Virginia Construction Loan Financing Term Sheet

Description

How to fill out Construction Loan Financing Term Sheet?

You can commit hrs on-line searching for the legal file format that meets the state and federal requirements you want. US Legal Forms provides 1000s of legal types which can be reviewed by specialists. You can easily down load or print out the Virginia Construction Loan Financing Term Sheet from my assistance.

If you already possess a US Legal Forms accounts, you are able to log in and then click the Download option. Afterward, you are able to complete, edit, print out, or signal the Virginia Construction Loan Financing Term Sheet. Each and every legal file format you get is your own permanently. To get one more copy for any bought develop, visit the My Forms tab and then click the related option.

Should you use the US Legal Forms internet site for the first time, follow the simple guidelines under:

- Initial, be sure that you have selected the correct file format for the region/city of your liking. See the develop information to make sure you have picked out the right develop. If readily available, take advantage of the Preview option to appear through the file format as well.

- If you would like discover one more edition from the develop, take advantage of the Lookup industry to discover the format that meets your requirements and requirements.

- After you have identified the format you would like, click on Get now to proceed.

- Choose the costs plan you would like, enter your accreditations, and register for a merchant account on US Legal Forms.

- Complete the financial transaction. You may use your Visa or Mastercard or PayPal accounts to pay for the legal develop.

- Choose the file format from the file and down load it to the gadget.

- Make alterations to the file if possible. You can complete, edit and signal and print out Virginia Construction Loan Financing Term Sheet.

Download and print out 1000s of file web templates making use of the US Legal Forms web site, which provides the greatest selection of legal types. Use expert and condition-particular web templates to tackle your company or person demands.

Form popularity

FAQ

Loans Not Covered by TRID Home-equity lines of credit. Reverse mortgages. Mortgages secured by a mobile home or dwelling not attached to land. No-interest second mortgage made for down payment assistance, energy efficiency or foreclosure avoidance. Loans made by a creditor who makes five or fewer mortgages in a year.

Even if the collateral is commercial real property, if primarily consumer purpose, TRID applies. For a TRID loan, property is the address of the property securing the loan, not purchased (if different).

The TRID rule requires lenders to provide two disclosure documents to lenders: a loan estimate and a closing disclosure. Because each document must be timed to give the borrower three days to look it over, it's sometimes referred to as the ?three-day rule.?

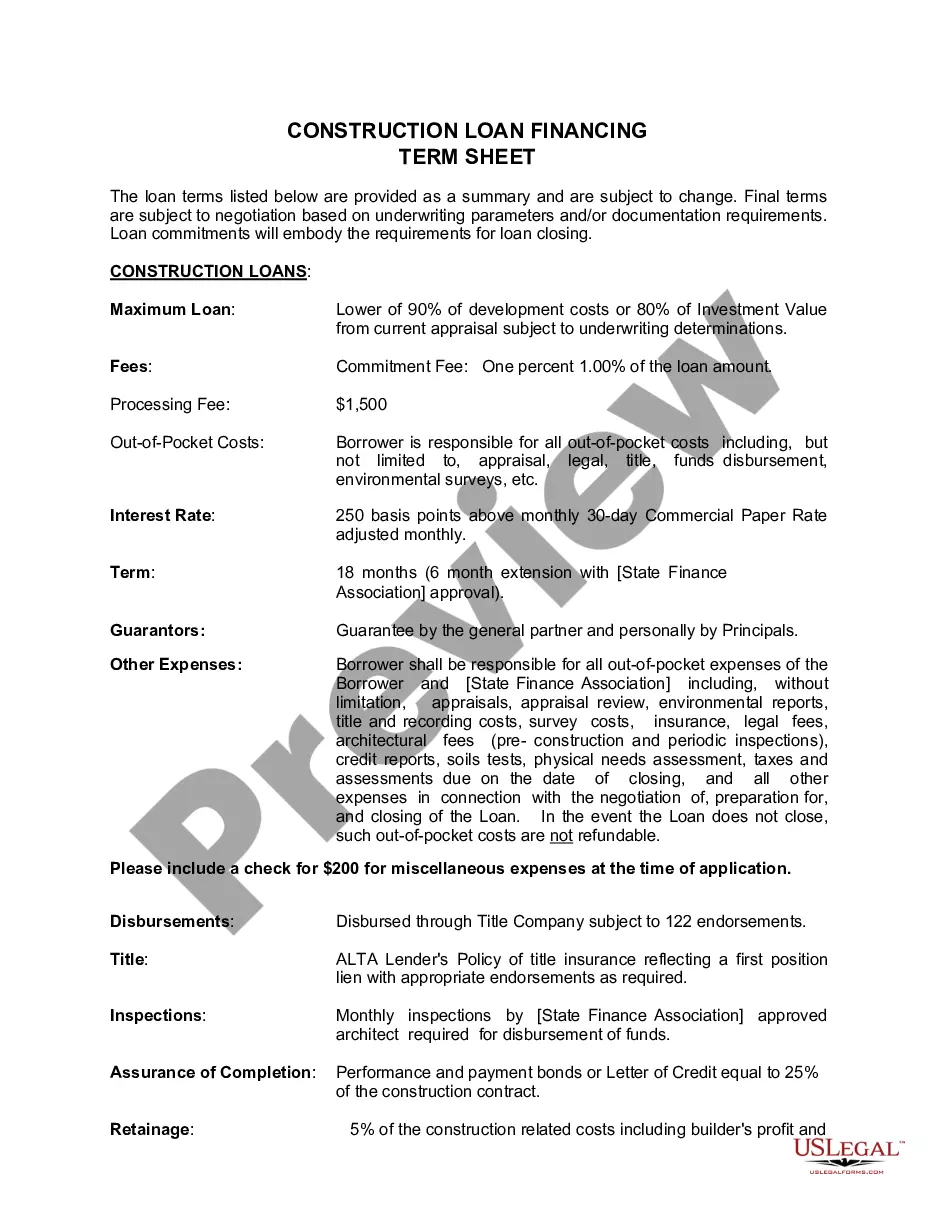

So, for instance, if the home is appraised to be worth $500,000, they will loan you $500,000 x (95% as an example) = $475,000. The down payment will be your construction costs less the loan amount. So, if the construction is quoted to cost $500,000, your down payment will be $500,000 - $475,000 = $25,000.

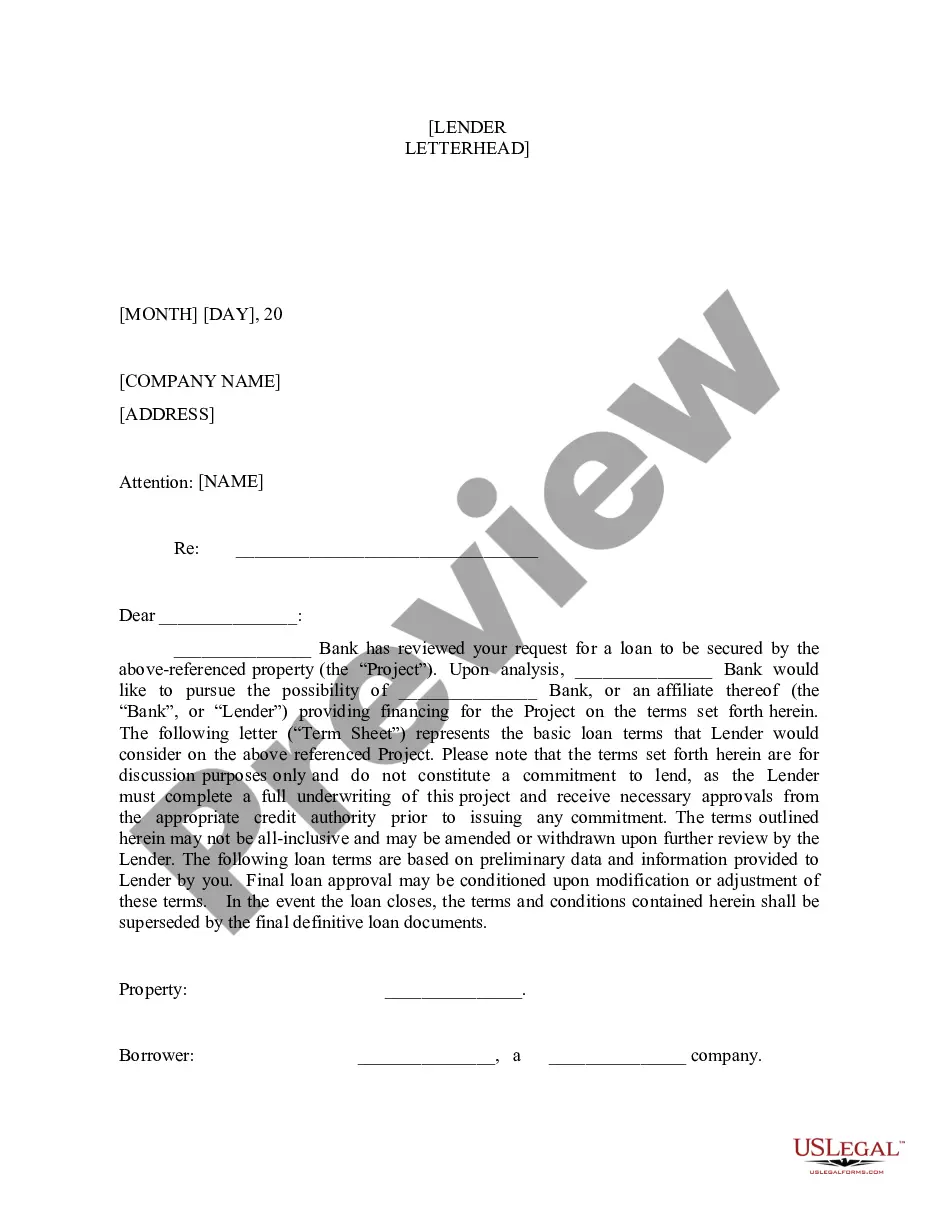

7. Using the concepts discussed above, a creditor can apply the TRI Rule to construction and constructionpermanent loans. The Loan Terms Table includes information about the Loan Amount, Interest Rate, Periodic Principal & Interest Payment, Prepayment Penalty, and Balloon Payment. 12 CFR § 1026.37(b).

Economic details. This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.