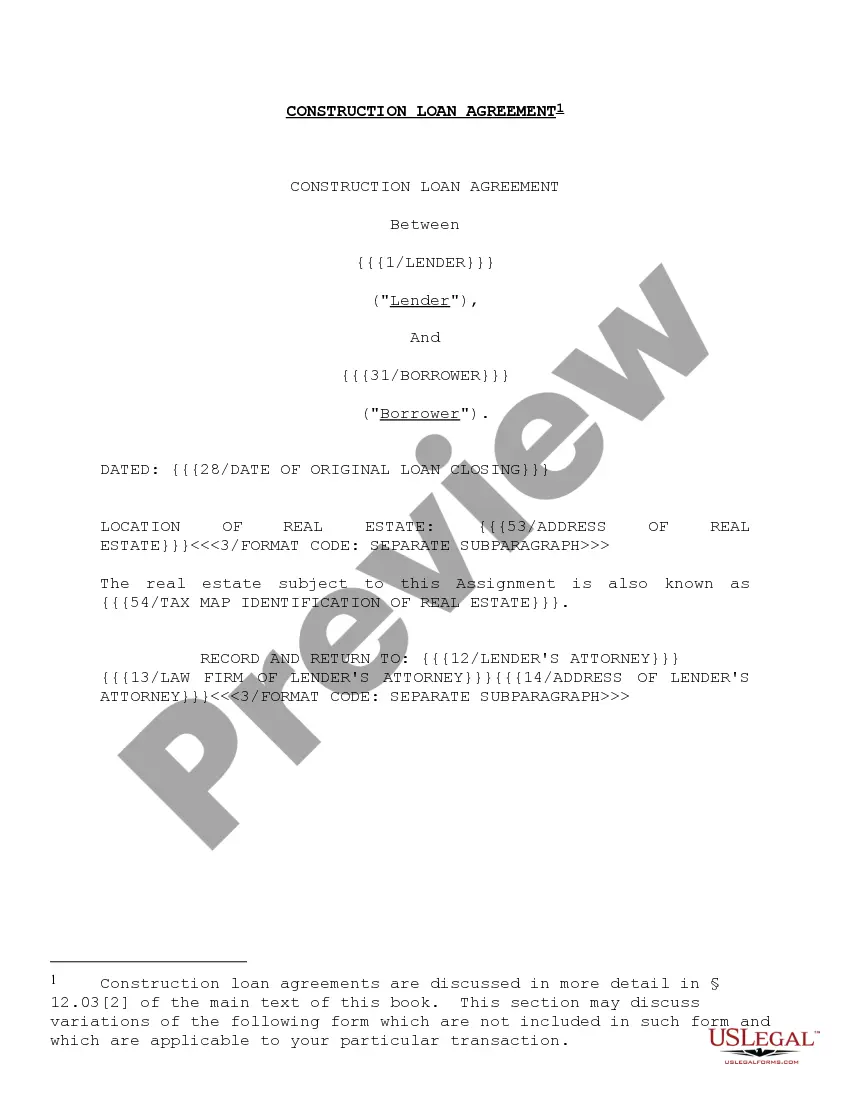

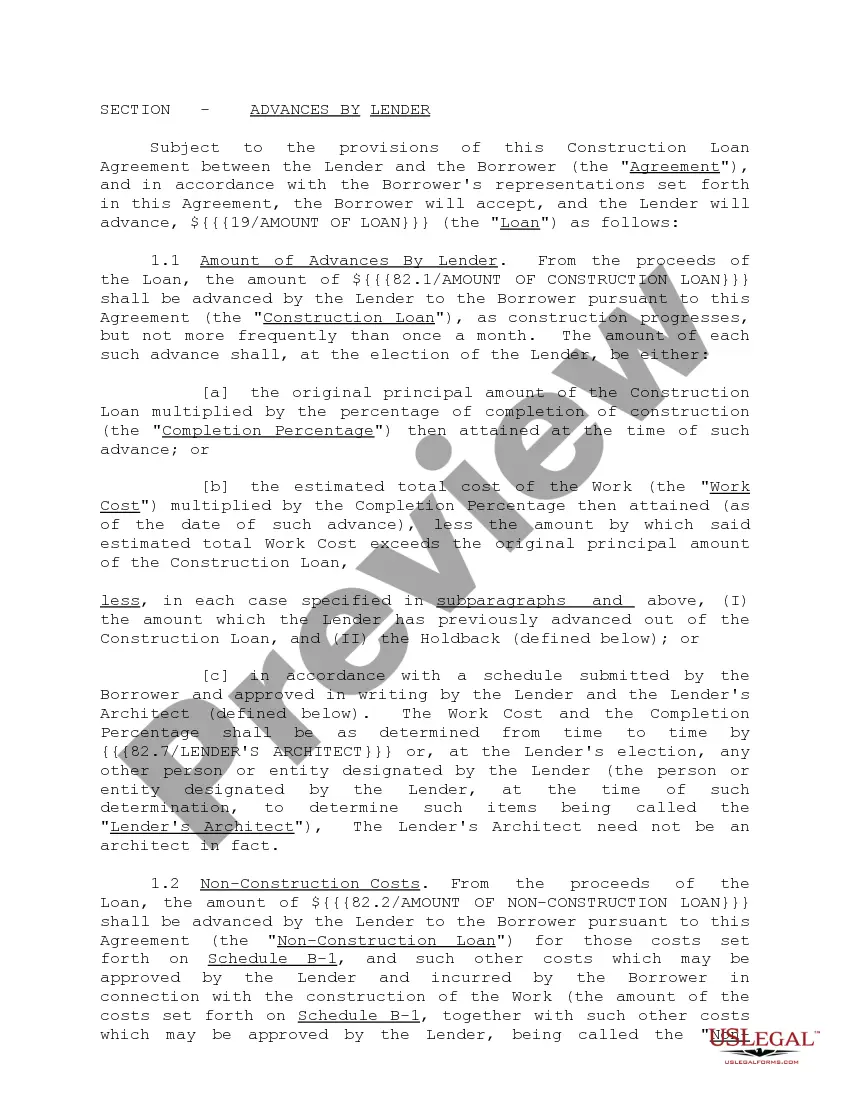

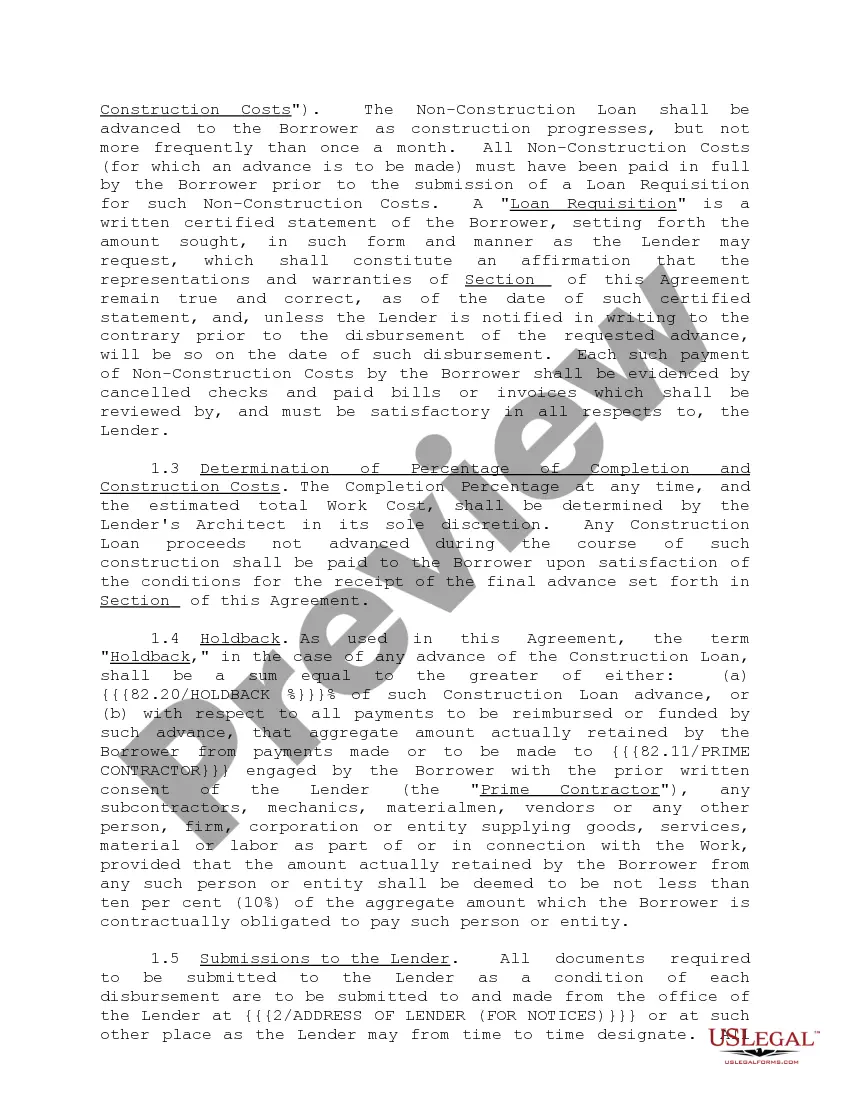

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Virginia Construction Loan Agreements and Variations: An Overview In the realm of real estate and property development, construction loan agreements play a pivotal role. These agreements provide essential financial assistance to individuals and businesses aiming to undertake construction projects in Virginia. A construction loan agreement, simply put, is a legally binding contract that outlines the terms and conditions of a loan provided to finance the costs associated with constructing a building or improving an existing property. Virginia, being a thriving hub of construction activity, offers various types of construction loan agreements and variations to cater to the diverse needs of borrowers. Here, we explore a few prominent types of Virginia construction loan agreements: 1. Traditional Construction Loan Agreement: This type of construction loan agreement in Virginia is designed for those seeking to build a new property from scratch. It typically involves a lender providing funds to the borrower in installments, known as "draws," at various stages of construction. These draws allow the borrower to pay for labor, materials, and other project-related costs as they progress. 2. Renovation or Remodeling Construction Loan Agreement: For individuals and businesses looking to renovate or remodel an existing property in Virginia, this type of construction loan agreement is suitable. It provides funding for repairs, renovations, or upgrades to enhance the value and functionality of the property. The loan amount may be based on the appraised value of the property after the improvements. 3. Construction-to-Permanent Loan Agreement: Often known as a "one-time-close" loan, this agreement combines the financing for construction and the long-term mortgage into a single package. It enables borrowers to transition smoothly from the construction phase to permanent financing without the need for a separate loan agreement. This type of loan is advantageous as it minimizes paperwork and ensures a seamless borrowing process. 4. Builder or Spec Home Construction Loan Agreement: Designed for experienced builders or developers, this type of construction loan agreement facilitates the construction of multiple homes or speculative projects. Builders can obtain upfront financing for land acquisition, labor, and construction costs. Upon completion, these homes can then be sold to potential buyers, enabling the builder to repay the loan. 5. Bridge Construction Loan Agreement: In instances where a borrower needs short-term financing to bridge the gap between the construction phase and the eventual sale or refinance of the property, a bridge construction loan agreement is ideal. It provides funding until the project is complete or a long-term loan can be secured. These short-term loans help alleviate financial burdens during the interim period. Overall, Virginia construction loan agreements and their variations offer a flexible approach to financing construction projects. Each type serves a different purpose, catering to the unique requirements and objectives of borrowers. It is crucial for potential borrowers to carefully consider their needs and consult with experienced professionals to select the most suitable construction loan agreement in Virginia.Virginia Construction Loan Agreements and Variations: An Overview In the realm of real estate and property development, construction loan agreements play a pivotal role. These agreements provide essential financial assistance to individuals and businesses aiming to undertake construction projects in Virginia. A construction loan agreement, simply put, is a legally binding contract that outlines the terms and conditions of a loan provided to finance the costs associated with constructing a building or improving an existing property. Virginia, being a thriving hub of construction activity, offers various types of construction loan agreements and variations to cater to the diverse needs of borrowers. Here, we explore a few prominent types of Virginia construction loan agreements: 1. Traditional Construction Loan Agreement: This type of construction loan agreement in Virginia is designed for those seeking to build a new property from scratch. It typically involves a lender providing funds to the borrower in installments, known as "draws," at various stages of construction. These draws allow the borrower to pay for labor, materials, and other project-related costs as they progress. 2. Renovation or Remodeling Construction Loan Agreement: For individuals and businesses looking to renovate or remodel an existing property in Virginia, this type of construction loan agreement is suitable. It provides funding for repairs, renovations, or upgrades to enhance the value and functionality of the property. The loan amount may be based on the appraised value of the property after the improvements. 3. Construction-to-Permanent Loan Agreement: Often known as a "one-time-close" loan, this agreement combines the financing for construction and the long-term mortgage into a single package. It enables borrowers to transition smoothly from the construction phase to permanent financing without the need for a separate loan agreement. This type of loan is advantageous as it minimizes paperwork and ensures a seamless borrowing process. 4. Builder or Spec Home Construction Loan Agreement: Designed for experienced builders or developers, this type of construction loan agreement facilitates the construction of multiple homes or speculative projects. Builders can obtain upfront financing for land acquisition, labor, and construction costs. Upon completion, these homes can then be sold to potential buyers, enabling the builder to repay the loan. 5. Bridge Construction Loan Agreement: In instances where a borrower needs short-term financing to bridge the gap between the construction phase and the eventual sale or refinance of the property, a bridge construction loan agreement is ideal. It provides funding until the project is complete or a long-term loan can be secured. These short-term loans help alleviate financial burdens during the interim period. Overall, Virginia construction loan agreements and their variations offer a flexible approach to financing construction projects. Each type serves a different purpose, catering to the unique requirements and objectives of borrowers. It is crucial for potential borrowers to carefully consider their needs and consult with experienced professionals to select the most suitable construction loan agreement in Virginia.