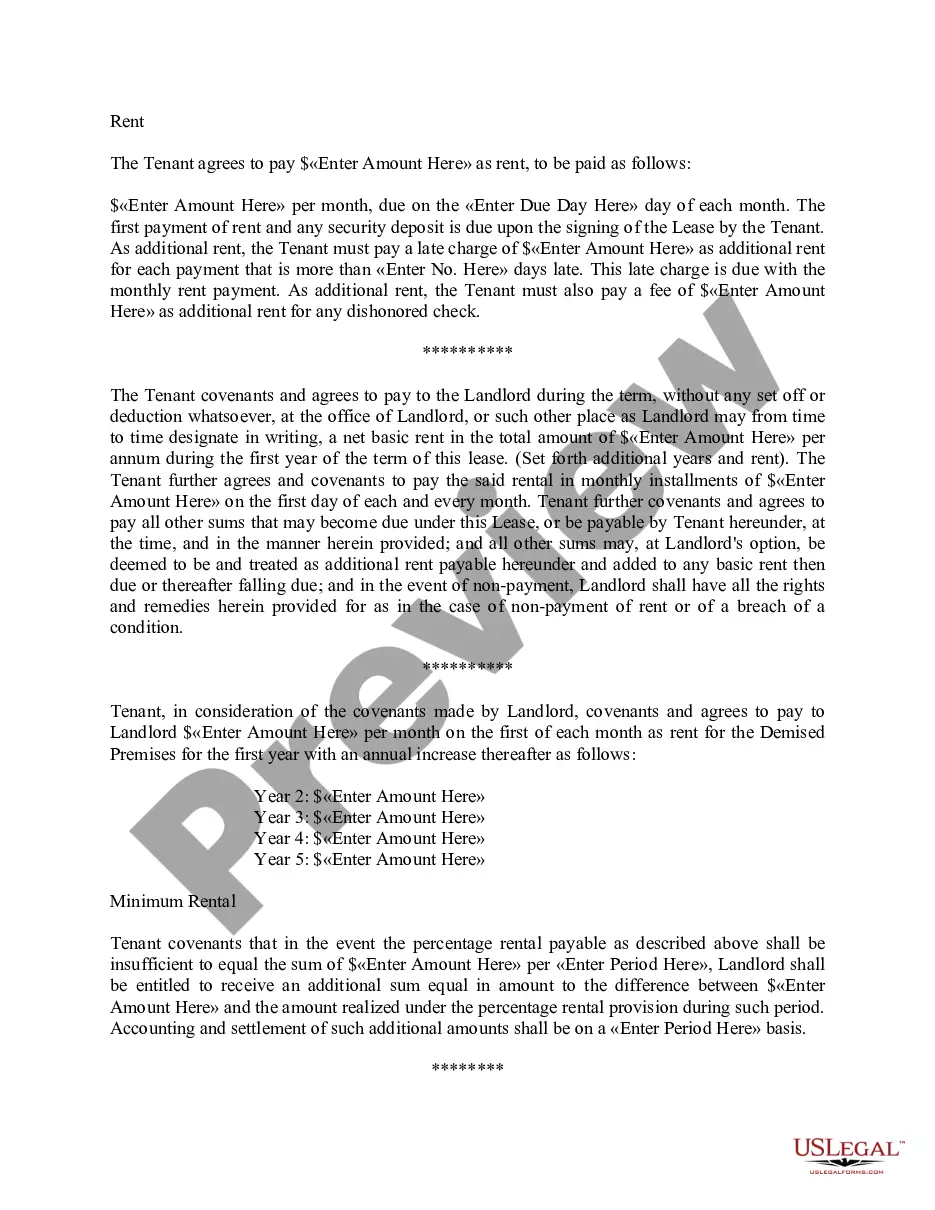

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

Virginia Construction Loan Agreement

Category:

State:

Multi-State

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Construction Loan Agreement?

Choosing the right lawful record web template can be quite a have difficulties. Of course, there are tons of layouts accessible on the Internet, but how will you find the lawful develop you require? Make use of the US Legal Forms internet site. The support delivers thousands of layouts, for example the Virginia Construction Loan Agreement, which can be used for company and private requires. All the varieties are examined by pros and satisfy federal and state needs.

Should you be already registered, log in to the accounts and then click the Obtain option to obtain the Virginia Construction Loan Agreement. Utilize your accounts to appear with the lawful varieties you possess purchased previously. Proceed to the My Forms tab of your own accounts and acquire an additional backup from the record you require.

Should you be a new customer of US Legal Forms, allow me to share straightforward guidelines that you can stick to:

- First, ensure you have selected the appropriate develop for the city/region. You can look over the form making use of the Review option and read the form information to ensure this is the right one for you.

- In case the develop is not going to satisfy your expectations, utilize the Seach area to discover the right develop.

- Once you are positive that the form is acceptable, click on the Buy now option to obtain the develop.

- Select the prices prepare you would like and enter in the essential details. Design your accounts and buy an order using your PayPal accounts or bank card.

- Pick the data file formatting and download the lawful record web template to the system.

- Comprehensive, edit and print out and sign the attained Virginia Construction Loan Agreement.

US Legal Forms is the most significant library of lawful varieties for which you can discover various record layouts. Make use of the service to download expertly-produced documents that stick to condition needs.

Form popularity

FAQ

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

A construction loan agreement is a legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

For loans by a commercial lender, the lender will provide the agreement. But for loans between friends or relatives, you will need to create your own loan agreement.

How to make a family loan agreement The amount borrowed and how it will be used. Repayment terms, including payment amounts, frequency and when the loan will be repaid in full. The loan's interest rate. ... If the loan can be repaid early without penalty, and how much interest will be saved by early repayment.

The VA program does not allow for owner/builders. While the VA only requires that the builder be registered to participate in the program, each lender can require the builder to go through an approval process. The borrower and the builder must submit a complete set of plans and specs for the home when applying.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

What a personal loan agreement should include Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided. Repayment date. Interest rate to be charged (if applicable). Annual percentage rate (if applicable).