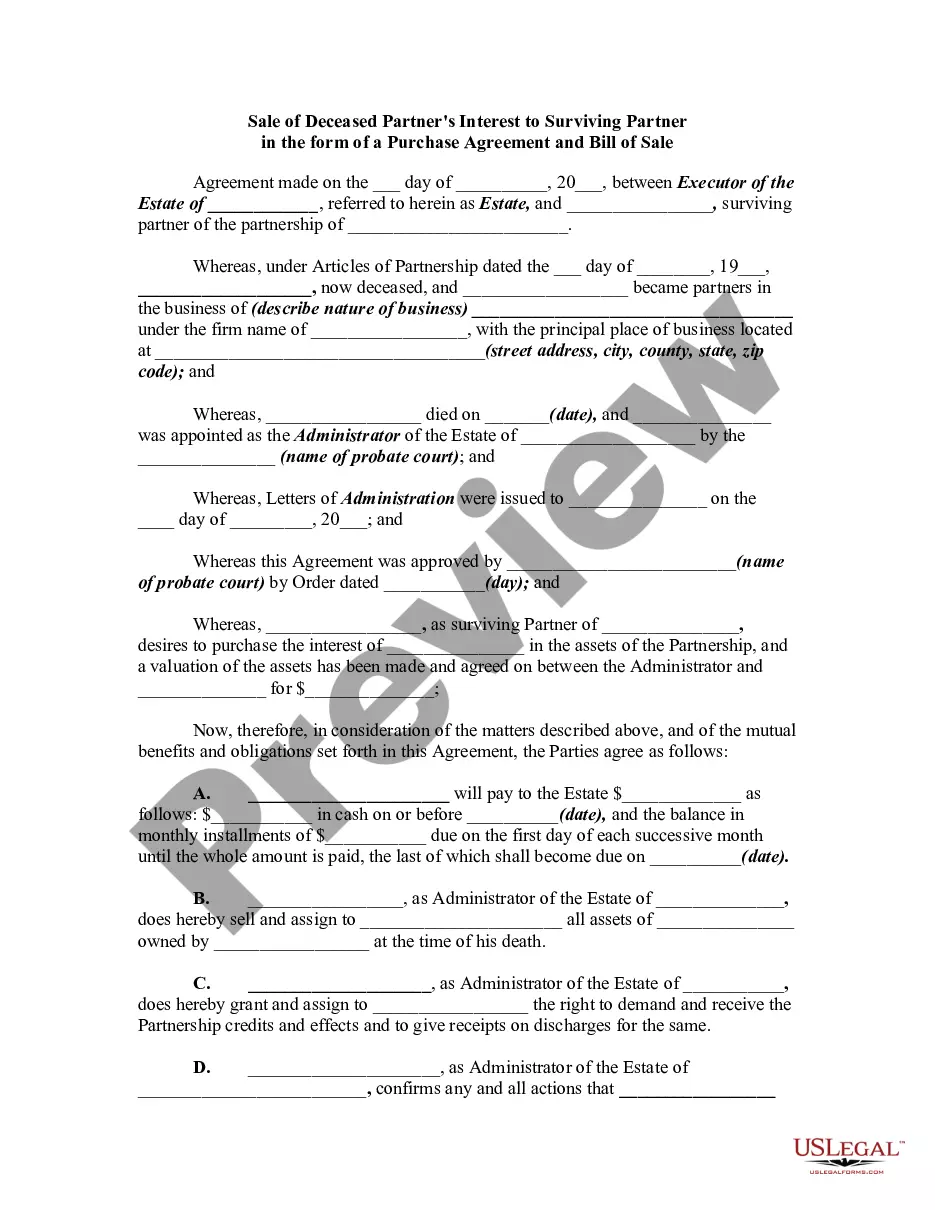

Title: Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner: Purchase Agreement and Bill of Sale Explained Keywords: Virgin Islands, Sale of Deceased Partner's Interest, Surviving Partner, Purchase Agreement, Bill of Sale Introduction: In the Virgin Islands, when a partner passes away, it becomes crucial to handle the transfer of their interest in a partnership to the surviving partner. This process is typically orchestrated through a Purchase Agreement and Bill of Sale, which outlines the terms and conditions of the transaction. In this article, we will discuss the details and importance of the Virgin Islands Sale of Deceased Partner's Interest to the Surviving Partner, shedding light on different types of approaches based on specific scenarios. I. Understanding the Importance of a Purchase Agreement and Bill of Sale: The Sale of Deceased Partner's Interest to the Surviving Partner is governed by a legally binding document, known as a Purchase Agreement and Bill of Sale. This agreement safeguards the rights and interests of both parties while providing a transparent and smooth transition of partnership ownership. II. Overview of a Purchase Agreement and Bill of Sale: A. Key Elements: 1. Identification of Parties: Clearly identify the deceased partner, the surviving partner, and any other relevant partners involved in the agreement. 2. Purchase Price: Specify the agreed-upon value or method of determining the purchase price for the deceased partner's interest. 3. Payment and Terms: Define the payment structure, including the payment method, installments (if any), interest (if applicable), and any other financial considerations. 4. Transfer of Interest: Explicitly state the date or conditions upon which the transfer of the deceased partner's interest will occur. 5. Representations and Warranties: Ensure that both parties provide accurate representations and warranties regarding their ability to enter into the agreement. 6. Indemnification: Address any liabilities or claims that may arise from the transfer of the deceased partner's interest and the surviving partner's assumption of those responsibilities. 7. Dispute Resolution: Establish a mechanism for resolving any disagreements or disputes that may arise during or after the transaction. B. Legal Requirements: 1. Notarization: The Purchase Agreement and Bill of Sale should be notarized to make it legally enforceable. 2. Compliance with Local Laws: Ensure conformity with the applicable laws and regulations in the Virgin Islands regarding partnership rights, taxation, and transfer of ownership. III. Types of Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner: A. Voluntary Agreement: This type of sale occurs when the deceased partner had previously outlined their wishes and the surviving partner agrees to buy their interest based on those predetermined terms and conditions. B. Court-Ordered Sale: If there is no voluntary agreement or the surviving partner is unable to pay the purchase price, the court may order the sale of the deceased partner's interest to the highest bidder, providing a fair opportunity for both the surviving partner and potential third-party buyers. Conclusion: The Virgin Islands Sale of Deceased Partner's Interest to the Surviving Partner through a Purchase Agreement and Bill of Sale is essential to ensure a smooth and legally binding transfer of partnership ownership. Whether based on a voluntary agreement or a court order, following the outlined legal requirements and considering the key elements mentioned above is crucial for a successful transaction. Professionals, such as attorneys and notaries, can guide partners through the process to ensure compliance with local laws and minimize potential conflicts.

Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out Virgin Islands Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

US Legal Forms - among the largest libraries of authorized varieties in America - gives a wide range of authorized record layouts it is possible to obtain or print. Using the website, you can get thousands of varieties for enterprise and specific functions, categorized by groups, says, or search phrases.You will find the newest versions of varieties just like the Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale within minutes.

If you already possess a monthly subscription, log in and obtain Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale from the US Legal Forms collection. The Obtain option will appear on every kind you perspective. You get access to all formerly downloaded varieties from the My Forms tab of your own profile.

In order to use US Legal Forms the first time, allow me to share easy directions to help you started:

- Make sure you have chosen the best kind to your metropolis/state. Select the Preview option to check the form`s information. Read the kind description to actually have selected the appropriate kind.

- In case the kind doesn`t satisfy your demands, use the Look for industry near the top of the display screen to get the the one that does.

- In case you are satisfied with the form, confirm your choice by clicking on the Acquire now option. Then, choose the rates program you prefer and give your credentials to sign up to have an profile.

- Approach the deal. Make use of credit card or PayPal profile to complete the deal.

- Choose the file format and obtain the form in your device.

- Make alterations. Complete, modify and print and indication the downloaded Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale.

Each and every web template you included with your bank account lacks an expiration particular date and it is the one you have permanently. So, if you would like obtain or print another copy, just visit the My Forms section and then click around the kind you want.

Get access to the Virgin Islands Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale with US Legal Forms, probably the most comprehensive collection of authorized record layouts. Use thousands of skilled and state-distinct layouts that meet up with your business or specific needs and demands.

Form popularity

FAQ

A partnership is dissolved when there is a death of a partner as a new partnership deed is to be made.

Business partnership agreement. A properly arranged and funded agreement is a legally binding contract that spells out exactly what is to happen if one of the business's owners dies. It generally calls for the survivors to buy the deceased owner's share in the business from his or her heirs.

If the partner dies, the partner's estate will typically succeed to that decedent's interest in the partnership.

Section 42 (c) of the partnership act can be applied in the case of a firm where there are more than two: partners. If one dies, the firm dissolves, but the surviving partner will continue the firm, whereas, in the case of a partnership between two, the firm by default comes to an end.

If the property is held in a partnership the assets in the partnership do not automatically receive a step-up in basis like those held in a disregarded LLC. It is possible to get a step-up in basis for the assets, but there must be an election under Section 754 of the Internal Revenue Code.

In case of death of a partner, the treatment of various items is similar to that at the time of retirement of the partner. After making all the adjustments in the Partners Capital Account, the amount that is due to him is paid to his Legal Representative.

754 provides an election to adjust the inside bases of partnership assets pursuant to Sec. 743(b) upon the transfer of a partnership interest caused by a partner's death. A Sec. 754 election can also be made when a member's interest is sold or upon certain distributions of partnership assets.

If the property is held in a partnership the assets in the partnership do not automatically receive a step-up in basis like those held in a disregarded LLC. It is possible to get a step-up in basis for the assets, but there must be an election under Section 754 of the Internal Revenue Code.