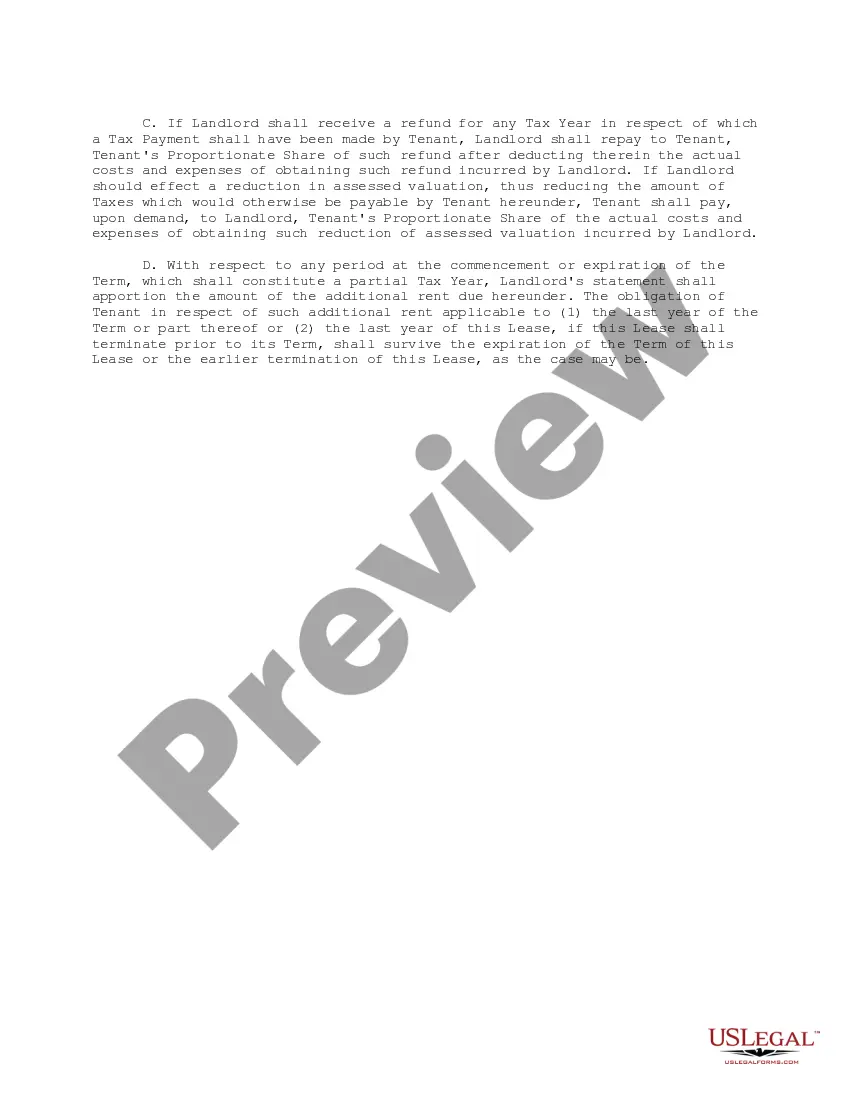

This form is a clause regarding additional rent element of an office lease providing for tax increases. The tax increases pertain to assessments and special assessments levied, assessed or imposed upon the building and/or the land under, including any land(s) dedicated to the use of, the building, by any governmental bodies or authorities.

The Virginia Tax Increase Clause, also known as the Tax-Increase Limitation, is a provision in the Virginia Constitution that serves as a constraint on the state's ability to raise taxes without explicit approval from the voters. This clause ensures that any proposed tax increase is subject to strict scrutiny and requires a super majority vote for approval by the General Assembly. The purpose of the Tax Increase Clause is to protect taxpayers by imposing a significant hurdle for the government to raise taxes. It reflects the belief that taxation should not be increased without a broad consensus from the public and helps maintain fiscal discipline in the state's budgetary process. There are two main types of the Virginia Tax Increase Clause: 1. General Tax Increase Clause: This clause governs all taxes proposed in Virginia and applies universally across various types of taxes. It imposes a requirement that any proposed tax increase, regardless of the specific type of tax, must be approved by a super majority vote (two-thirds) in both the Virginia House of Delegates and the Virginia Senate. 2. Transportation Tax Increase Clause: In addition to the general Tax Increase Clause, Virginia has a separate clause dedicated to transportation taxes. This clause mandates that any proposed increase in transportation-related taxes must be approved by a majority vote in a general referendum. This ensures that decisions related to transportation funding involve direct public input. Overall, the Virginia Tax Increase Clause serves as a safeguard for taxpayers, requiring a higher threshold for tax increases than those required for regular legislation. It ensures that elected officials must closely consider the potential impact on the economy and the public before proposing any tax hikes. This constitutional provision has been instrumental in maintaining a balanced and considerate approach to taxation in the state of Virginia.