Escrow refers to a type of account in which the money, a mortgage or deed of trust, an existing promissory note secured by the real property, escrow "instructions" from both parties, an accounting of the funds and other documents necessary to complete the transaction by a date, is held by a third party, called an "escrow agent", until the conditions of an agreement are met. When the funding is complete and the deed is clear, the escrow agent will then record the deed to the buyer and deliver funds to the seller. The escrow agent or officer is an independent holder and agent for both parties who receives a fee for their services.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

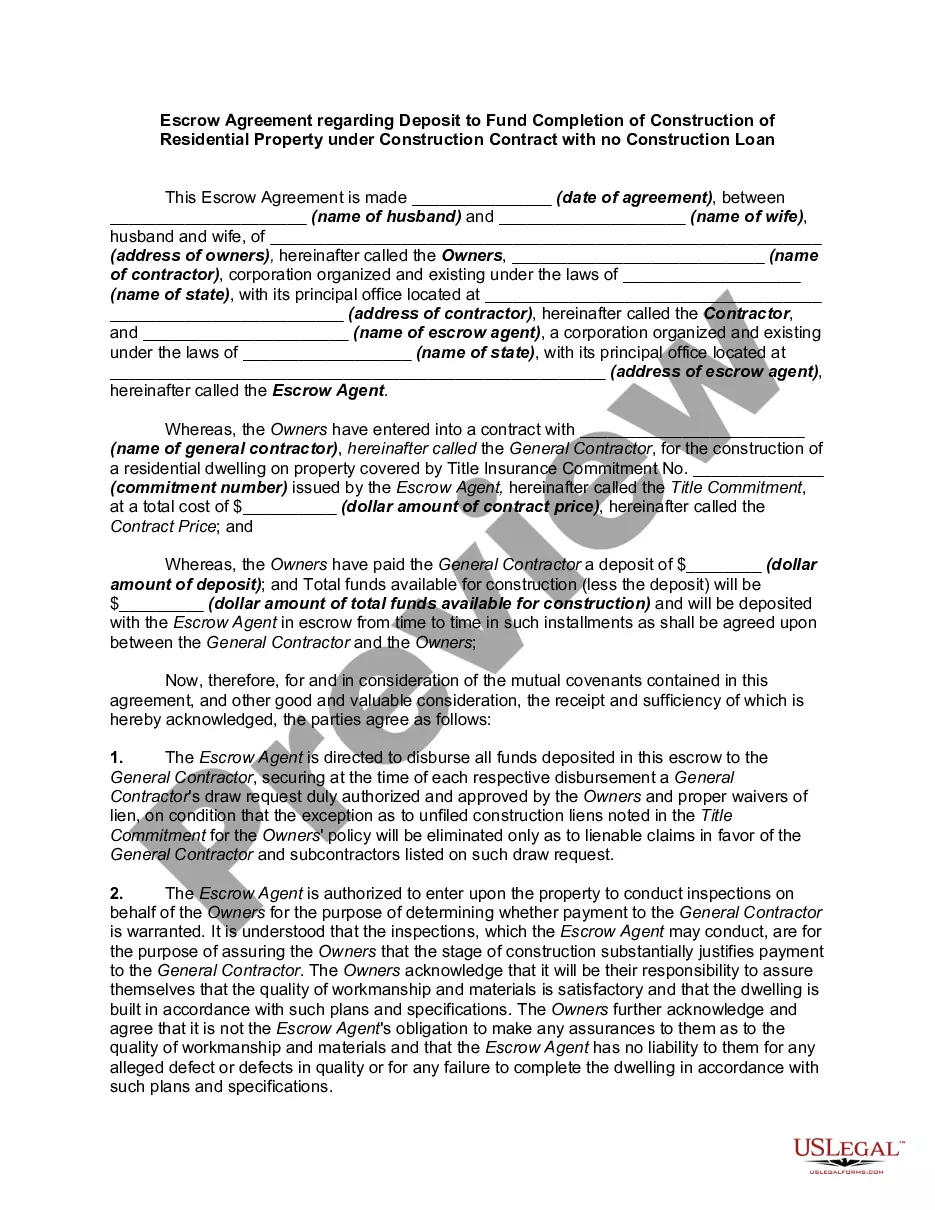

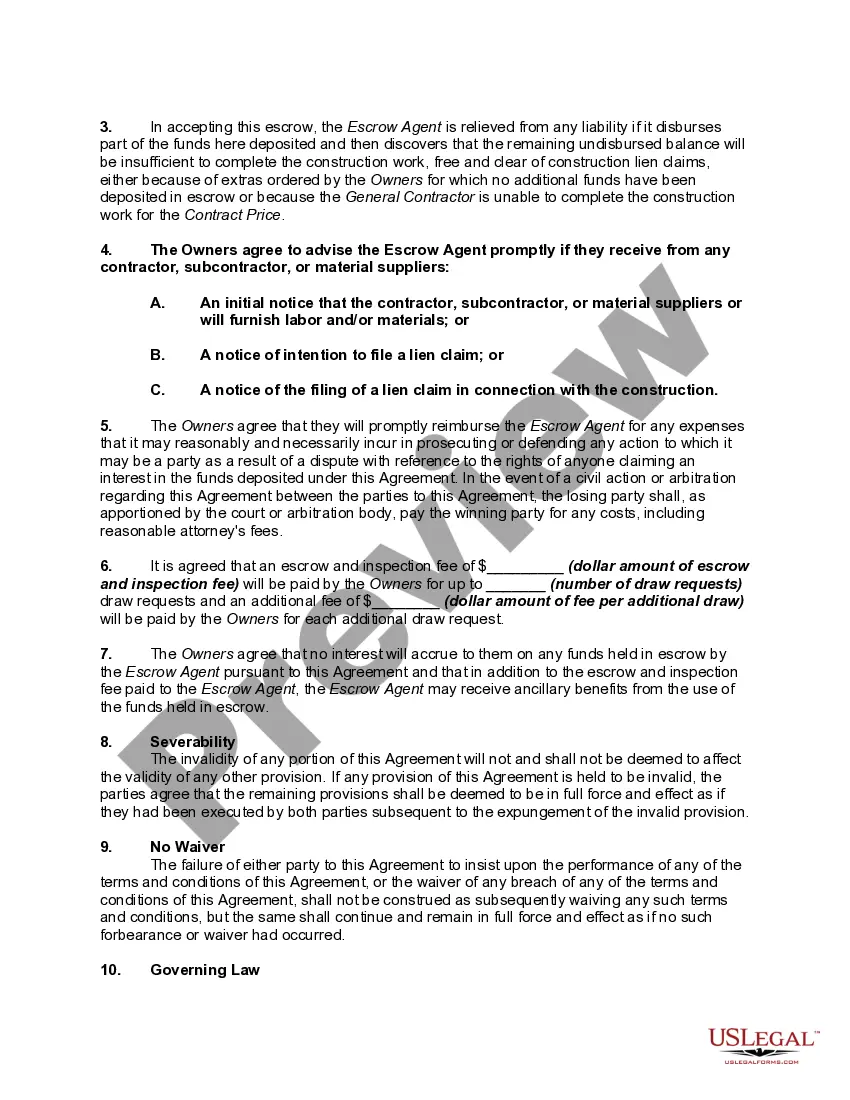

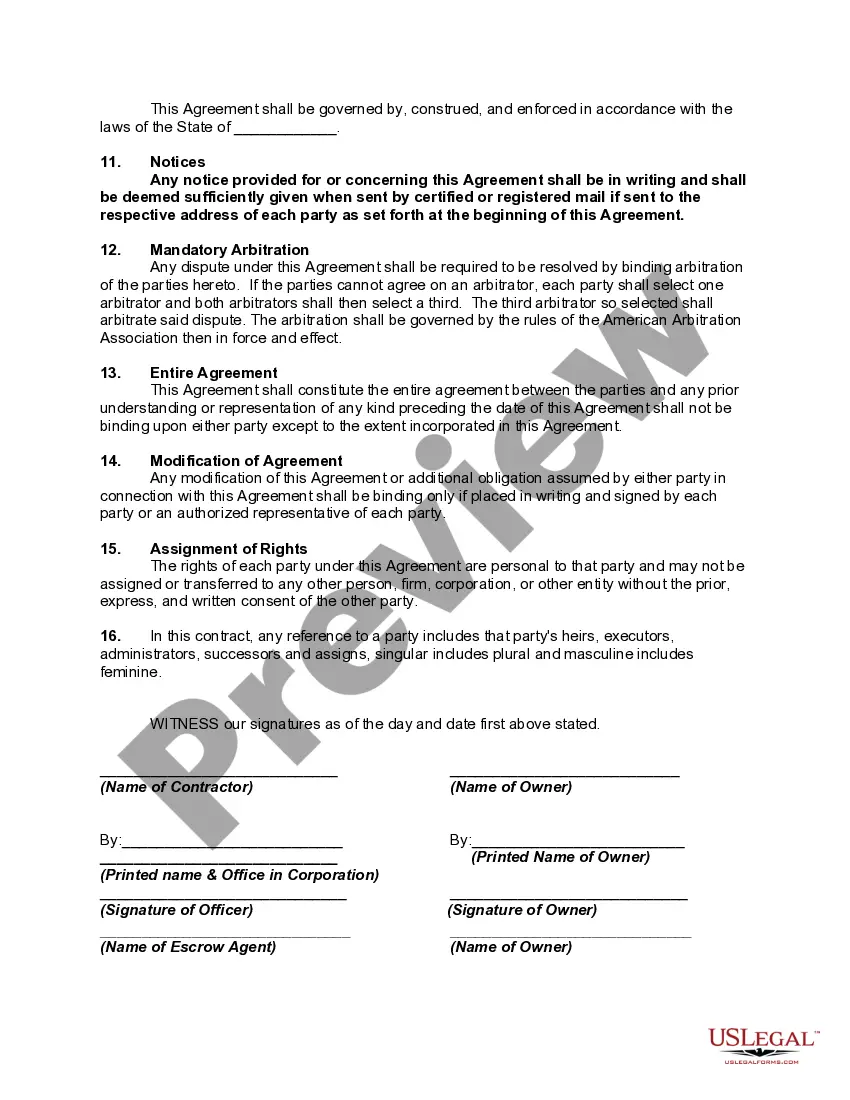

Virgin Islands Escrow Agreement Regarding Deposit to Fund Completion of Construction of Residential Property Under Construction Contract with no Construction Loan In the Virgin Islands, an escrow agreement is a legal arrangement used to ensure the successful completion of construction projects for residential properties. Specifically, it is employed when there is no construction loan involved, and a deposit is required to fund the completion of the project. This agreement safeguards the interests of all parties involved, including the property owner, the contractor, and the escrow agent. The Virgin Islands Escrow Agreement establishes the terms and conditions under which the deposit will be held in escrow and released to fund the construction milestones. Here are the different types of Virgin Islands Escrow Agreements commonly used in such scenarios: 1. Standard Escrow Agreement: This is the most common type of agreement used when there is no construction loan involved. It outlines the responsibilities and obligations of each party, including the deposit amount, the construction milestones, and the release conditions. 2. Disbursement Escrow Agreement: In certain cases, the parties may opt for a disbursement escrow agreement. This agreement specifies the construction milestones and the corresponding funds to be released upon the completion of each milestone. It ensures that the funds are disbursed in a timely manner, promoting project progress. 3. Performance Escrow Agreement: This type of escrow agreement adds a layer of security for the property owner. It requires the contractor to deposit a performance bond or provide additional collateral as a guarantee for completing the construction project within the specified terms. 4. Dual Escrow Agreement: In complex construction projects, where multiple parties are involved, a dual escrow agreement may be utilized. This agreement allows for separate escrow accounts to be established, one for the property owner and another for the contractor. Each party's funds are held separately, providing an added level of transparency and protection. Regardless of the type of Virgin Islands Escrow Agreement used, there are key elements included in all these agreements: a. Parties Involved: The agreement should clearly state the names and contact information of the property owner, the contractor, and the escrow agent. b. Deposit Amount: The agreement outlines the specific amount of the deposit required to fund the completion of the construction project. c. Construction Milestones: The agreement should define the construction milestones that need to be completed, such as foundation, framing, electrical wiring, plumbing, etc. d. Release Conditions: The conditions under which the funds will be released from escrow to the contractor should be clearly specified. This could include inspection reports, certification of completion, or any other project-specific conditions. e. Dispute Resolution: The agreement should outline the procedures for dispute resolution in case conflicts arise during the project. f. Termination Clause: In the event of project cancellation or failure to complete the construction, the agreement should include a termination clause that outlines the steps for returning the remaining deposit to the property owner. In conclusion, the Virgin Islands Escrow Agreement regarding the deposit to fund the completion of construction of residential property under a construction contract with no construction loan plays a crucial role in protecting the interests of all parties involved. By clearly defining the terms and conditions, these agreements ensure transparency, timely disbursements, and a successful completion of the construction project.Virgin Islands Escrow Agreement Regarding Deposit to Fund Completion of Construction of Residential Property Under Construction Contract with no Construction Loan In the Virgin Islands, an escrow agreement is a legal arrangement used to ensure the successful completion of construction projects for residential properties. Specifically, it is employed when there is no construction loan involved, and a deposit is required to fund the completion of the project. This agreement safeguards the interests of all parties involved, including the property owner, the contractor, and the escrow agent. The Virgin Islands Escrow Agreement establishes the terms and conditions under which the deposit will be held in escrow and released to fund the construction milestones. Here are the different types of Virgin Islands Escrow Agreements commonly used in such scenarios: 1. Standard Escrow Agreement: This is the most common type of agreement used when there is no construction loan involved. It outlines the responsibilities and obligations of each party, including the deposit amount, the construction milestones, and the release conditions. 2. Disbursement Escrow Agreement: In certain cases, the parties may opt for a disbursement escrow agreement. This agreement specifies the construction milestones and the corresponding funds to be released upon the completion of each milestone. It ensures that the funds are disbursed in a timely manner, promoting project progress. 3. Performance Escrow Agreement: This type of escrow agreement adds a layer of security for the property owner. It requires the contractor to deposit a performance bond or provide additional collateral as a guarantee for completing the construction project within the specified terms. 4. Dual Escrow Agreement: In complex construction projects, where multiple parties are involved, a dual escrow agreement may be utilized. This agreement allows for separate escrow accounts to be established, one for the property owner and another for the contractor. Each party's funds are held separately, providing an added level of transparency and protection. Regardless of the type of Virgin Islands Escrow Agreement used, there are key elements included in all these agreements: a. Parties Involved: The agreement should clearly state the names and contact information of the property owner, the contractor, and the escrow agent. b. Deposit Amount: The agreement outlines the specific amount of the deposit required to fund the completion of the construction project. c. Construction Milestones: The agreement should define the construction milestones that need to be completed, such as foundation, framing, electrical wiring, plumbing, etc. d. Release Conditions: The conditions under which the funds will be released from escrow to the contractor should be clearly specified. This could include inspection reports, certification of completion, or any other project-specific conditions. e. Dispute Resolution: The agreement should outline the procedures for dispute resolution in case conflicts arise during the project. f. Termination Clause: In the event of project cancellation or failure to complete the construction, the agreement should include a termination clause that outlines the steps for returning the remaining deposit to the property owner. In conclusion, the Virgin Islands Escrow Agreement regarding the deposit to fund the completion of construction of residential property under a construction contract with no construction loan plays a crucial role in protecting the interests of all parties involved. By clearly defining the terms and conditions, these agreements ensure transparency, timely disbursements, and a successful completion of the construction project.