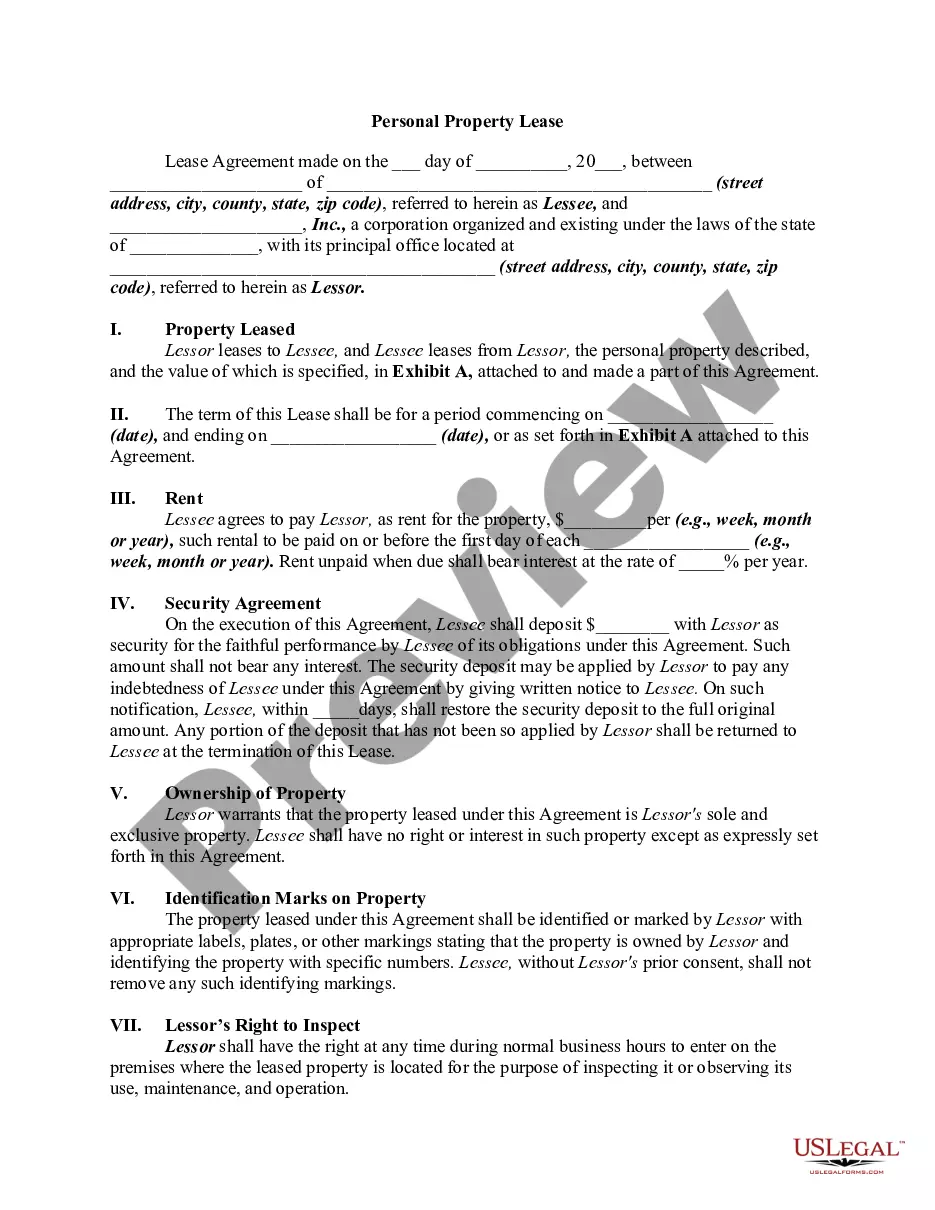

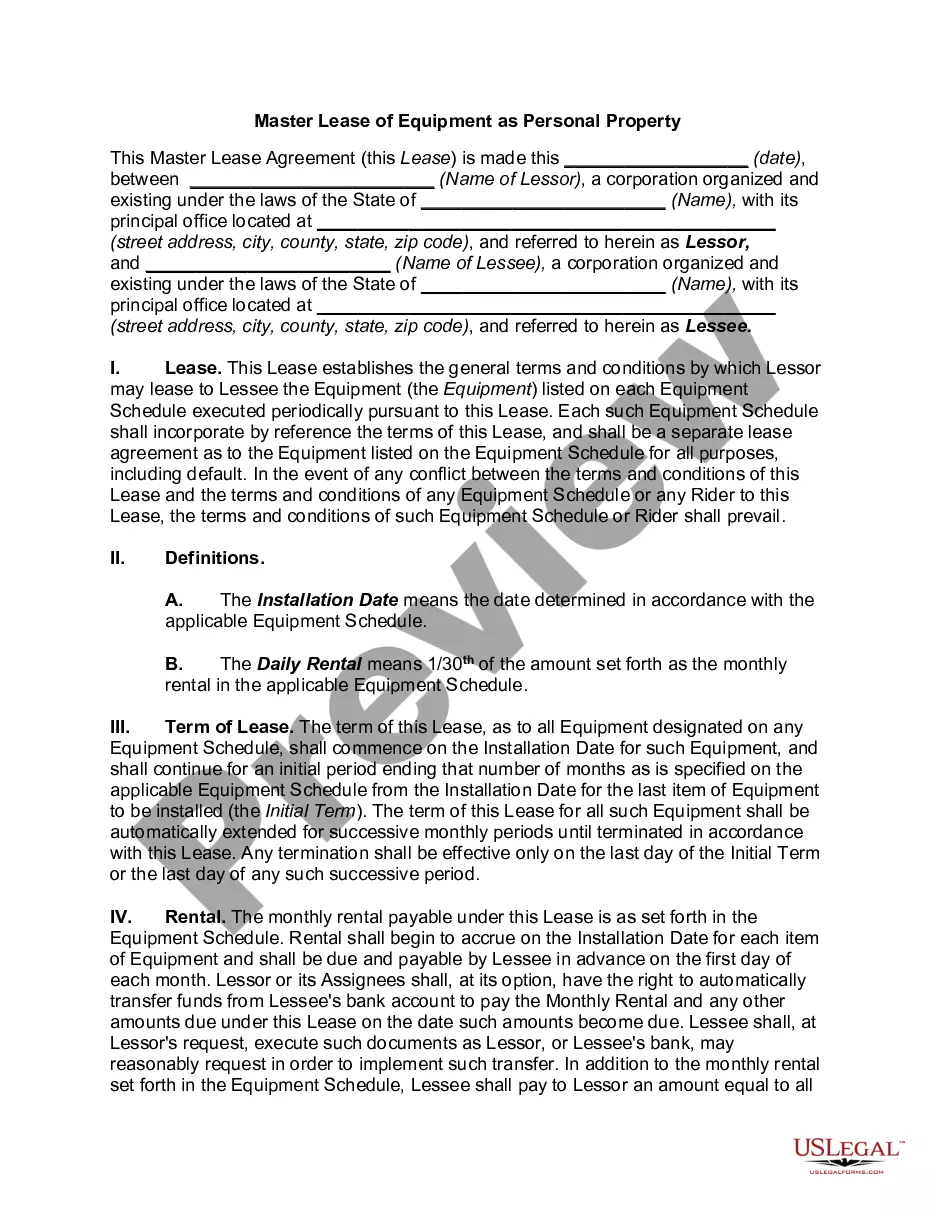

This form is a contract for the lease of personal property. The lessor demises and leases to the lessee and the lessee takes and rents from the lessor certain personal property described in Exhibit "A".

Virgin Islands Contract for the Lease of Personal Property

Instant download

Description

Free preview

How to fill out Contract For The Lease Of Personal Property?

If you want to complete, download, or create lawful document templates, utilize US Legal Forms, the largest assortment of legal forms available online.

Take advantage of the site’s simple and convenient search feature to find the documents you need.

A range of templates for business and personal uses is organized by categories and headings, or keywords.

Step 4. Once you have identified the form you need, click the Get now button. Select the pricing plan that suits you and enter your details to register for an account.

Step 6. Complete the payment process. You can use your credit card or PayPal account to finalize the transaction.

- Utilize US Legal Forms to locate the Virgin Islands Contract for the Lease of Personal Property with just a few clicks.

- If you are already a US Legal Forms subscriber, Log In to your account and click the Download button to acquire the Virgin Islands Contract for the Lease of Personal Property.

- You can also view forms you previously obtained from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the form for your correct city/state.

- Step 2. Utilize the Preview option to review the form's content. Remember to read the description.

- Step 3. If you are unhappy with the form, use the Search field at the top of the screen to find other variations of the legal document template.