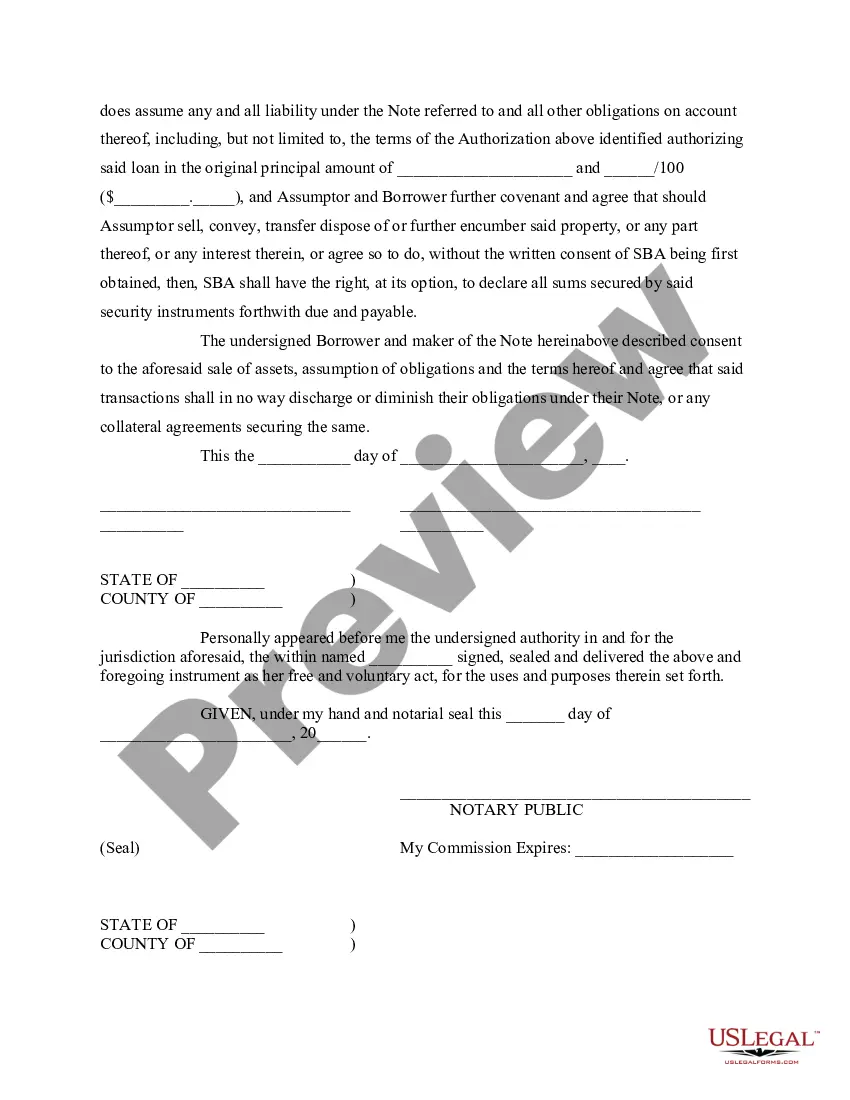

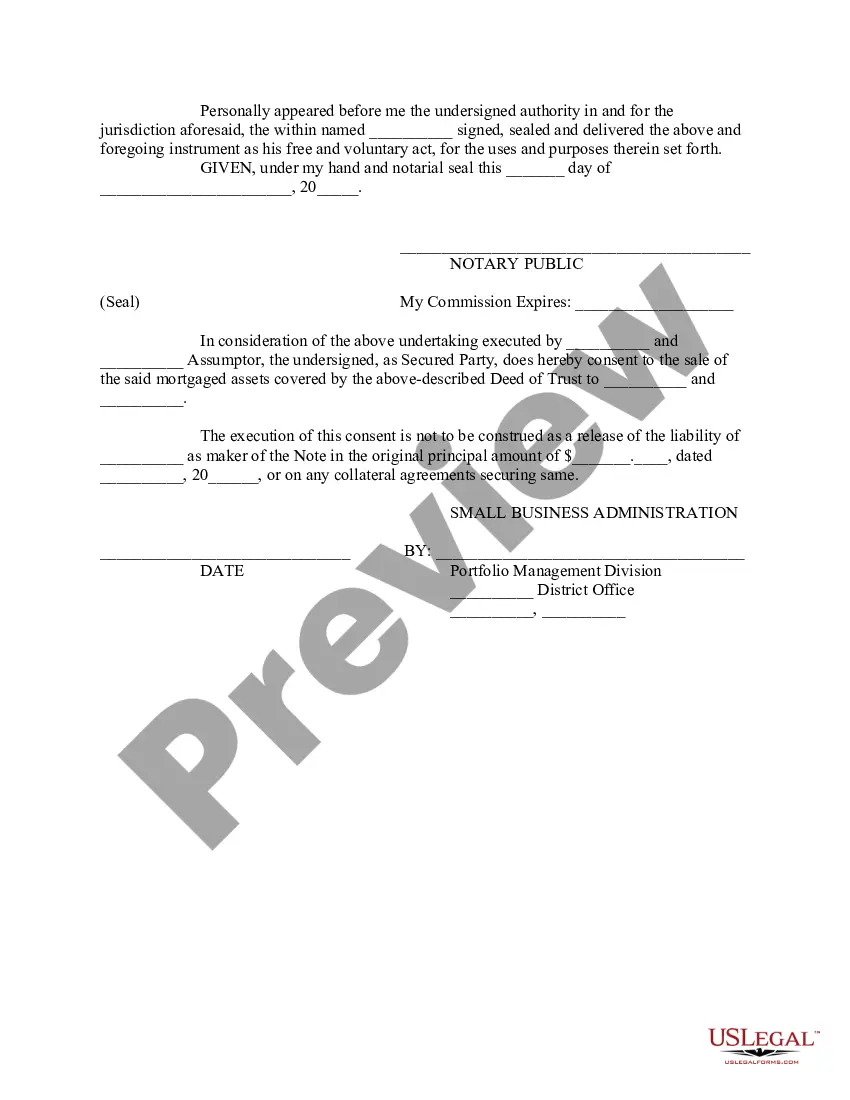

This form is an assumption agreement for a Small Business Administration (SBA) loan. Party assuming the loan agrees to continue payments thereon. SBA agrees to the assumption of the loan and release of original debtor. Adapt to fit your circumstances.

The Virgin Islands Assumption Agreement of Small Business Administration (SBA) Loan refers to a legal document that encompasses the transfer of responsibility for an existing SBA loan from the original borrower (the "assumed") to a new borrower (the "assumed"). This agreement is specifically applicable to the U.S. Virgin Islands, an unincorporated territory of the United States. The purpose of the Virgin Islands Assumption Agreement is to formally recognize the new borrower's assumption of all obligations, liabilities, and responsibilities associated with the SBA loan. This includes the repayment of the outstanding loan balance, adherence to the terms and conditions set forth in the original loan agreement, and compliance with any applicable federal, state, and local laws. The agreement typically incorporates the key terms and provisions of the original SBA loan, including the principal amount, interest rate, repayment schedule, prepayment penalties, and any personal guarantees or collateral involved. Additionally, it outlines the terms specific to the assumption process, such as the effective date of the assumption, the documentation required for approval, and any fees or costs associated with the assumption. In some cases, there may be multiple types or variations of Virgin Islands Assumption Agreements of SBA Loans, depending on specific circumstances or requirements. These can include: 1. Full Assumption: This type of assumption agreement transfers complete responsibility for the SBA loan from the original borrower to the new borrower, including both the loan balance and all associated obligations. 2. Partial Assumption: In certain situations, a partial assumption may be allowed, wherein only a portion of the outstanding SBA loan balance is transferred to the new borrower. This can occur when a primary borrower wishes to reduce their liability, but the lender determines that the new borrower has adequate financial stability to assume a partial responsibility. 3. Assumption with Release: This type of assumption agreement releases the original borrower from all obligations and liabilities associated with the SBA loan upon successful assumption by the new borrower. This can provide added flexibility for the original borrower while allowing the new borrower to assume responsibility for the loan. It is important to note that the specific terms and conditions of the Virgin Islands Assumption Agreement of SBA Loan may be subject to negotiation between the parties involved, including the current borrower, the new borrower, and the SBA lender. Consulting with legal professionals or experienced loan officers is highly recommended ensuring compliance and protect the interests of all parties involved.

The Virgin Islands Assumption Agreement of Small Business Administration (SBA) Loan refers to a legal document that encompasses the transfer of responsibility for an existing SBA loan from the original borrower (the "assumed") to a new borrower (the "assumed"). This agreement is specifically applicable to the U.S. Virgin Islands, an unincorporated territory of the United States. The purpose of the Virgin Islands Assumption Agreement is to formally recognize the new borrower's assumption of all obligations, liabilities, and responsibilities associated with the SBA loan. This includes the repayment of the outstanding loan balance, adherence to the terms and conditions set forth in the original loan agreement, and compliance with any applicable federal, state, and local laws. The agreement typically incorporates the key terms and provisions of the original SBA loan, including the principal amount, interest rate, repayment schedule, prepayment penalties, and any personal guarantees or collateral involved. Additionally, it outlines the terms specific to the assumption process, such as the effective date of the assumption, the documentation required for approval, and any fees or costs associated with the assumption. In some cases, there may be multiple types or variations of Virgin Islands Assumption Agreements of SBA Loans, depending on specific circumstances or requirements. These can include: 1. Full Assumption: This type of assumption agreement transfers complete responsibility for the SBA loan from the original borrower to the new borrower, including both the loan balance and all associated obligations. 2. Partial Assumption: In certain situations, a partial assumption may be allowed, wherein only a portion of the outstanding SBA loan balance is transferred to the new borrower. This can occur when a primary borrower wishes to reduce their liability, but the lender determines that the new borrower has adequate financial stability to assume a partial responsibility. 3. Assumption with Release: This type of assumption agreement releases the original borrower from all obligations and liabilities associated with the SBA loan upon successful assumption by the new borrower. This can provide added flexibility for the original borrower while allowing the new borrower to assume responsibility for the loan. It is important to note that the specific terms and conditions of the Virgin Islands Assumption Agreement of SBA Loan may be subject to negotiation between the parties involved, including the current borrower, the new borrower, and the SBA lender. Consulting with legal professionals or experienced loan officers is highly recommended ensuring compliance and protect the interests of all parties involved.