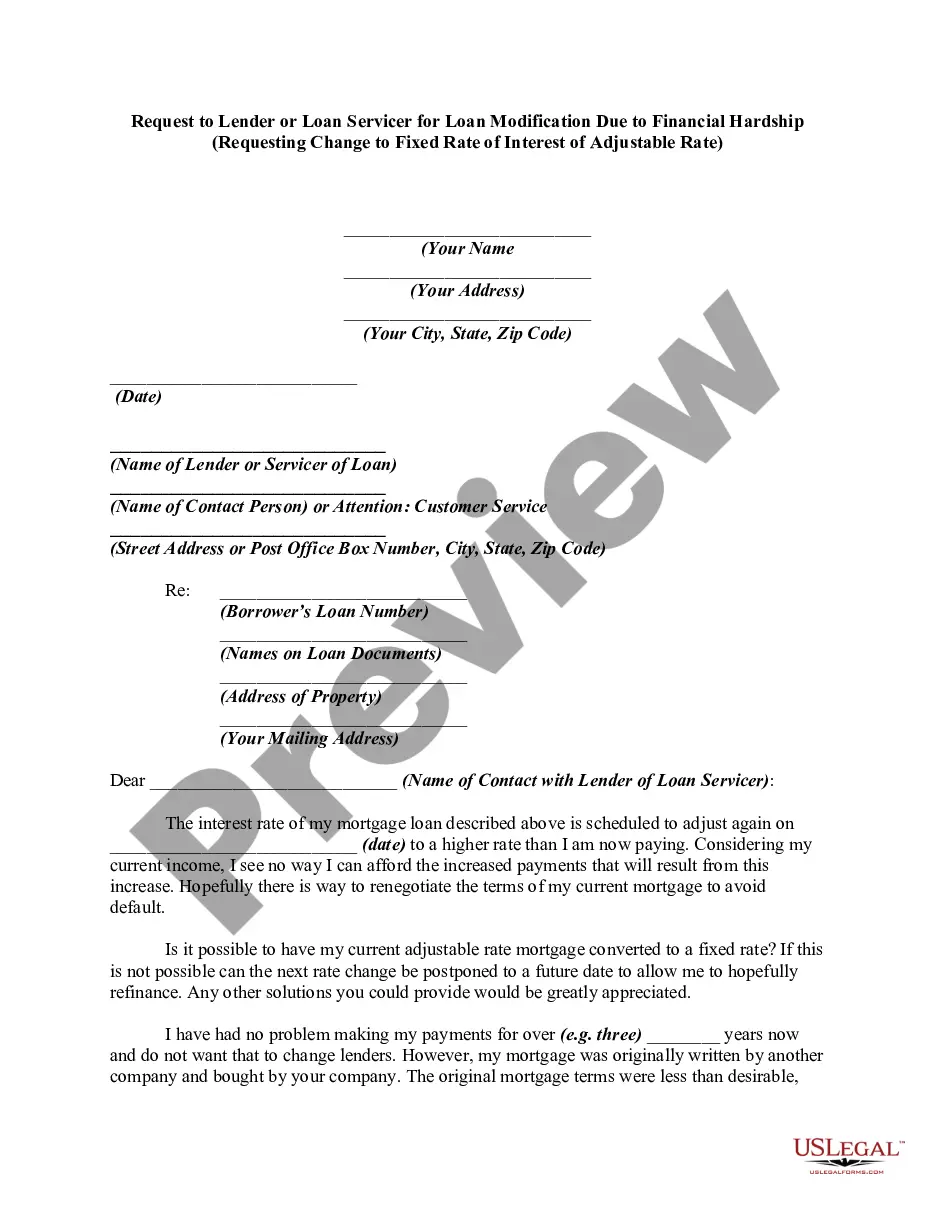

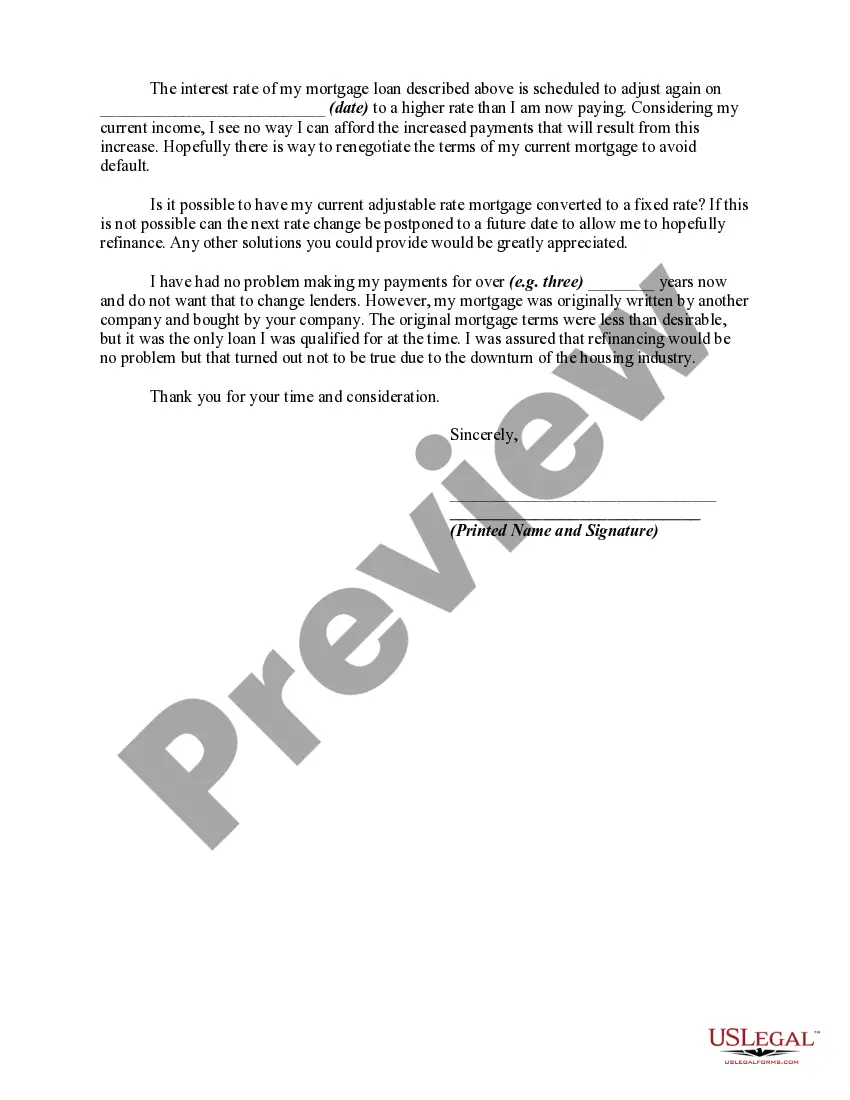

A loan workout is a series of steps taken by a lender with a borrower to resolve the problem of delinquent loan payments. Steps can include rescheduling loan payments into lower installments over a longer period of time so that the entire outstanding principal is eventually repaid. One of the items lenders often ask for during the loan workout or loan modification process is a hardship letter. A hardship letter is a written explanation as to what has caused you to fall behind on your mortgage. Some of the hardships that that lenders consider during the loan workout process are the following: Illness; Loss of Job; Reduced Income; Failed Business; Job Relocation; Death of Spouse or Co-Borrower; Incarceration; Divorce; Military Duty; and Damage to Property (e.g., natural disaster or fire).

Title: Virgin Islands Request to Lender or Loan Service for Loan Modification Due to Financial Hardship — Requesting Change to Fixed Rate of Interest from Adjustable Rate Introduction: In the Virgin Islands, homeowners experiencing financial hardships may face challenges in paying off their adjustable-rate mortgages (ARM). In such situations, homeowners can utilize a loan modification request to their lender or loan service, aimed at obtaining a change from an adjustable rate of interest to a fixed rate. This article provides a comprehensive description highlighting the process, benefits, and considerations associated with the Virgin Islands request for loan modification due to financial hardship. I. Understanding the Virgin Islands Loan Modification Process: 1. Eligibility Criteria: Homeowners seeking a loan modification must meet certain eligibility criteria, such as demonstrating financial hardship and the ability to make modified mortgage payments. 2. Document Preparation: The borrower should gather the necessary documents, including financial statements, proof of income, and a financial hardship letter explaining the reasons behind the request. 3. Submitting the Request: The borrower should submit a well-drafted request to the lender or loan service, emphasizing the reasons for financial hardship and the need for a fixed interest rate to ensure long-term affordability. 4. Review and Decision: The lender or loan service will review the request, evaluate the borrower's financial situation, and determine whether a loan modification is feasible. II. Benefits of Requesting a Change to Fixed Rate: 1. Stable and Predictable Payments: A fixed-rate loan modification provides homeowners with certainty by offering a predetermined, unchanging monthly payment amount for the duration of the loan term. 2. Mitigating Interest Rate Risks: Adjustable-rate mortgages are susceptible to fluctuations in interest rates, which can lead to unpredictable increases in monthly payments. Converting to a fixed rate eliminates this uncertainty. 3. Long-term Affordability: With a fixed-rate loan modification, borrowers can accurately plan their monthly budget, ensuring stable mortgage payments within their financial capabilities. III. Factors to Consider: 1. Financial Assessment: Lenders or loan services will evaluate the borrower's financial situation to determine if a fixed-rate modification is suitable. This analysis may include an examination of income, expenses, employment status, and other relevant factors. 2. Loan Modification Alternatives: In some cases, lenders or loan services may propose alternatives to fixed-rate modifications, such as refinancing options or extending the loan term. Borrowers should weigh these options against their financial goals and long-term affordability. Conclusion: For Virgin Islands homeowners facing financial hardship due to adjustable-rate mortgages, requesting a loan modification to convert to a fixed rate offers numerous benefits. This process allows borrowers to obtain predictable and stable mortgage payments, mitigating the risk associated with fluctuating interest rates. However, it is essential to thoroughly understand the eligibility criteria, gather the required documentation, and consider alternative modification options before submitting a request to the lender or loan service.