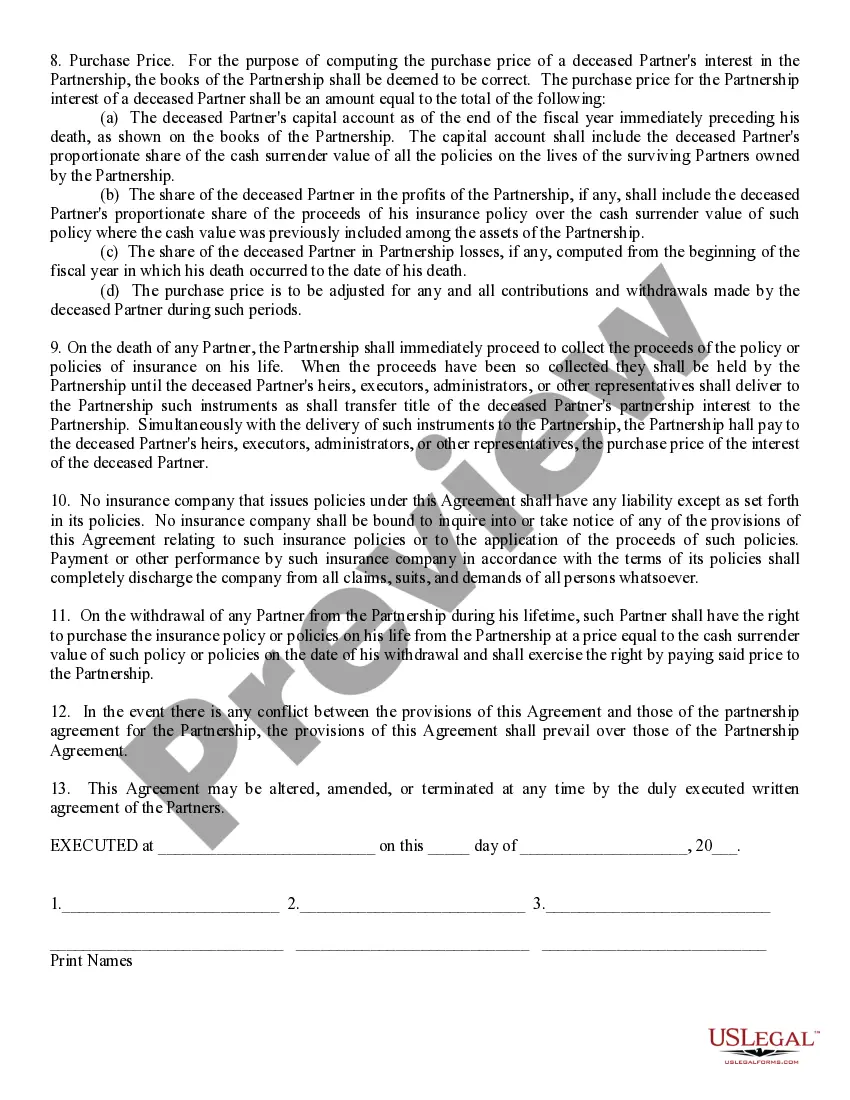

The Virgin Islands Sale of Deceased Partner's Interest refers to the legal process of selling a deceased partner's share in a business located in the Virgin Islands. This can occur when a partner in a partnership or a member in a limited liability company passes away, and their share of ownership needs to be transferred or sold to another party. In the Virgin Islands, there are different types of sales of a deceased partner's interest depending on the business structure and the existing agreements in place: 1. Sale of Deceased Partner's Interest in a Partnership: In a general or limited partnership, when a partner dies, their share of ownership can be transferred to the remaining partners. This type of sale typically involves the surviving partners negotiating the purchase price and terms with the deceased partner's estate or beneficiaries. 2. Sale of Deceased Partner's Interest in a Limited Liability Company (LLC): In an LLC, the deceased member's interest can be sold or transferred to the remaining members or, in some cases, to an external buyer. The sale can be governed by the LLC's operating agreement, which outlines the procedure and terms for such a transfer. 3. Buy-Sell Agreements: In some cases, partnerships or LCS have buy-sell agreements in place, which establish a plan for transferring a deceased partner's interest. These agreements may include provisions such as a right of first refusal, which gives the remaining partners or members the opportunity to buy the interest before it can be sold to an outside party. It's important to note that the sale of a deceased partner's interest in the Virgin Islands typically involves legal and financial considerations. The process may require the involvement of attorneys, accountants, and estate administrators to ensure a smooth transfer of the ownership rights. When dealing with the sale of a deceased partner's interest in the Virgin Islands, it is crucial to understand the specific laws and regulations that govern such transactions. Seeking professional advice is strongly recommended navigating this complex process and to protect the interests of all parties involved.

Virgin Islands Sale of Deceased Partner's Interest

Description

How to fill out Virgin Islands Sale Of Deceased Partner's Interest?

You might spend multiple hours online looking for the legal document format that meets the federal and state requirements you need.

US Legal Forms offers thousands of legal documents that are reviewed by experts.

It is easy to download or print the Virgin Islands Sale of Deceased Partner's Interest from our services.

To find another version of the document, use the Search field to locate the format that satisfies your needs and requirements.

- If you already have a US Legal Forms account, you can Log In and click the Download button.

- Then, you can complete, modify, print, or sign the Virgin Islands Sale of Deceased Partner's Interest.

- Every legal document format you obtain is yours permanently.

- To acquire another copy of a purchased document, go to the My documents tab and click the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document format for the county/city that you choose.

- Review the document description to confirm that you have selected the appropriate document.

Form popularity

FAQ

Although a Virgin Islands inheritance tax is set out in Chapter 1, Title 33 of the V.I. Code, all inheritances after 1984 are exempt from taxation.

About Form 8689, Allocation of Individual Income Tax to the U.S. Virgin Islands Internal Revenue Service.

Under Reg. 1.937-1(c)(1), an individual taxpayer must be physically located in the Virgin Islands for at least 183 days during the tax year. So long as an individual is physically present in the Virgin Islands at any time during the day, for any amount of time, the day will count for purposes of the presence test.

Countries that do not impose a capital gains tax include Bahrain, Barbados, Belize, Cayman Islands, Isle of Man, Jamaica, New Zealand, Sri Lanka, Singapore, and others.

To take the credit, you must complete Form 8689 and attach it to your Form 1040 or 1040-SR. Add line 41 and line 46 of Form 8689 and include the amount in the total on Form 1040 or 1040-SR, Total payments line. On the dotted line next to it, enter Form 8689 and the amount paid.

The mailing address is 9601 Estate Thomas, St. Thomas, VI 00802.

An individual who has income from American Samoa, the Commonwealth of the Northern Mariana Islands (CNMI), Guam, Puerto Rico or the U.S. Virgin Islands will usually have to file a tax return with the tax department of one of these territories.

There is no electronic filing in the Virgin Islands at this time. Taxpayers must drop off in person or mail the returns to the Bureau for processing. For more information about filing requirements for bona fide residents, please call the Office of Chief Counsel at 715-1040, ext. 2249.

The U.S. Virgin Islands is unique among offshore tax planning jurisdictions: it is the only jurisdiction which can offer a tax-free entity under the U.S. flag.

US Virgin Is.: Capital gains taxes (%). It is their only source of capital gains in the country.