Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

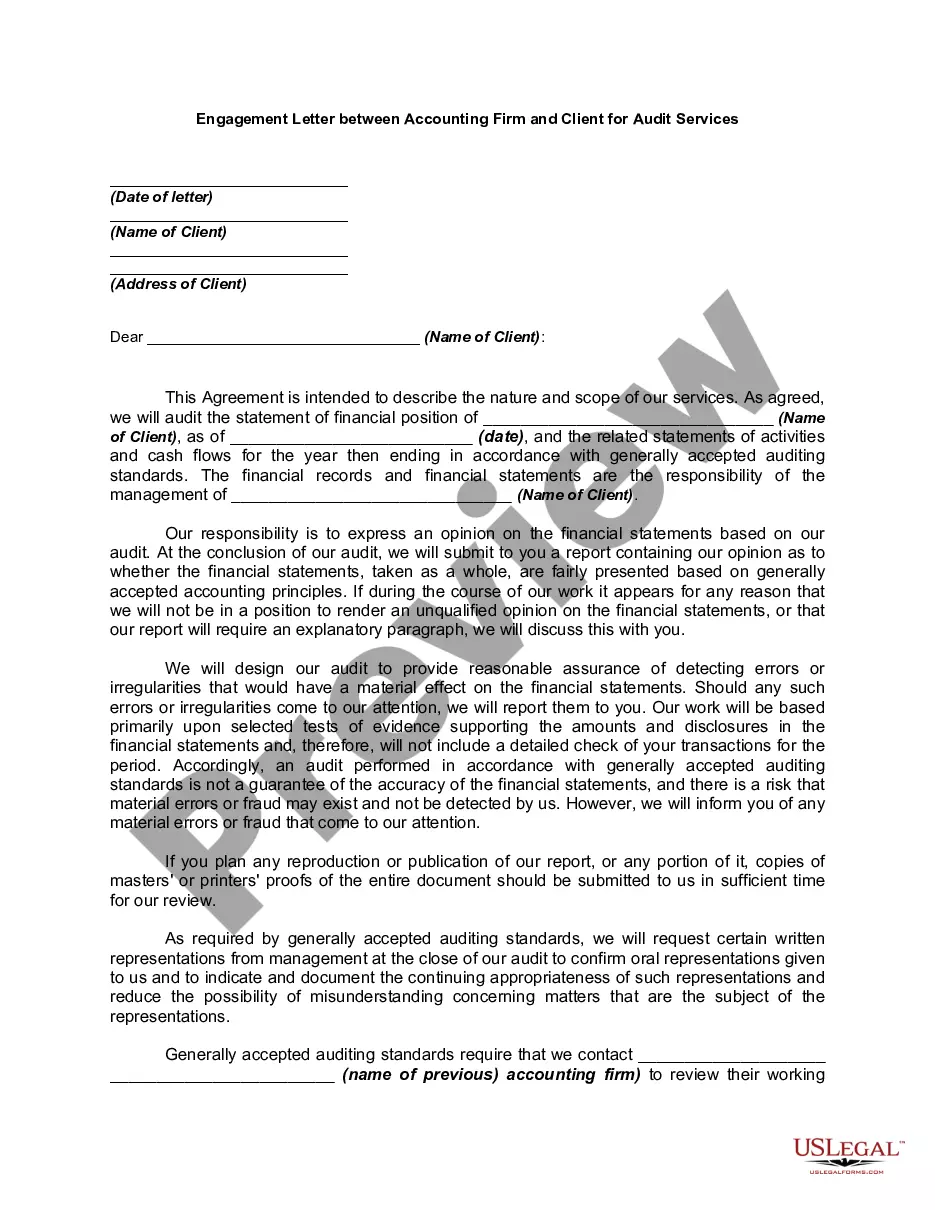

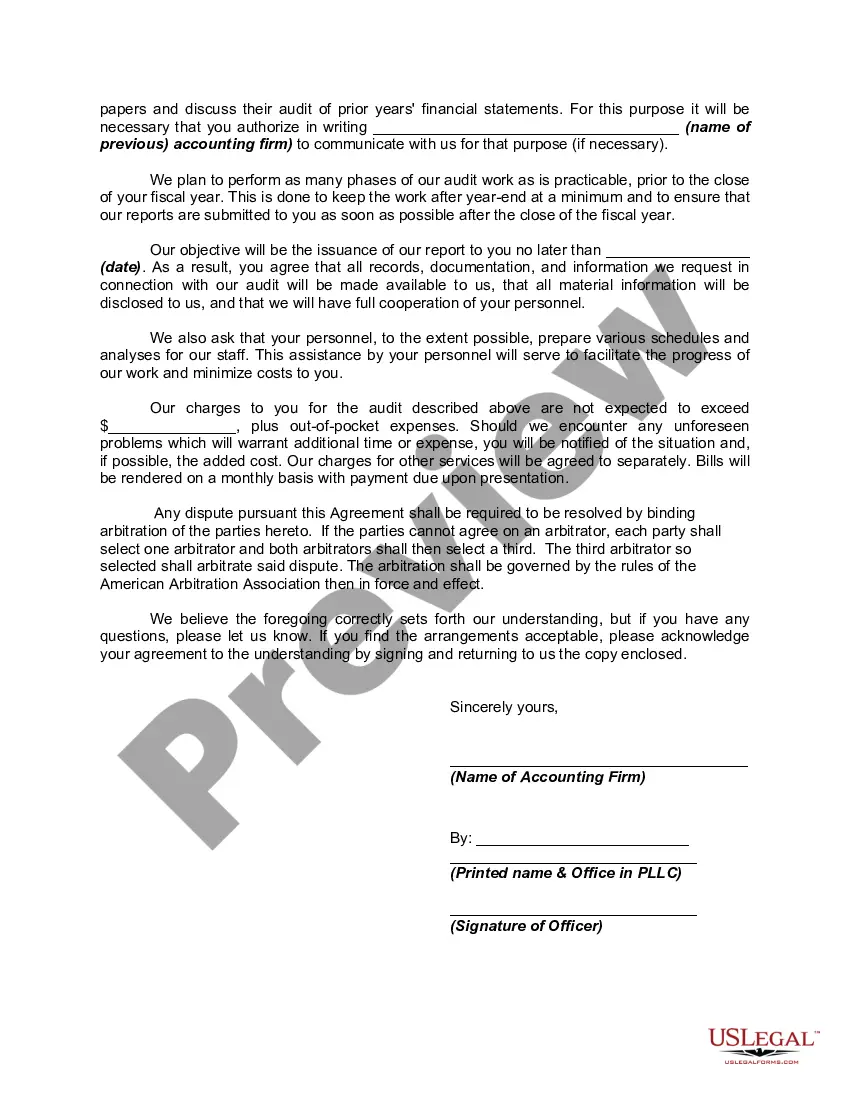

A Virgin Islands Engagement Letter between an accounting firm and a client for audit services is a legally binding document that outlines the terms and conditions of the audit engagement. This letter serves as the basis for a professional relationship between the accounting firm and the client, ensuring transparency and clear expectations in the audit process. The engagement letter typically includes the following key elements: 1. Scope of Services: It clearly defines the specific audit services to be provided by the accounting firm, such as financial statement audits, internal control assessments, or compliance audits. 2. Timeframe: The engagement letter sets forth the stipulated timeline for completing the audit, including any agreed-upon interim reporting or annual financial reporting requirements. 3. Responsibilities of the Accounting Firm: This section outlines the duties and responsibilities of the accounting firm, including conducting the audit in accordance with professional standards, maintaining professional independence, and exercising due professional care during the engagement. 4. Responsibilities of the Client: The engagement letter also clarifies the client's responsibilities, such as providing accurate and complete financial records, facilitating access to relevant personnel and documentation, and ensuring compliance with laws and regulations. 5. Fees and Payment Terms: The engagement letter specifies the audit fees, billing arrangements, and payment terms. This section may also include details about additional expenses, such as travel expenses or out-of-pocket costs. 6. Reporting and Deliverables: It explains the format and content of the final audit report, as well as any interim or draft reports that may be prepared during the engagement. The timeline for the delivery of reports is also usually outlined. 7. Confidentiality and Data Security: The engagement letter highlights the importance of confidentiality and data security, ensuring that sensitive client information is protected and that the accounting firm adheres to relevant privacy laws and regulations. 8. Limitations of Liability: This section establishes the limitations of the accounting firm's liability arising from the audit engagement, protecting both parties from any potential claims or damages. 9. Termination: The engagement letter may include provisions for the termination of the audit engagement, along with the consequences and procedures to be followed in case of termination. Different types of Virgin Islands Engagement Letters between accounting firms and clients for audit services may include variations in terms or areas of focus. For example, there could be specific engagement letters for financial statement audits, compliance audits, internal control assessments, or other specialized audits required by certain industries or regulatory bodies. Overall, the Virgin Islands Engagement Letter establishes a solid framework for the audit engagement, ensuring mutual understanding, clear communication, and legal compliance for both the accounting firm and the client.A Virgin Islands Engagement Letter between an accounting firm and a client for audit services is a legally binding document that outlines the terms and conditions of the audit engagement. This letter serves as the basis for a professional relationship between the accounting firm and the client, ensuring transparency and clear expectations in the audit process. The engagement letter typically includes the following key elements: 1. Scope of Services: It clearly defines the specific audit services to be provided by the accounting firm, such as financial statement audits, internal control assessments, or compliance audits. 2. Timeframe: The engagement letter sets forth the stipulated timeline for completing the audit, including any agreed-upon interim reporting or annual financial reporting requirements. 3. Responsibilities of the Accounting Firm: This section outlines the duties and responsibilities of the accounting firm, including conducting the audit in accordance with professional standards, maintaining professional independence, and exercising due professional care during the engagement. 4. Responsibilities of the Client: The engagement letter also clarifies the client's responsibilities, such as providing accurate and complete financial records, facilitating access to relevant personnel and documentation, and ensuring compliance with laws and regulations. 5. Fees and Payment Terms: The engagement letter specifies the audit fees, billing arrangements, and payment terms. This section may also include details about additional expenses, such as travel expenses or out-of-pocket costs. 6. Reporting and Deliverables: It explains the format and content of the final audit report, as well as any interim or draft reports that may be prepared during the engagement. The timeline for the delivery of reports is also usually outlined. 7. Confidentiality and Data Security: The engagement letter highlights the importance of confidentiality and data security, ensuring that sensitive client information is protected and that the accounting firm adheres to relevant privacy laws and regulations. 8. Limitations of Liability: This section establishes the limitations of the accounting firm's liability arising from the audit engagement, protecting both parties from any potential claims or damages. 9. Termination: The engagement letter may include provisions for the termination of the audit engagement, along with the consequences and procedures to be followed in case of termination. Different types of Virgin Islands Engagement Letters between accounting firms and clients for audit services may include variations in terms or areas of focus. For example, there could be specific engagement letters for financial statement audits, compliance audits, internal control assessments, or other specialized audits required by certain industries or regulatory bodies. Overall, the Virgin Islands Engagement Letter establishes a solid framework for the audit engagement, ensuring mutual understanding, clear communication, and legal compliance for both the accounting firm and the client.