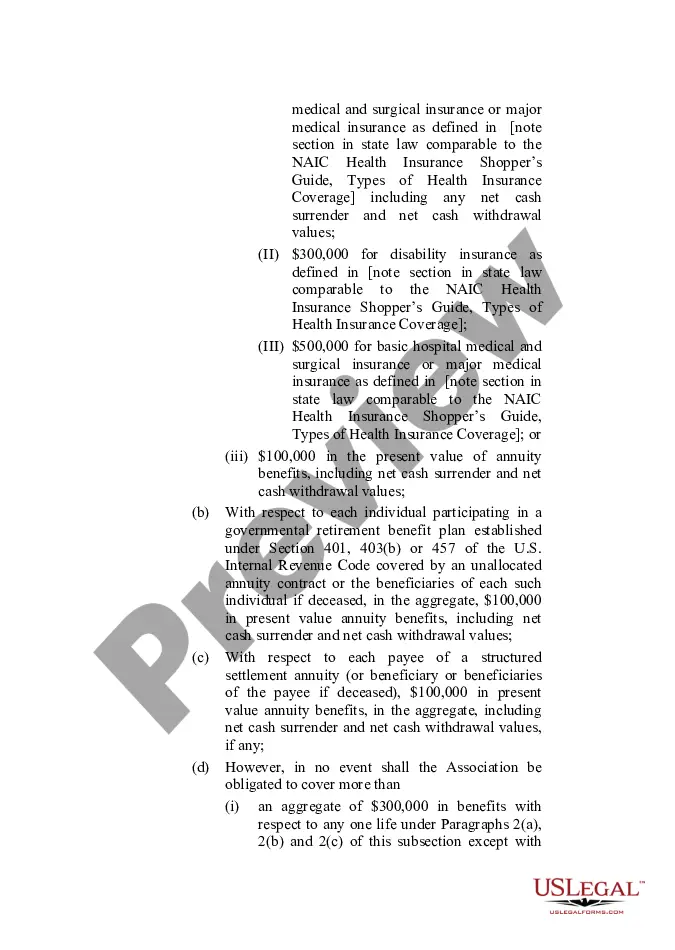

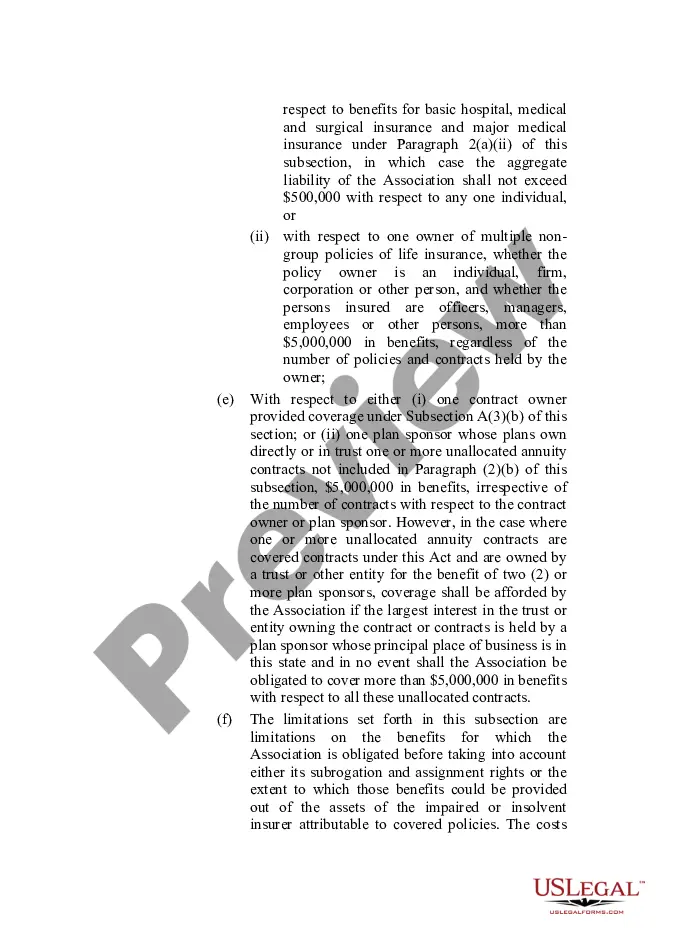

Full text and statutory guidelines for the Life and Health Insurance Guaranty Association Model Act.

The Virginia Life and Health Insurance Guaranty Association Model Act is a legislative framework designed to protect policyholders in the event of an insurance company's insolvency. This model act serves as a blueprint for state insurance guaranty associations to ensure that consumers are safeguarded when an insurance provider is unable to fulfill its obligations. The main purpose of this model act is to establish a Virginia Life and Health Insurance Guaranty Association (HIGH), which is a nonprofit organization formed by insurance companies licensed to conduct business within the state. The HIGH acts as a safety net, providing protection and assistance to policyholders who may face financial loss due to an insolvent insurer. Under the Virginia Life and Health Insurance Guaranty Association Model Act, policyholders are assured a certain level of protection. If an insurance company becomes insolvent and is unable to meet its claims obligations, the HIGH steps in to help fulfill these obligations, up to certain limits defined by the act. There are various provisions and guidelines outlined in this model act to ensure smooth operations and fair treatment for policyholders. The act covers both life and health insurance policies, safeguarding individuals who have invested in these types of coverage. Some key features of the Virginia Life and Health Insurance Guaranty Association Model Act include: 1. Coverage Limits: The act defines certain limits on the amount of coverage provided by the HIGH. Typically, the coverage amount is capped per individual policy or contract, ensuring a reasonable level of protection without creating an excessive burden on the guaranty association. 2. Claims Process: The model act lays down detailed procedures for policyholders to file claims with the HIGH. It defines the timeframes within which claims must be made and processed, ensuring efficient and fair resolution of policyholder claims. 3. Assessments: The act also addresses funding arrangements for the HIGH. Insurance companies licensed in Virginia are typically required to contribute financially to the association's capital base to ensure it has sufficient funds to meet its obligations. Assessments are generally based on the insurance company's premium writings or other appropriate criteria. 4. Rehabilitation and Liquidation: The model act outlines the role of the HIGH in the rehabilitation or liquidation of insolvent insurers. It ensures that policyholders' rights are protected throughout the process and that the association actively participates to protect their interests. It's worth mentioning that while this description primarily focuses on the Virginia Life and Health Insurance Guaranty Association Model Act, there may be variations or amendments specific to Virginia state law. Furthermore, it is essential to refer to the official legislative text or consult legal experts for precise details on the Virginia-specific versions of this act.The Virginia Life and Health Insurance Guaranty Association Model Act is a legislative framework designed to protect policyholders in the event of an insurance company's insolvency. This model act serves as a blueprint for state insurance guaranty associations to ensure that consumers are safeguarded when an insurance provider is unable to fulfill its obligations. The main purpose of this model act is to establish a Virginia Life and Health Insurance Guaranty Association (HIGH), which is a nonprofit organization formed by insurance companies licensed to conduct business within the state. The HIGH acts as a safety net, providing protection and assistance to policyholders who may face financial loss due to an insolvent insurer. Under the Virginia Life and Health Insurance Guaranty Association Model Act, policyholders are assured a certain level of protection. If an insurance company becomes insolvent and is unable to meet its claims obligations, the HIGH steps in to help fulfill these obligations, up to certain limits defined by the act. There are various provisions and guidelines outlined in this model act to ensure smooth operations and fair treatment for policyholders. The act covers both life and health insurance policies, safeguarding individuals who have invested in these types of coverage. Some key features of the Virginia Life and Health Insurance Guaranty Association Model Act include: 1. Coverage Limits: The act defines certain limits on the amount of coverage provided by the HIGH. Typically, the coverage amount is capped per individual policy or contract, ensuring a reasonable level of protection without creating an excessive burden on the guaranty association. 2. Claims Process: The model act lays down detailed procedures for policyholders to file claims with the HIGH. It defines the timeframes within which claims must be made and processed, ensuring efficient and fair resolution of policyholder claims. 3. Assessments: The act also addresses funding arrangements for the HIGH. Insurance companies licensed in Virginia are typically required to contribute financially to the association's capital base to ensure it has sufficient funds to meet its obligations. Assessments are generally based on the insurance company's premium writings or other appropriate criteria. 4. Rehabilitation and Liquidation: The model act outlines the role of the HIGH in the rehabilitation or liquidation of insolvent insurers. It ensures that policyholders' rights are protected throughout the process and that the association actively participates to protect their interests. It's worth mentioning that while this description primarily focuses on the Virginia Life and Health Insurance Guaranty Association Model Act, there may be variations or amendments specific to Virginia state law. Furthermore, it is essential to refer to the official legislative text or consult legal experts for precise details on the Virginia-specific versions of this act.