Virgin Islands Owner Financing Contract for Vehicle

Description

How to fill out Owner Financing Contract For Vehicle?

US Legal Forms - one of the largest collections of legal templates in the United States - offers a wide range of legal document templates that you can download or print.

By using the website, you will find thousands of forms for business and personal purposes, categorized by type, state, or keywords. You can access the latest forms such as the Virgin Islands Owner Financing Contract for Vehicle in just a few minutes.

If you already have a membership, Log In and download the Virgin Islands Owner Financing Contract for Vehicle from the US Legal Forms collection. The Download button will appear on every form you view. You can access all previously downloaded forms in the My documents section of your account.

Choose the format and download the form to your device.

Make edits. Fill in, modify, and print and sign the downloaded Virgin Islands Owner Financing Contract for Vehicle. All templates you add to your account have no expiration date and belong to you indefinitely. So, if you want to download or print another copy, simply navigate to the My documents section and click on the form you need.

- If you’re using US Legal Forms for the first time, here are simple steps to guide you.

- Ensure you have chosen the correct form for your locality/county.

- Click the Review button to examine the document's content.

- Check the form details to confirm that you've selected the right one.

- If the form doesn't meet your requirements, utilize the Search field at the top of the page to find the suitable one.

- If you are happy with the form, confirm your choice by clicking the Buy now button. Then, select your preferred pricing plan and provide your information to sign up for an account.

- Process the payment. Use a credit card or PayPal account to complete the transaction.

Form popularity

FAQ

Yes, in Texas, both the seller and buyer generally need to be present to transfer a title. This process ensures that all documentation is completed accurately, and both parties can verify the information. While this doesn't relate directly to a Virgin Islands Owner Financing Contract for Vehicle, understanding these local requirements can help streamline your vehicle sales across different jurisdictions.

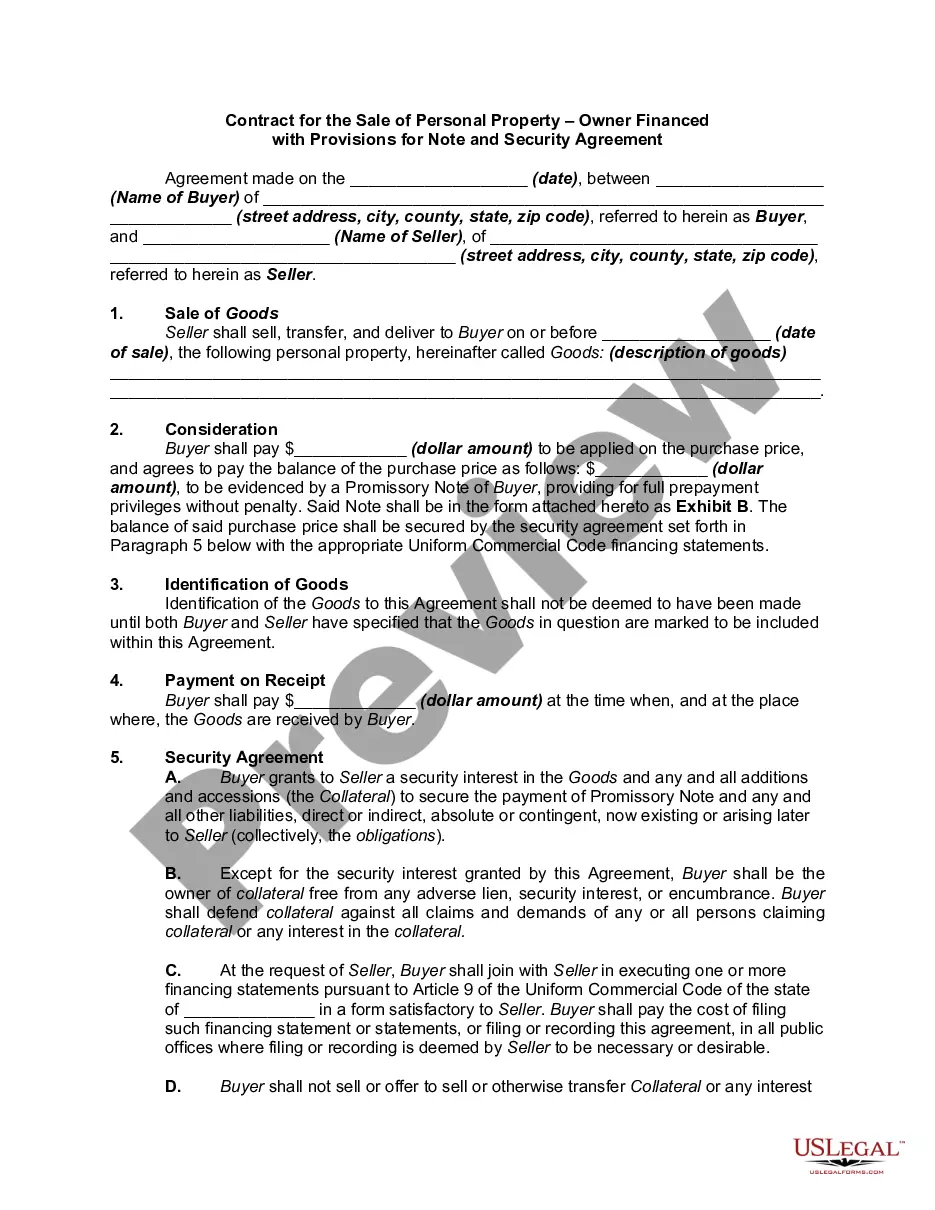

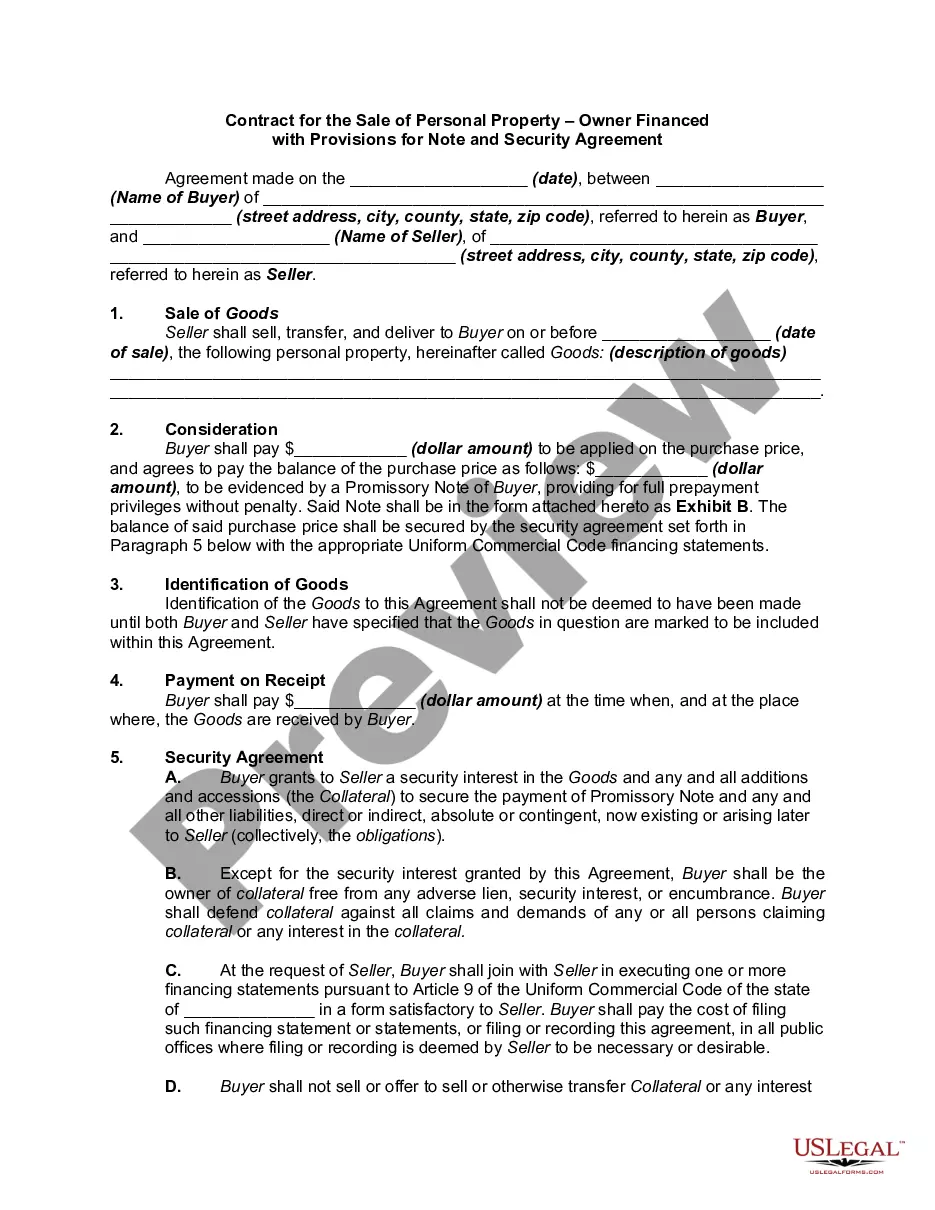

Writing an owner finance contract requires careful attention to detail. Begin by including essential information such as the buyer’s and seller’s names, the vehicle description, and the payment terms. A Virgin Islands Owner Financing Contract for Vehicle template can simplify this process, as it provides a structured format that covers all necessary aspects while being customizable to fit your specific agreement.

In an owner financing setup, the seller typically retains the title to the vehicle until the buyer fulfills all payment obligations. This arrangement protects the seller, allowing them to reclaim the vehicle if the buyer defaults. Therefore, it’s crucial to ensure the terms regarding title transfer are clearly defined in your Virgin Islands Owner Financing Contract for Vehicle.

Writing an owner finance contract requires clear communication of all terms and conditions involved in the sale. Begin by including essential details like buyer and seller information, vehicle specifics, payment structure, and any contingencies. For guidance, you can utilize platforms such as US Legal Forms, which provide templates that help you create a comprehensive Virgin Islands Owner Financing Contract for Vehicle.

When you consider a Virgin Islands Owner Financing Contract for Vehicle, various challenges may arise. For instance, if the buyer fails to make timely payments, you may face difficulties in recouping your investment. Additionally, unclear terms can lead to disputes, so it's essential to clarify all conditions in the contract to avoid misunderstandings.

Writing a finance contract begins with including essential parties and a clear description of the financed item. Outline payment details, interest rates, and both parties' rights and obligations. By using US Legal Forms, you can create a solid Virgin Islands Owner Financing Contract for Vehicle that protects your interests and clarifies the financing terms.