A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

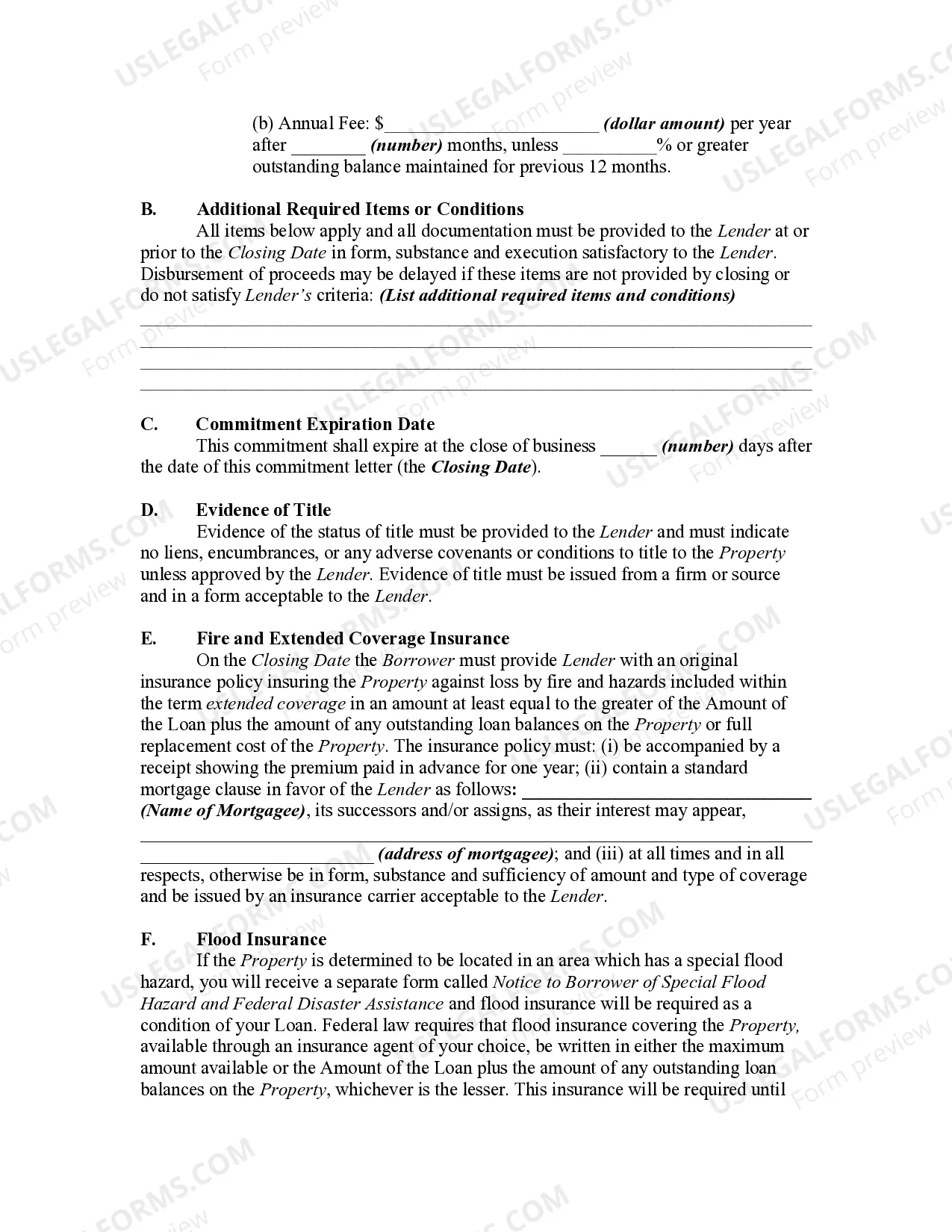

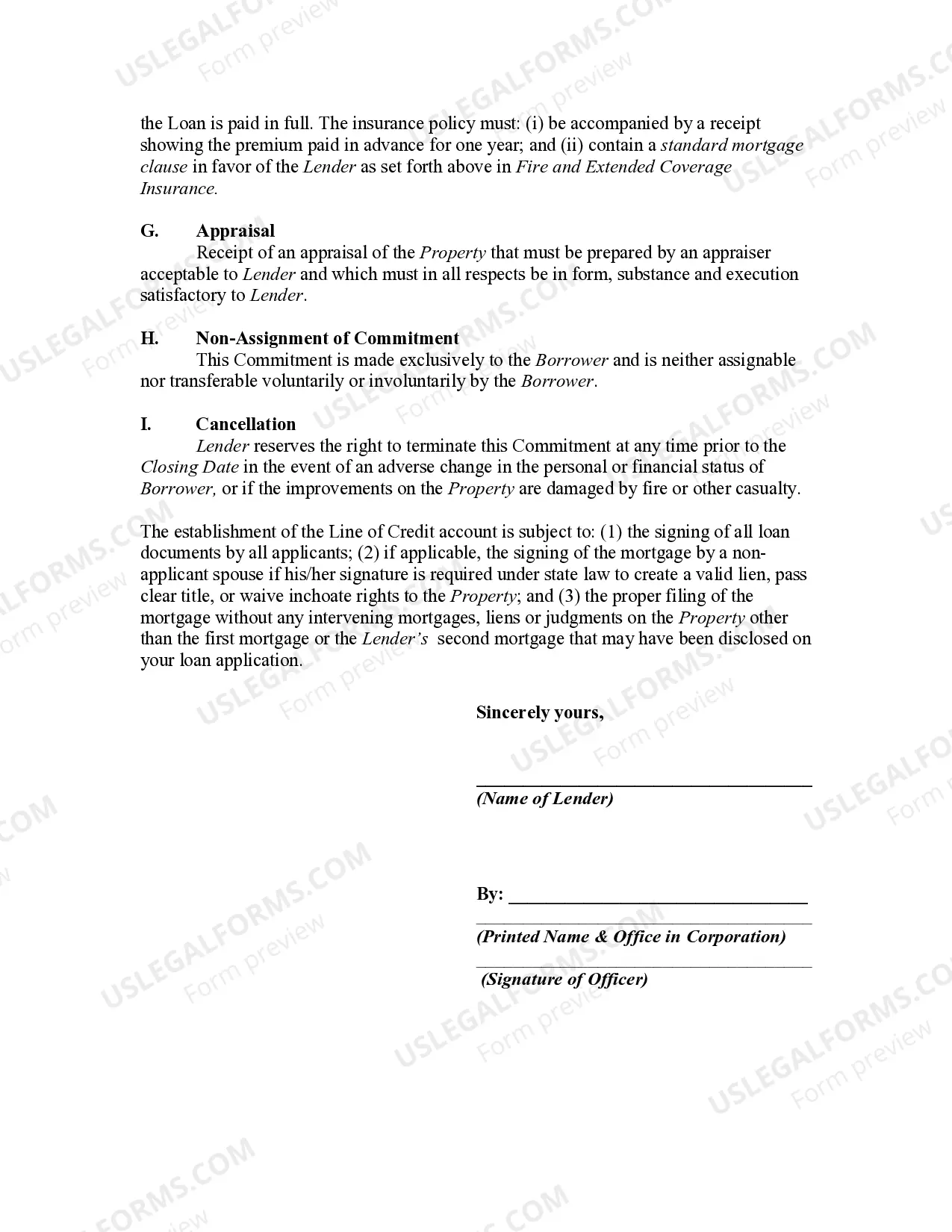

The Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a financial service offered to homeowners in the Virgin Islands who are looking to access the equity in their homes. This commitment allows borrowers to secure a line of credit based on the appraised value of their home, minus any outstanding mortgage balance. A Mortgage Loan Commitment for Home Equity Line of Credit provides homeowners with the flexibility to borrow funds as needed, up to a predetermined credit limit. These funds can be used for various purposes, such as home renovations, debt consolidation, education expenses, or unexpected emergencies. With this commitment, borrowers are required to make minimum monthly payments, typically consisting of just the interest accrued on the amount borrowed. The outstanding balance can be repaid over a specified term or in full at any time, depending on the agreement. Different types of the Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit depend on factors such as interest rates, repayment terms, and credit limits. Some common variations include: 1. Fixed-Rate HELOT: This type of commitment offers a fixed interest rate for a specific period, usually ranging from 5 to 10 years. Borrowers can borrow up to the credit limit during the draw period and make fixed monthly payments for the borrowed amount. 2. Adjustable-Rate HELOT: With an adjustable-rate commitment, the interest rate is tied to an index, such as the prime rate, and may change over time. This can result in fluctuations in monthly payments and overall borrowing costs. 3. Interest-Only HELOT: This commitment allows borrowers to make interest-only payments during the draw period, typically lasting around 10 years. After the draw period ends, the borrower enters the repayment period where both principal and interest payments are required. 4. Home Equity Conversion Mortgage (HELM): This type of commitment is specifically designed for homeowners aged 62 and older, enabling them to convert a portion of their home equity into cash. HELM commitments have unique requirements and regulations, including mandatory counseling sessions for borrowers. To qualify for a Mortgage Loan Commitment for Home Equity Line of Credit, borrowers are typically required to have a good credit score, sufficient income to cover the payments, and a minimum amount of equity in their homes. The loan process often involves appraisals, documentation verification, and closing costs. Choosing the right Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit depends on an individual's financial goals, risk tolerance, and current economic conditions. It is advisable to seek guidance from a reputable lender or financial advisor to determine the most suitable commitment for one's needs and circumstances.The Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a financial service offered to homeowners in the Virgin Islands who are looking to access the equity in their homes. This commitment allows borrowers to secure a line of credit based on the appraised value of their home, minus any outstanding mortgage balance. A Mortgage Loan Commitment for Home Equity Line of Credit provides homeowners with the flexibility to borrow funds as needed, up to a predetermined credit limit. These funds can be used for various purposes, such as home renovations, debt consolidation, education expenses, or unexpected emergencies. With this commitment, borrowers are required to make minimum monthly payments, typically consisting of just the interest accrued on the amount borrowed. The outstanding balance can be repaid over a specified term or in full at any time, depending on the agreement. Different types of the Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit depend on factors such as interest rates, repayment terms, and credit limits. Some common variations include: 1. Fixed-Rate HELOT: This type of commitment offers a fixed interest rate for a specific period, usually ranging from 5 to 10 years. Borrowers can borrow up to the credit limit during the draw period and make fixed monthly payments for the borrowed amount. 2. Adjustable-Rate HELOT: With an adjustable-rate commitment, the interest rate is tied to an index, such as the prime rate, and may change over time. This can result in fluctuations in monthly payments and overall borrowing costs. 3. Interest-Only HELOT: This commitment allows borrowers to make interest-only payments during the draw period, typically lasting around 10 years. After the draw period ends, the borrower enters the repayment period where both principal and interest payments are required. 4. Home Equity Conversion Mortgage (HELM): This type of commitment is specifically designed for homeowners aged 62 and older, enabling them to convert a portion of their home equity into cash. HELM commitments have unique requirements and regulations, including mandatory counseling sessions for borrowers. To qualify for a Mortgage Loan Commitment for Home Equity Line of Credit, borrowers are typically required to have a good credit score, sufficient income to cover the payments, and a minimum amount of equity in their homes. The loan process often involves appraisals, documentation verification, and closing costs. Choosing the right Virgin Islands Mortgage Loan Commitment for Home Equity Line of Credit depends on an individual's financial goals, risk tolerance, and current economic conditions. It is advisable to seek guidance from a reputable lender or financial advisor to determine the most suitable commitment for one's needs and circumstances.