An escrow account refers to an account held in the name of the borrower which is returnable to the borrower on the performance of certain conditions.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

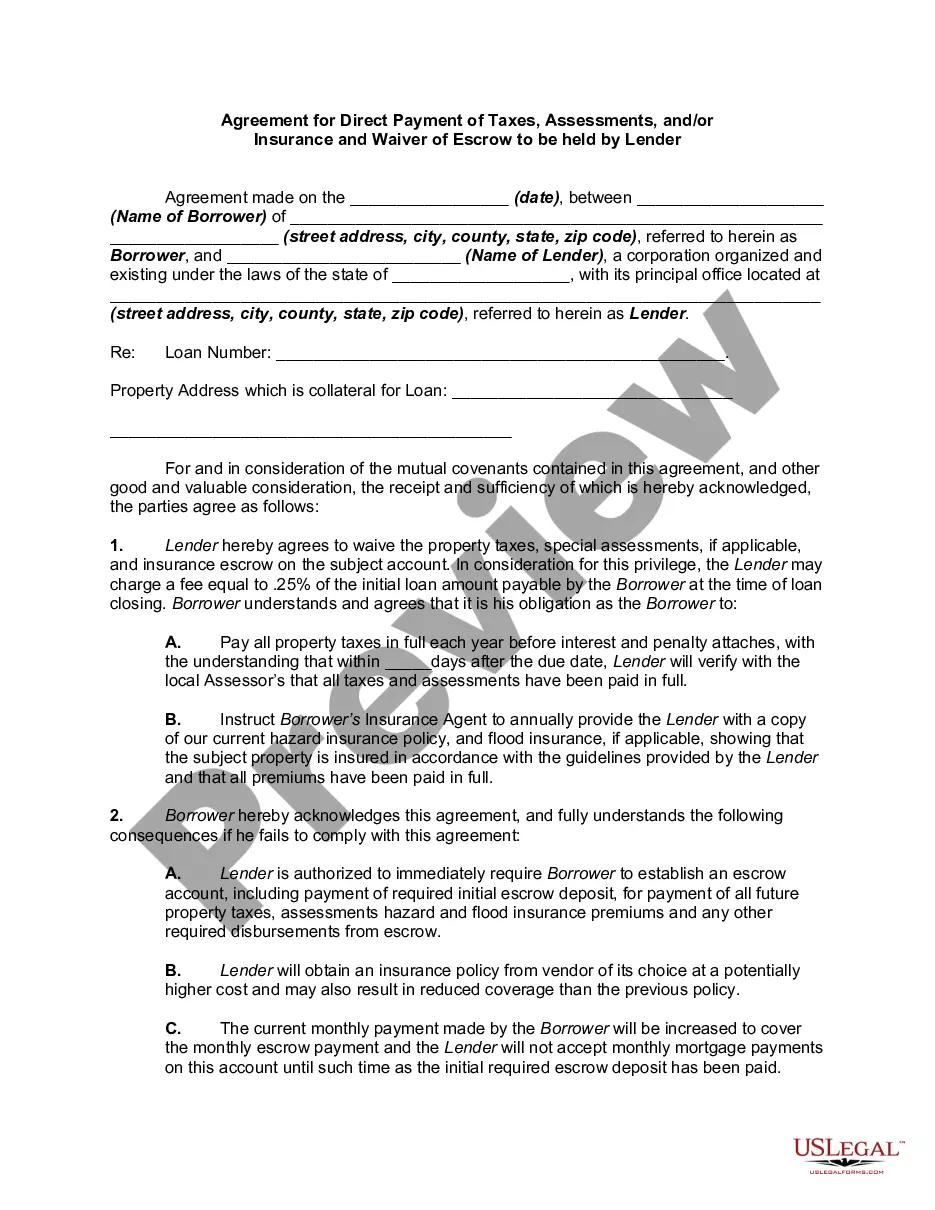

The Virgin Islands Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender is a legal document that outlines the terms and conditions for the direct payment of taxes, assessments, and insurance by a borrower in the Virgin Islands. This agreement allows the borrower to take responsibility for making these payments directly, rather than having the mes crowed and managed by the lender. In this agreement, the borrower agrees to pay all applicable taxes, assessments, and insurance premiums directly to the respective government agencies and insurance providers. This arrangement ensures that the borrower retains control over these payments and can manage them in a way that aligns with their financial planning. By waiving the escrow requirement, the borrower is not required to contribute additional funds to an escrow account maintained by the lender. Instead, they can allocate their resources more efficiently and make payments directly as they come due. This can provide the borrower with greater flexibility and control over their financial obligations. There are different types of the Virgin Islands Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender, including: 1. Virgin Islands Agreement for Direct Payment of Taxes: This type of agreement specifically focuses on the direct payment of taxes owed by the borrower to the Virgin Islands government. It outlines the obligations of the borrower to timely pay property taxes and any other applicable taxes directly. 2. Virgin Islands Agreement for Direct Payment of Assessments: This variant of the agreement focuses on the direct payment of assessments, such as homeowners association fees or special assessments on the property. It ensures that the borrower is responsible for making these payments directly to the relevant association or entity. 3. Virgin Islands Agreement for Direct Payment of Insurance: This agreement type pertains to the direct payment of insurance premiums, encompassing homeowner's insurance, flood insurance, or any other insurance coverage required by the lender or the Virgin Islands jurisdiction. It grants the borrower the responsibility of making these payments directly to the insurance provider. Each type of agreement serves to outline the specific obligations of the borrower to make direct payments for taxes, assessments, and/or insurance, while waiving the requirement for an escrow account held by the lender. These agreements facilitate a more direct and efficient financial management process for borrowers in the Virgin Islands.The Virgin Islands Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender is a legal document that outlines the terms and conditions for the direct payment of taxes, assessments, and insurance by a borrower in the Virgin Islands. This agreement allows the borrower to take responsibility for making these payments directly, rather than having the mes crowed and managed by the lender. In this agreement, the borrower agrees to pay all applicable taxes, assessments, and insurance premiums directly to the respective government agencies and insurance providers. This arrangement ensures that the borrower retains control over these payments and can manage them in a way that aligns with their financial planning. By waiving the escrow requirement, the borrower is not required to contribute additional funds to an escrow account maintained by the lender. Instead, they can allocate their resources more efficiently and make payments directly as they come due. This can provide the borrower with greater flexibility and control over their financial obligations. There are different types of the Virgin Islands Agreement for Direct Payment of Taxes, Assessments, and/or Insurance and Waiver of Escrow to be held by Lender, including: 1. Virgin Islands Agreement for Direct Payment of Taxes: This type of agreement specifically focuses on the direct payment of taxes owed by the borrower to the Virgin Islands government. It outlines the obligations of the borrower to timely pay property taxes and any other applicable taxes directly. 2. Virgin Islands Agreement for Direct Payment of Assessments: This variant of the agreement focuses on the direct payment of assessments, such as homeowners association fees or special assessments on the property. It ensures that the borrower is responsible for making these payments directly to the relevant association or entity. 3. Virgin Islands Agreement for Direct Payment of Insurance: This agreement type pertains to the direct payment of insurance premiums, encompassing homeowner's insurance, flood insurance, or any other insurance coverage required by the lender or the Virgin Islands jurisdiction. It grants the borrower the responsibility of making these payments directly to the insurance provider. Each type of agreement serves to outline the specific obligations of the borrower to make direct payments for taxes, assessments, and/or insurance, while waiving the requirement for an escrow account held by the lender. These agreements facilitate a more direct and efficient financial management process for borrowers in the Virgin Islands.