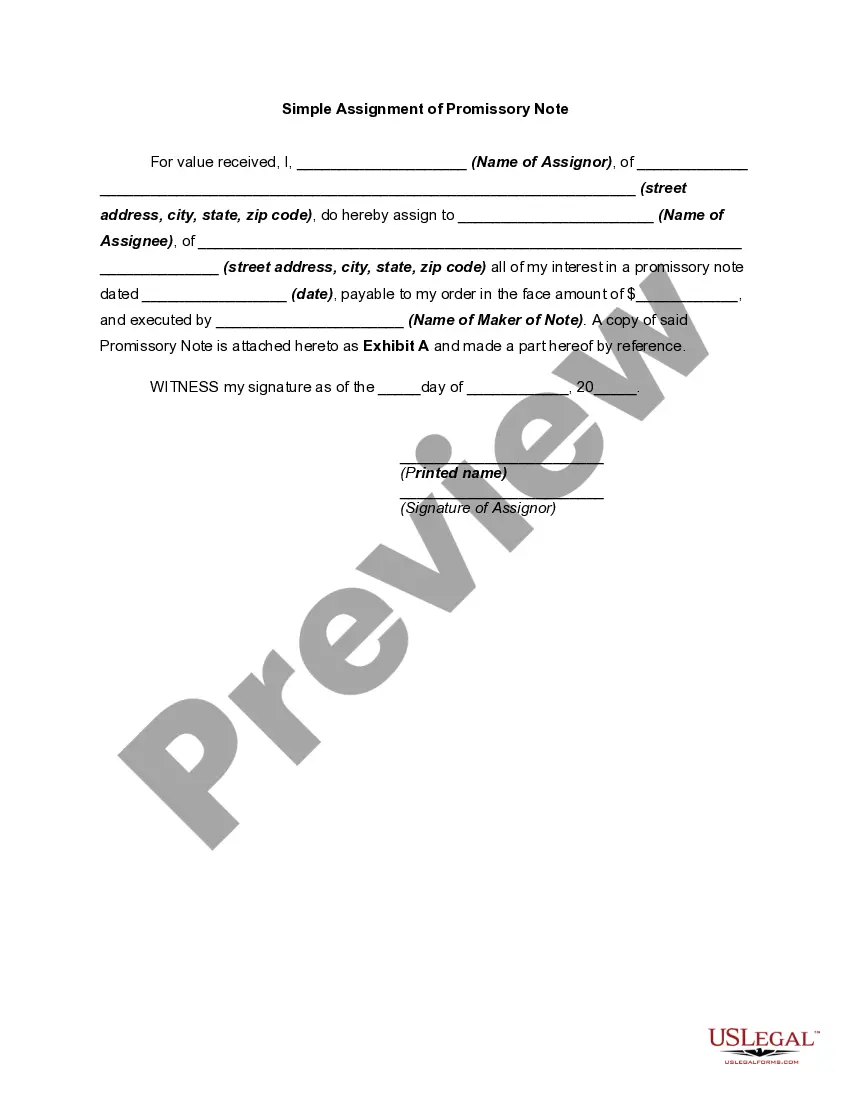

A Virgin Islands Simple Promissory Note for Family Loan is a legal document that outlines the terms and conditions of a loan agreement between family members in the United States Virgin Islands. This note serves as a written record of the loan, ensuring that both parties involved are protected and aware of their rights and responsibilities. The Virgin Islands Simple Promissory Note for Family Loan can be used for various purposes, including lending money to a family member to finance a new business, purchase a home, cover educational expenses, or any other financial need. It represents a formal agreement between the lender and the borrower, detailing the loan amount, repayment terms, and any applicable interest rates. This type of promissory note is relatively straightforward and does not involve complex legal language or extensive requirements, making it suitable for family loans. However, it is crucial to include specific information in the document to ensure its validity and enforceability. The key elements typically included in a Virgin Islands Simple Promissory Note for Family Loan are: 1. Loan details: The note should clearly state the amount of the loan, whether it is a one-time lump sum or multiple disbursements over a period of time. 2. Interest terms: If applicable, the note should specify the interest rate charged on the loan. It is important to establish whether the interest will be simple or compound and whether it will be calculated monthly, annually, or upon maturity. 3. Repayment terms: The note should outline the repayment schedule, including the amount to be paid monthly or in a lump sum, the due date, and the duration of the loan. It is advisable to include details on any grace period or prepayment options. 4. Collateral: In some cases, a Virgin Islands Simple Promissory Note for Family Loan may require collateral as security for the loan. If collateral is involved, it should be clearly stated in the document, along with a description of the collateral and its estimated value. 5. Signatures and witnesses: Both the lender and the borrower should sign and date the promissory note. It is often recommended having witnesses present to ensure the legality of the agreement. These witnesses should also sign the document. It is essential to consult with a legal professional or seek legal advice while drafting a Virgin Islands Simple Promissory Note for Family Loan to ensure compliance with local laws and regulations. Other specific types of promissory notes in the Virgin Islands may include demand promissory notes, installment promissory notes, or balloon promissory notes. Each of these types may have variations in terms and repayment structures, depending on the specific needs and requirements of the loan arrangement.

Virgin Islands Simple Promissory Note for Family Loan

Description

How to fill out Virgin Islands Simple Promissory Note For Family Loan?

Have you been inside a situation where you require papers for possibly organization or person functions virtually every working day? There are a lot of lawful papers themes available on the net, but discovering versions you can rely is not simple. US Legal Forms delivers a large number of develop themes, like the Virgin Islands Simple Promissory Note for Family Loan, that happen to be published to fulfill federal and state needs.

When you are presently familiar with US Legal Forms website and get a free account, basically log in. Following that, you are able to acquire the Virgin Islands Simple Promissory Note for Family Loan web template.

If you do not offer an account and need to start using US Legal Forms, follow these steps:

- Obtain the develop you want and ensure it is for your correct city/area.

- Utilize the Preview switch to examine the shape.

- See the description to actually have chosen the right develop.

- In the event the develop is not what you are looking for, use the Look for industry to get the develop that fits your needs and needs.

- Once you find the correct develop, just click Acquire now.

- Opt for the pricing strategy you desire, fill in the required info to create your money, and buy an order with your PayPal or charge card.

- Select a convenient file file format and acquire your backup.

Locate each of the papers themes you might have purchased in the My Forms menus. You may get a further backup of Virgin Islands Simple Promissory Note for Family Loan at any time, if necessary. Just click the needed develop to acquire or print the papers web template.

Use US Legal Forms, probably the most considerable selection of lawful kinds, to save time and prevent blunders. The services delivers expertly manufactured lawful papers themes which can be used for a selection of functions. Create a free account on US Legal Forms and start making your daily life a little easier.

Form popularity

FAQ

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

The name and address of the person loaning the money. The name and address of the person borrowing the money. Terms of repayment: schedule of repayment, amount of each payment and manner of payments (in-person, cash, check, etc.) Interest to be charged related to the loan, if any.

A personal loan agreement should include the following information:Names and addresses of the lender and the borrower.Information about the loan cosigner, if applicable.Amount borrowed.Date the loan was provided.Expected repayment date.Interest rate, if applicable.Annual percentage rate (APR), if applicable.More items...?

A family loan, sometimes called an intra-family loan, is a loan between family members. Family loans are often less formal than personal loans from traditional lenders or in the peer-to-peer (P2P) marketplace, which connects potential investors directly to borrowers.

Put family loans in writing Be sure to include both parties in the decision-making process. Basic terms for a family loan agreement may include: The amount borrowed and how it will be used. Repayment terms, including payment amounts, frequency and when the loan will be repaid in full.

How do I write a loan agreement for a family member?Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule.Set and interest rate.Put your agreement in writing.Keep payment records.

How do I write a loan agreement for a family member?Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule.Set and interest rate.Put your agreement in writing.Keep payment records.

Put family loans in writingThe amount borrowed and how it will be used.Repayment terms, including payment amounts, frequency and when the loan will be repaid in full.The loan's interest rate.If the loan can be repaid early without penalty, and how much interest will be saved by early repayment.More items...?