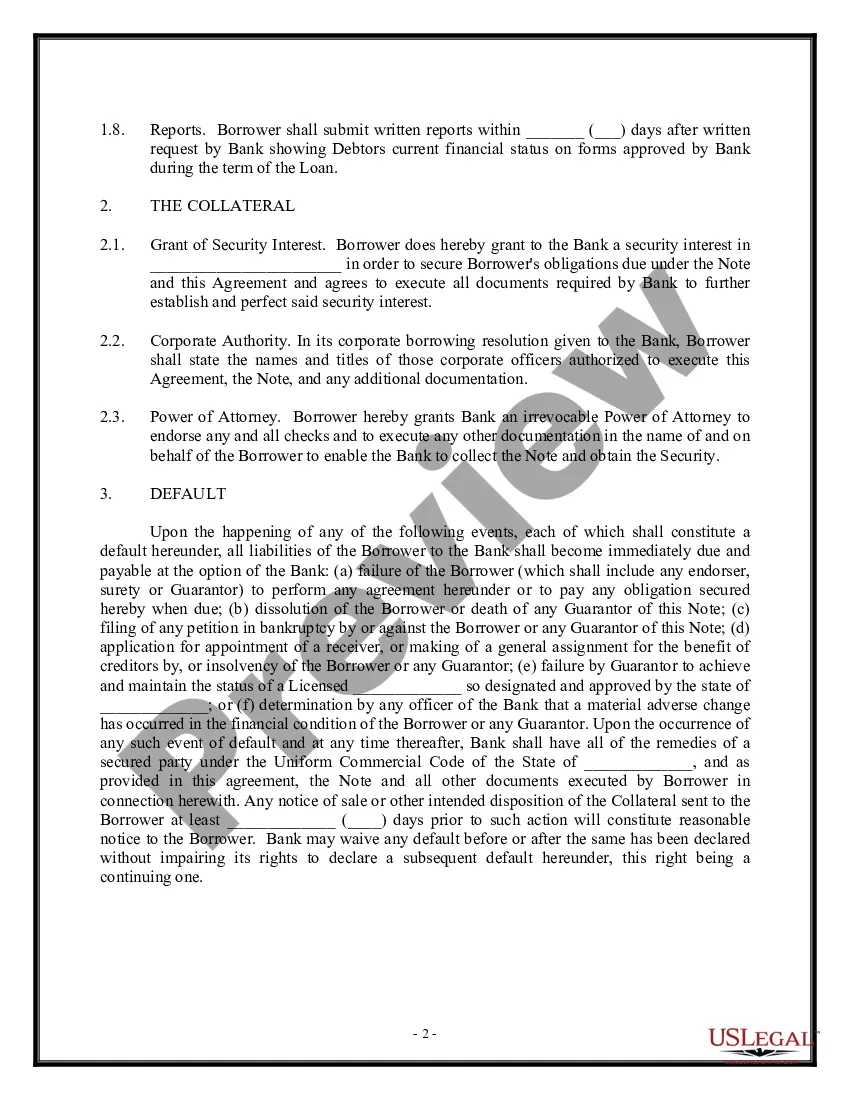

The Virgin Islands Loan Agreement — Short Form is a legally binding document that outlines the terms and conditions of a loan agreement between two parties in the Virgin Islands. This agreement sets out the responsibilities and rights of both the lender and the borrower and is used to ensure clarity and protection for both parties involved in the loan transaction. The Virgin Islands Loan Agreement — Short Form typically includes important details such as the names and contact information of the lender and borrower, the loan amount, the interest rate, repayment terms, late payment penalties, and any other specific terms and conditions agreed upon by both parties. There can be a few different types of Virgin Islands Loan Agreement — Short Form, which may vary based on the purpose of the loan or the relationship between the lender and borrower. Some common types include: 1. Personal Loan Agreement: This type of loan agreement is used when an individual borrows money from another individual or entity for personal use, such as funding education or medical expenses. 2. Business Loan Agreement: This agreement is designed for loans given to businesses, whether it be for startup capital, expansion, or any other purpose related to the business's operations. 3. Real Estate Loan Agreement: This form of loan agreement is specific to loans related to real estate transactions, including mortgages or loans for property purchase, construction, or renovation. 4. Vehicle Loan Agreement: This agreement is used when a loan is given specifically for the purchase of a vehicle, such as a car, motorcycle, or boat. It is important to note that specific loan agreements may include additional clauses or terms depending on the nature of the loan or the requirements of the lender and borrower. Consulting legal professionals or financial experts in the Virgin Islands can provide guidance on drafting or reviewing a loan agreement to ensure it complies with local laws and regulations.

Virgin Islands Loan Agreement - Short Form

Description

How to fill out Virgin Islands Loan Agreement - Short Form?

US Legal Forms - among the greatest libraries of lawful forms in America - delivers an array of lawful record templates you may down load or produce. Utilizing the site, you can find a large number of forms for enterprise and specific functions, categorized by categories, claims, or key phrases.You can find the latest models of forms much like the Virgin Islands Loan Agreement - Short Form in seconds.

If you currently have a registration, log in and down load Virgin Islands Loan Agreement - Short Form in the US Legal Forms local library. The Down load button can look on every develop you view. You get access to all earlier saved forms from the My Forms tab of the account.

If you wish to use US Legal Forms the first time, listed here are basic directions to obtain started:

- Be sure to have picked out the best develop to your city/state. Go through the Preview button to review the form`s content material. Look at the develop explanation to ensure that you have chosen the correct develop.

- In the event the develop doesn`t suit your demands, make use of the Search industry near the top of the monitor to obtain the one which does.

- If you are satisfied with the form, validate your option by clicking the Get now button. Then, select the rates program you prefer and offer your qualifications to register to have an account.

- Method the financial transaction. Make use of credit card or PayPal account to accomplish the financial transaction.

- Select the structure and down load the form on your product.

- Make alterations. Load, edit and produce and sign the saved Virgin Islands Loan Agreement - Short Form.

Every design you included in your account lacks an expiry date and is your own permanently. So, in order to down load or produce yet another duplicate, just proceed to the My Forms section and click on the develop you will need.

Gain access to the Virgin Islands Loan Agreement - Short Form with US Legal Forms, probably the most substantial local library of lawful record templates. Use a large number of professional and status-particular templates that fulfill your organization or specific needs and demands.